Part A

Introduction

UG UG Users Guide

UG-A UG-A Introduction

UG-A.1 UG-A.1 Purpose

UG-A.1.1

The Central Bank of Bahrain ('the CBB'), in its capacity as the regulatory and supervisory authority for all financial institutions in Bahrain, issues regulatory instruments that licensees and other specified persons are legally obliged to comply with. These regulatory instruments are contained in the CBB Rulebook. Much of the Rulebook’s substantive content was previously issued by the Bahrain Monetary Agency (‘the BMA’), and was carried forward when the CBB replaced the BMA in September 2006.

Amended: January 2007UG-A.1.2

The Rulebook is divided into 7 Volumes, covering different areas of financial services activity. These Volumes are being progressively issued. Volumes 1 and 2, covering conventional and Islamic bank licensees respectively, were issued in July 2004 and January 2005. This Volume (Volume 3), was issued in April 2005. Volume 4, covering investment business, was issued in April 2006. Volumes 5 (covering specialised licensees), and Volume 6 (capital markets) are being issued gradually. Volume 7 on collective investment undertakings (CIUs) was issued in May 2012.

Amended: October 2012

Amended: October 2007

Amended: January 2007UG-A.1.3

This User's Guide provides guidance on (i) the status and application of the Rulebook, with specific reference to Volume 3 (Insurance); (ii) the structure and design of the Rulebook; and (iii) its maintenance and version control.

Amended: January 2007UG-A.1.4

Volume 3 (Insurance) covers

insurance licensees , i.e. those CBB licensees that solely undertakeregulated insurance services . It contains prudential requirements (such as rules on minimum capital and risk management); and conduct of business requirements (such as rules on providing insurance services and the treatment ofpolicyholders ). Collectively, these requirements are aimed at ensuring the safety and soundness of the CBB, and providing an appropriate level of protection forpolicyholders .Added: January 2007

Amended: October 2007Legal Basis

UG-A.1.5

This Module contains the CBB's Directive (as amended from time to time) regarding the User's Guide for Volume 3 of the CBB Rulebook, and is issued under the powers available to the CBB under Article 38 of the of the Central Bank of Bahrain and Financial Institutions Law 2006 ("CBB Law"). The Directive in this Module is applicable to all

insurance licensees (including theirapproved persons ), and toregistered actuaries andloss adjusters .Amended: January 2011

Added: January 2007UG-A.1.6

For an explanation of the CBB’s rule-making powers and different regulatory instruments, see Section UG-1.1.

Added: January 2007UG-A.2 UG-A.2 Module History

UG-A.2.1

This Module was first issued in April 2005 by the BMA, together with the rest of Volume 3 (Insurance). Any material changes that have subsequently been made to this Module are annotated with the calendar date in which the change was made; Chapter UG-3 provides further details on Rulebook maintenance and version control.

Amended: January 2007UG-A.2.2

When the CBB replaced the BMA in September 2006, the provisions of this Module remained in force. Volume 3 was updated in January 2007 to reflect the switch to the CBB; however, new calendar quarter dates were only issued where the update necessitated changes to the actual requirements.

Added: January 2007UG-A.2.3

A list of recent changes made to this Module is provided below:

Module Ref. Change Date Description of Changes UG-A.1 01/2007 Updated to reflect new CBB Law, various references changed and new Rule UG-A.1.6 introduced categorising this Module as a Directive. UG-1.2 01/2007 New Rules UG-1.2.6 and UG-1.2.7 to reflect the CBB Law, other material reorderd as a consequence. UG-3.2.1 10/2007 Updated CBB policy re distribution of hard copies of Volumes of Rulebook. Order Form 10/2007 Amended Order Form to reflect new policy re hard copy availability. UG-A.1.5 01/2011 Clarified legal basis UG-2.1.2 01/2011 Updated to reflect structure of Volume 5. UG-A.1.2, UG-1.2.1, UG-1.2.2, UG-1.2.7, UG-2.1.1, UG-2.1.2, UG-2.1.3, and UG-2.2.2 10/2012 Various minor amendments to reflect the structure of the Rulebook, including the issuance of Volume 7. UG-3.2 and Annex 01/2013 Amended as CBB Rulebook only now available on CBB Website. UG-1.3.4 10/2016 Added Section to clarify reference to 'he' 'his' 'she' 'her'. UG-3.2.2 04/2020 Amended Paragraph. UG-A.2.4

Guidance on the implementation and transition to Volume 3 (Insurance) is given in Module ES (Executive Summary).

Superseded Requirements

Deleted: January 2007UG-A.2.3

Deleted: January 2007UG-1 UG-1 Rulebook Status and Application

UG-1.1 UG-1.1 Legal Basis

UG-1.1.1

Volume 3 (Insurance) of the CBB Rulebook is issued by the CBB pursuant to the Central Bank of Bahrain and Financial Institutions Law 2006 (‘CBB Law’). The CBB Law provides for two formal rulemaking instruments: Regulations (made pursuant to Article 37) and Directives (made pursuant to Article 38). Other articles in the CBB Law also prescribe various specific requirements (for example, requirements relating to licensing (Artilces 44 to 49), or the notification and approval of controllers of licensees (Articles 52 to 56)).

Amended: January 2007UG-1.1.2

The Purpose Section of each Module specifies in all cases the rulemaking instrument(s) used to issue the content of the Module in question, and the legal basis underpinning the Module’s requirements.

Amended: January 2007UG-1.1.3

The requirements for

representative offices will be covered as part of Volume 5 (Specialised activities) of the Rulebook and will be issued at a later date.Amended: January 2007

Amended: October 2007CBB's Rulemaking Instruments

UG-1.1.4

Regulations are made pursuant to Article 37 of the CBB Law. These instruments have general application throughout the Kingdom and bind all persons ordinarily affected by Bahraini legislative measures (i.e. residents and/or Bahraini persons wherever situated).

Added: January 2007UG-1.1.5

Because Regulations have wide general application, they are subject to two important safeguards: (i) the CBB is under a duty to consult with interested parties and to review their comments; and (ii) the finalised Regulations only become effective after they are published in the Official Gazette.

Added: January 2007UG-1.1.6

Directives are made pursuant to Article 38 of the CBB Law. These instruments do not have general application in the Kingdom, but are rather addressed to specific

licensees (or categories oflicensees ),approved persons orregistered persons . Directives are binding to whom they are addressed.Added: January 2007UG-1.1.7

Unlike Regulations, there is no duty on the CBB to either consult with addressees or publicise a Directive by publishing it in the Official Gazette (save that an addressee must obviously have actual or constructive notice of a Directive). However, as a matter of general policy, the CBB also consults on Rulebook content issued by way of a Directive.

Added: January 2007UG-1.1.8

All of the content of the CBB Rulebook has the legal status of at least a Directive, issued pursuant to Article 38 of the CBB Law. Certain of the requirements contained in the CBB Rulebook may also have the status of a Regulation, in which case they are also separately issued pursuant to Article 37 of the CBB Law and published in the Official Gazette. When this is the case, then the Rulebook crossrefers to the Regulation in question and specifies the requirements concerned.

Adopted: July 2007UG-1.1.9

In keeping with the nature of these regulatory requirements, Regulations are used to supplement the CBB Rulebook, either where explicitly required under the CBB Law, or where a particular requirement needs to have general applicability, in addition to being applied to licensees,

approved persons , or registered persons.Adopted: July 2007

Amended: October 2007UG-1.2 UG-1.2 Status of Provisions

UG-1.2.1

The contents of the CBB Rulebook are categorised either as Rules or as Guidance. Rules have a binding effect. If a licensee breaches a Rule to which it is subject, it is liable to enforcement action by the CBB and, in certain cases, criminal proceedings by the Office of the Public Prosecutor.

Amended: October 2012

Amended: January 2007UG-1.2.2

Guidance is not binding; rather, it is material that helps inform a particular Rule or sets of Rules, or provides other general information. Where relevant, compliance with Guidance will generally lead the CBB to assess that the rule(s) to which the Guidance relates has been complied with. Conversely, failure to comply with Guidance will generally be viewed by the CBB as tending to suggest breach of a Rule.

Amended: October 2012

Amended: January 2007UG-1.2.3

The status of each Paragraph within the Rulebook is identified by its text format, as follows:

• Rules are in bold, font size 12. The Paragraph reference number is also highlighted in a coloured box.• Guidance is in normal type, font size 11.

Amended: January 2007UG-1.2.4

Where there are differences of interpretation over the meaning of a Rule or Guidance, the CBB reserves the right to apply its own interpretation.

Amended: January 2007UG-1.2.5 [Deleted]

Deleted: January 2007UG-1.2.6 [Deleted]

Deleted: January 2007UG-1.2.7 [Deleted]

Deleted: January 2007UG-1.2.5

Rule UG-1.2.4 does not prejudice the rights of an authorised person to make a judicial appeal, should it believe that the CBB is acting unreasonably or beyond its legal powers.

Amended: January 2007UG-1.2.6

All Rulebook content has the formal status of at least a Directive. Some Rulebook content may also have the status of Regulations. Rulebook content that is categorised as a Rule is therefore legally mandatory and must be complied with by those to whom the content is addressed.

Added: January 2007UG-1.2.7

[This Paragraph was deleted in October 2012].

Deleted: October 2012

Added: January 2007UG-1.2.8

The CBB’s enforcement processes are set out in Module EN.

Added: January 2007UG-1.3 UG-1.3 Application

UG-1.3.1

Volume 3 of the CBB Rulebook for the most part applies to all

insurance licensees ; to individuals undertaking key functions in those licensees (so-called “approved persons”); and to certain support services (actuaries andloss adjusters ). (Representative offices are subject to the relevant requirements in Volume 5 of the CBB Rulebook). Further information and relevant definitions are provided in Module AU (Authorisation). Most of the content of Volume 3 only has the formal status of a Directive.Amended: January 2007

Amended: October 2007UG-1.3.2 [Deleted]

Deleted: January 2007UG-1.3.2

A few Rules and Guidance have general applicability (and thus also have the formal status of a Regulation); for instance, no one may carry on an insurance business within or from Bahrain without the appropriate license, and

controllers ofinsurance licensees are also subject to various requirements.Amended: January 2007

Amended: October 2007UG-1.3.3

Each Module in Volume 3 (except those listed under the 'Introduction' and 'Sector Guides' headings) contains a Scope of Application Chapter, setting out which Rules and Guidance apply to which particular type of

insurance licensee or person, for the Module concerned. In addition, each Rule, (or Section containing a series of Rules) is drafted such that its application is clearly highlighted for the user. Finally, each Module, in its Purpose Section, specifies in all cases the rulemaking instrument(s) used to issue the content of the Module in question, and the legal basis underpinning the Module’s requirements.Amended: January 2007UG-1.3.4

All references in this Module to 'he' or 'his' shall, unless the context otherwise requires, be construed as also being references to 'she' and 'her'.

Added: October 2016UG-1.4 UG-1.4 Effective Date

UG-1.4.1

Volume 3 (Insurance) of the CBB Rulebook was first issued in April 2005. Its contents have immediate effect, subject to transition arrangements that may be specified.

Amended: January 2007UG-1.4.2

Module ES (Executive Summary) contains details of the implementation and transition arrangements for Volume 3 (Insurance).

UG-2 UG-2 Rulebook Structure and Format

UG-2.1 UG-2.1 Rulebook Structure

Rulebook Volumes

UG-2.1.1

The Rulebook is divided into 7 Volumes, covering different areas of financial services activity, as follows:

Volume 1 Conventional Banks Volume 2 Islamic Banks Volume 3 Insurance Volume 4 Investment Business Volume 5 Specialised Activities Volume 6 Capital Markets Volume 7 Collective Investment Undertakings Amended: October 2012

Amended: January 2007UG-2.1.2

Volume 5 (Specialised Activities), covers money changers; financing companies;

representative offices ; administrators; trust service providers, micro-finance institutions and ancillary services providers.Amended: October 2012

Amended: January 2011

Amended: October 2007

Amended: January 2007Rulebook Contents (Overview)

UG-2.1.3

Except for Volumes 5, 6 and 7, the basic structure of each Rulebook is the same. Each Volume starts with a contents page and an introduction containing a User's Guide and Executive Summary. Subsequent material is organised underneath the following headings:

(a) High Level Standards;(b) Business Standards;(c) Reporting Requirements;(d) Enforcement and Redress; and, where appropriate,(e) Sector Guides.Amended: October 2012

Amended: January 2007

Amended: October 2007UG-2.1.4

Volume 5 is organised by the category of specialised firm concerned, whilst Volume 6 by subject area (authorised exchanges; issuers of securities, etc).

Amended: January 2007UG-2.1.5

The material in Volumes 1–4 is contained in Modules, each covering a specific area of requirements (e.g. capital). In turn, each Module is divided into Chapters, Sections and Paragraphs, as detailed below.

UG-2.1.6

Each Volume has its own appendix Volume containing relevant reporting and authorisation forms; a glossary; and any supplementary information. In all cases, the main Volume is called "Part A" and the appendix Volume is called "Part B".

UG-2.2 UG-2.2 Volume Structure

Modules

UG-2.2.1

Rulebook Volumes are subdivided into Modules, arranged in groups according to their subject matter, underneath the headings listed in Paragraph UG-2.1.3 above.

UG-2.2.2

Each Module in a Volume is referenced using a two-or three-letter code, which is usually a contraction or abbreviation of its title. These codes are used for cross-referencing within the text.

Amended: October 2012Chapters

UG-2.2.3

Each Module consists of Chapters, categorised into two types:

• A standard introductory Chapter (referenced with a letter: e.g. UG-A); andUG-2.2.4

The introductory Chapters summarise the purpose of the Module and its history (in terms of changes made to its contents). A separate introductory Chapter also prescribes the scope of application of the Module’s requirements.

Amended: January 2007Sections and Paragraphs

UG-2.2.5

Chapters are further sub-divided into Sections; these extend the Chapter numbering (e.g. FC-1.1, FC-1.2, FC-1.3 etc). In turn, Sections are sub-divided into Paragraphs; these extend the Chapter and Section numbering (e.g. FC-1.1.1, FC-1.1.2, FC-1.1.3 etc.). Where appropriate, sub-section headings may be used, to guide the reader through a Section; sub-section headings are italicised and unnumbered, and act purely as an indicator (without limitation), as to the status of the Paragraphs that follow.

Amended: January 2007Table of Contents

UG-2.2.6

Each Volume's contents page lists all the Modules contained within it (Part A), and the information contained in the relevant appendix Volume (Part B).

UG-2.2.7

The contents page of each Module lists the Chapters and Sections it contains, and the latest version date of each Section in issue.

Amended: January 2007UG-2.3 UG-2.3 Format and Page Layout

Headers

UG-2.3.1

The top of each page in the Rulebook identifies the Volume, Module and Chapter in question.

Footers

UG-2.3.2

The bottom of each page in the Rulebook (on the left hand side) identifies the Module in question, its section and page number. Page numbering starts afresh for each Section: the total number of pages in each Section is shown as well as the individual page number. The bottom right hand side shows an end-calendar quarter issue date. The contents page for each Module, and each Section in a Module, are each given their own issue date. In addition, the Module contents page lists the latest issue date for each Section in that Module. The contents page thus acts as a summary checklist of the current issue date in force for each Section. Further explanation is provided in Section UG-3.1 below.

Amended: January 2007Defined Terms

UG-2.3.3

Defined terms used in the Rulebook are underlined. Each Volume has its own glossary listing defined terms and giving their meaning. Definitions of terms used apply only to the Volume in question. It is possible for the same term to be used in a different Volume with a different meaning.

Amended: January 2007Cross-references

UG-2.3.4

Any cross-references given in a text state the Module code, followed (where appropriate) by the numbering convention for any particular Chapter, Section or Paragraph being referred to. For example, the cross-reference FC-1.2.3 refers to the third Paragraph in the second Section of the First Chapter of the Financial Crime Module. Many references will be quite general, referring simply to a particular Module, Chapter or Section, rather than a specific Paragraph.

Amended: July 2007Text format

UG-2.3.5

Each Paragraph is assigned a complete reference to the Module, Chapter, and Section, as well as its own Paragraph number, as explained in Paragraph UG-2.3.4 above. The format of the Paragraph reference and text indicates its status as either a Rule or Guidance, as explained in Paragraph UG-1.2.4 above.

Amended: July 2007UG-2.3.6

When cross-referring to specific Paragraphs, and it is important to make clear the status of the Paragraph in question as a Rule or Guidance, the words ‘Rule’ or ‘Guidance’ may be used instead of ‘Paragraph’, followed by the reference number (e.g. “As required by Rule FC-1.1.1, licensees must …”).

Amended: January 2007UG-3 UG-3 Rulebook Maintenance and Access

UG-3.1 UG-3.1 Rulebook Maintenance

Quarterly Updates

UG-3.1.1

Any changes to the Rulebook are generally made on a quarterly cycle (the only exception being when changes are urgently required) in early January, April, July and October. When changes are made to a Module, the amended Sections are given a new version date, in the bottom right-hand page.

Amended: January 2007UG-3.1.2

The contents page for each amended Module is also updated: the table of contents is changed to show the new version date for each amended Section (in the “date Last Changed” column), and the contents page itself is also given its own new version date in the bottom right-hand corner. The Module contents pages thus act as a checklist for hard-copy users to verify which are the current version dates for each Section in that Module.

Amended: January 2007UG-3.1.3

A summary of any changes made to a Module is included in the Module History Section of each Module. The table summarises the nature of the change made, the date of the change and, the Module components and relevant pages affected. The Module History can thus be used to identify which pages were updated within individual Sections.

Amended: July 2007UG-3.1.4

Hard-copy users of the CBB Rulebook can check that they have the latest copy of each Module’s contents pages, by referring to the overall table of contents for each Volume. The Volume table of contents lists the date each Module was last changed; users can use this table to check the date showing in the bottom right-hand corner of each Module’s contents page.

Amended: January 2007UG-3.1.5

The website version of the Rulebook acts at all times as the definitive version of the Rulebook. Any changes are automatically posted to the CBB website, together with a summary of those changes. Licensees are in addition e-mailed every quarter , to notify them of changes (if any). Hard-copy users are invited to print off the updated pages from the website to incorporate in their Rulebook in order to keep it current.

Amended: January 2007Changes to Numbering

UG-3.1.6

In order to limit the knock-on impact of inserting or deleting text on the numbering of text that follows the change, the following conventions apply:

(a) Where a new Paragraph is to be included in a Section, such that it would impact the numbering of existing text that would follow it, the Paragraph retains the numbering of the existing Paragraph immediately preceding it, but with the addition of an "A"; a second inserted Paragraph that follows immediately afterwards would be numbered with a "B", and so on.

For example, if a new Paragraph needs to inserted after UG-3.1.6, it would be numbered UG-3.1.6A; a second new Paragraph would be numbered UG-3.1.6B, and so on. This convention avoids the need for renumbering existing text that follows an insertion. The same principle is applied where a new Section or a new Chapter needs to be inserted: for example, UG-3.1A (for a new Section), and UG-3A (for a new Chapter).(b) Where a Paragraph is deleted, then the numbering of the old Paragraph is retained, and the following inserted in square brackets: "(This Paragraph was deleted in April 2006.)" ( The date given being the actual end-calendar quarter date of the deletion.) The same principle is applied with respect to Sections and Chapters.Amended: January 2007UG-3.1.7

Where many such changes have built up over time, then the CBB may reissue the whole section, Paragraph, Chapter or even Module concerned, consolidating all these changes into a renumbered version.

Amended: January 2007UG-3.2 UG-3.2 Rulebook Access

Availability

UG-3.2.1

The Rulebook is available on the CBB website.

Amended: January 2013

Amended: January 2007

Amended: October 2007Queries

UG-3.2.2

Questions regarding the administration of the Rulebook (e.g. ordering additional copies, website availability, the updating of material etc) should be addressed to the Rulebook Section of the Regulatory Policy Unit

Rulebook Section

Regulatory Policy Unit

Central Bank of Bahrain

PO Box 27

Manama

Kingdom of Bahrain

Tel: +973 - 17 54 7413

Fax: +973 - 17 53 0228

E-mail: rulebook@cbb.gov.bh

Web: www.cbb.gov.bhQuestions regarding interpretation of the policy and requirements contained in the Rulebook should be addressed to the licensee's regular supervisory point of contact within the CBB.

Amended: April 2020

Amended: January 2013

Amended: January 2007CBB Rulebook Order Form [This form was deleted in January 2013]

Deleted: January 2013ES ES Executive Summary

ES-A ES-A Introduction

ES-A.1 ES-A.1 Purpose

Executive Summary

ES-A.1.1

The purpose of this Module is to:

(a) Provide an overview of the structure of Volume 3 (Insurance);(b) Provide a summary of each Module; and(c) Outline the transition rules for the implementation of the Volume 3.Amended: January 2007ES-A.1.2

The Central Bank of Bahrain ('CBB'), in its capacity as the regulatory and supervisory authority for all financial institutions in Bahrain, has as its mission:

(a) To ensure monetary and financial stability in the Kingdom of Bahrain; and(b) To regulate, develop and maintain confidence in the financial sector.Amended: January 2007ES-A.1.3

As the single regulator, the CBB ensures the consistent application of regulatory standards in banking, insurance and capital markets, as well as encourages an open and cooperative approach in dealing with financial institutions.

Amended: January 2007ES-A.1.4

The supervision of the insurance sector in the Kingdom pays particular regard to the standards set by the International Association of Insurance Supervisors (IAIS). The CBB plays an important role in meeting stakeholders' expectations — the principal stakeholders of the CBB are the Government of the Kingdom of Bahrain, the regulated financial institutions, the consumers, the IAIS and several other international organizations.

Amended: January 2007ES-A.1.5

To carry out its responsibilities in relation to the insurance sector, the CBB has four supervisory objectives, namely to:

(a) Promote the stability and soundness in the insurance system;(b) Provide an appropriate degree of protection to insurance companypolicyholders ;(c) Promote transparency and market discipline; and(d) Reduce the likelihood ofinsurance licensees being used for financial crime (including money laundering activities).Amended: January 2007Legal Basis

ES-A.1.6

This Module contains the CBB's (as amended from time to time) Directive relating to transition rules and is issued under the powers available to the CBB under Article 38 of the Central Bank of Bahrain and Financial Institutions Law 2006 ('CBB Law'). The Directive in this Module is applicable to all

insurance licensees (including theirapproved persons ).Amended: January 2011

Amended: January 2007ES-A.1.7

For an explanation of the CBB's rule-making power and different regulatory instruments, see Section UG-1.1.

Amended: January 2007ES-A.2 ES-A.2 Module History

ES-A.2.1

This Module was first issued in April 2005 by the BMA together with the rest of Volume 3 (Insurance). Any material changes to that have subsequently been made to this Module are annotated with the calendar quarter date in which the change was made; Chapter UG-3 provides further details on Rulebook maintenance and version control.

Amended: January 2007ES-A.2.2

When the CBB replaced the BMA in September 2006, the provisions of this Module remained in force. Volume 3 was updated in January 2007 to reflect the switch to the CBB; however, new calendar quarter dates were only issued where the update necessitated changes to actual requirements.

Adopted: January 2007ES-A.2.3

A list of recent changes made to this Module is provided below:

Module Ref. Change Date Description of Changes ES-1.1 01/07/05 Module BR: Corrected first quarterly return due for the period ending 31 March 2006. ES-1.1 01/10/05 Clarified application of Module FC to insurance managers. ES-1.10 01/10/05 Corrected cross-reference referring to examples of suspicious transactions. ES-2.4 01/10/05 Added transition period for actuarial requirements for insurance firms whose long term insurance business is restricted to group life policies having a maturity of less than or equal to 1 year. ES-2.5 01/10/05 Corrected cross-reference. ES-2.6 01/10/05 Updated transition rules for minimum Tier 1 capital. ES-1.1 01/01/06 Transition rules for reporting by insurance firms updated. ES-2.7 01/01/06 A Section on transition rules for reporting by insurance firms was added. ES-1.1.5 01/07/06 Transition rule for Modules RM and PD has been added. ES-2.6A 01/07/06 Added transition rules for physical security measures and third party insurance. ES-2.8 01/07/06 Transition rules in respect of semi-annual disclosure requirements have been added. ES-A.1.6 01/2007 New Rule introduced, categorising this Module as a Directive. ES-1.1.9 and ES-2.4.2 01/2007 Clarified the first period for which a report from the Signing Actuary is required.ES-1.1.9 and ES-2.6B.1 01/2007 Allowed for a transition period for the external auditor's report required under Subparagraph FC-3.3.1(d). ES-1.1.9 10/2007 Minimum Tier 1 capital only applies to Bahraini insurance firms .ES-1.2.2 10/2007 Pure reinsurers can undertake both general insurance business andlong-term insurance business within the same entity.ES-2.4.3 10/2007 Clarified the transition period for the rotation of audit partner. ES-2.6.2 10/2007 Minimum Tier 1 capital only applies to Bahraini insurance firms .ES-1.1, ES-1.2, ES-1.11, ES-1.14 10/2009 Reference added to appointed representatives as per Resolution (11) of 2009. ES-1.2.3 10/2009 Amended list of controlled functions to be consistent with Module AU. ES-1.5.4 10/2009 Amended to be consistent with Section AA-4.2. ES-2.5.4 10/2009 Introduced transition rule for new requirements for appointed representatives as per Resolution (11) of 2009. ES-A.1.6 01/2011 Clarified legal basis ES1.1.9, ES-1.4, ES-1.17.3 and ES-2.3 04/2011 Amended to reflect changes to Module HC. ES-1.1.9, ES-1.8A and ES-2.6AA2 04/2012 Amendments made to reflect the issuance of Module CL (Client Money). ES-2.6AA1 04/2012 Added transition period to have in place customer complaints procedures as outlined in Chapter BC-4. ES-2.7.4 and ES-2.7.5 04/2012 Added transition period for filing of IBR and IBRS. ES-1.1.9

ES-1.1510/2012 The reference to Module DP was deleted as customer complaints procedures are included in Chapter BC-4. ES-1.1.9 04/2014 Updated transition period to repay/write of Qard Hassan granted for solvency purposes. ES-1.2.3 04/2014 Updated list of approved persons to be in line with AU-1.2.2. ES-1.7.5, ES-1.19.3, ES-2.4 and ES-2.6 04/2014 Updated to reflect the consultation on the enhanced operational and solvency framework for Takaful firms. ES-1 ES-1 Structure and Summary of Insurance Modules

ES-1.1 ES-1.1 Structure of Volume 3 (Insurance)

ES-1.1.1

Volume 3 (Insurance) of the Rulebook covers insurance activities, i.e. the provision of

regulated insurance services byinsurance licensees . It also includes requirements regardingapproved persons ; and the registration requirements foractuaries ,loss adjusters andappointed representatives .Amended: October 2009

Amended: January 2007ES-1.1.2

Volume 3 excludes

representative offices ofinsurance firms , andancillary services providers . These Regulations will later be incorporated into Volume 5 (Specialised Activities) of the CBB Rulebook, to be released at a later date.Adopted: January 2007

Amended: October 2007ES-1.1.3

Volume 3 (Insurance) is made up of two volumes: Part A is the main Volume containing detailed Modules containing the Rules and Guidance and Part B is an appendix Volume containing a glossary of defined terms, CBB authorisation forms, CBB reporting forms and any supplementary information.

Amended: January 2007ES-1.1.4

Part A of Volume 3 (Insurance) is organized under the following headings:

• Introduction;• High Level Standards;• Business Standards;• Reporting Requirements;• Enforcement and Redress; and• Sector Guides.Amended: January 2007

Amended: October 2007ES-1.1.5

Including this Executive Summary Module, there are 20 Modules that make up Part A of Volume 3 (Insurance). The requirements for the various insurance license categories are embedded throughout Part A. In addition, for some specialised licenses (

captive insurers ,insurance intermediaries andtakaful /retakaful ) there are sector guides summarizing the key requirements, specifically applicable to these categories.Amended: January 2007ES-1.1.6

Part B of Volume 3 is organized under the following headings:

• Glossary;• Reporting Forms; andAdopted: January 2007

Amended: October 2007ES-1.1.7

Defined terms used in the Rulebook are underlined; their definition can be found in the Glossary. Each volume has its own Glossary, as definitions of terms used apply only to the Volume in question. It is possible for the same term to be used in a different volume with a different meaning.

Adopted: January 2007ES-1.1.8

There are four authorisation forms, comprising (i) Form 1 (application for a license); (ii) Form 2 (application for the authorisation of a

controller ); (iii) Form 3 (application forapproved person status); and (iv) Form 4 (application for registration).Adopted: January 2007

Amended: October 2007ES-1.1.9

A summary of the Modules, their application and implementation is given in the table below:

Module Application Transition Rules Module AU All new applicants for licenses, approved persons and registration ofactuaries ,loss adjusters andappointed representatives .Effective 1 June 2005. AU-1.1.11 where an insurance licensee carries on a prohibited commercial business, the licensee must notify the CBB and establish the transitional rules. Module PB All insurance licensees andapproved persons .None.

Effective 1 June 2005.Module HC 1. Applies to allBahraini insurance licensees except for Bahraini single person companies.2. Insurance consultants, insurance managers and captive insurers are subject to Guidance under HC-10.3. Exemption possible from the requirement to have 2independent non-executive Directors forBahraini insurance licensees that are part of an overseas group and exemption to have Board Committees (HC-1.5.2).4. Where an insurance broker's Board does not consider it necessary to create an audit committee, it must be prepared to give reasons for its decision to the CBB (HC-B.1.2).The updated Module is effective on 1st January 2011. All insurance licensees to which Module HC applies must be in full compliance by the financial year end 2011.Module AA All insurance licensees —auditors

Allinsurance firms —actuaries For insurance firms whose business is restricted to group life policies, having a maturity of less than or equal to 1 year, actuarial requirements must be met by December 31, 2007.

The first period for which a report is required by aSigning Actuary is for the period ending December 31, 2008.

All other requirements are effective 1 July 2005.Module GR Refer to chart in GR-B.1.1 for application All insurance licensees must comply with the requirements for books and records within Bahrain, effective 1 July 2005.

Professional indemnity coverage must be met by allinsurance brokers andinsurance consultants by 31 Dec. 2005.

For unincorporated brokers licensed prior to 1 June 2005, professional indemnity coverage must be met by 31 Dec 2006.

All other provisions of Module GR are to be applied effective 1 June 2005.

Compliance with Resolution (11) of 2009 dealing withappointed representatives is effective 1st January 2010.Module CA All insurance licensees , with specific requirements applicable to different types of licensees.

Also special rules in place fortakaful firms .Minimum Tier 1 capital for Bahraini insurance firms to be met by December 31, 2007.

Forinsurance brokers licensed prior to 1 June 2005, implementation effective 31 Dec. 2006.

For Qard Hassan granted for solvency purposes, repayment or write off over a period of 5 years from April 2014.

For otherinsurance licensees licensed prior to 1 June 2005, implementation effective 31 Dec. 2005.Module BC Applicable to direct domestic business . Reinsurance business is exempted. Also special rules in place fortakaful firms .None.

Effective 1 July 2005.Module CL Applies to all insurance brokers and appointed representatives licensed by the CBB that undertake the broking of insurance contracts (see Rule AU-1.4.10) and hold client money. Effective 1 July 2012. Module RM Only applies to insurance firms andinsurance brokers .Physical Security Measures and Third Party Insurance are effective December 31, 2006. Module FC Measures for the prevention of money laundering and terrorism financing apply to insurance firms andinsurance brokers , with some exemptions forcaptive insurers managed by aninsurance manager . Wherecaptive insurers are managed by aninsurance manager , this Module also applies to theinsurance manager .

Some exemption possible for reinsurers (FC-B.1.2).

Measures dealing with fraud (FC-8) apply to allinsurance licensees .Effective 1 July 2005. For long-term insurance contracts, the CBB expects the Module to be applied to current clients gradually on a case by case basis. Module TC To be developed in the future. Module BR All insurance licensees , with specific requirements applicable to different types of licensees.For insurance firms , first annual and group reporting due for the period ending 31 December 2006 and first quarterly report due for the quarter ending 31 March 2007. Notification and approval requirements effective 1 June 2005.Module PD Only applies to insurance firms .First disclosure requirements required for the period ending 31 December 2005.

First semi-annual disclosure requirements required for the period ending 30 June 2008.Module EN All insurance licensees ,approved persons and registered persons.None.

Effective 1 June 2005.Module DP [Deleted as included in Chapter BC-4] Module CP To be developed in the future. Module CI Captive insurers Transition rules as per those stated in main Modules. Module IM Insurance intermediaries Transition rules as per those stated in main Modules. Module TA Takaful /retakaful Transition rules as per those stated in main Modules. Amended: April 2014

Amended: October 2012

Amended: April 2012

Amended: April 2011

Amended: October 2009

Amended: October 2007

Amended: January 2007ES-1.2 ES-1.2 Module AU — Authorisation

ES-1.2.1

Module AU covers the licensing requirements for

insurance licensees ; registration requirements foractuaries ,loss adjusters andappointed representatives ; and authorisation requirements forapproved persons . The Module defines what is included as part ofregulated services , specifically providing definitions for:(a) Carrying on of insurance business (insurance firms );(b) The broking of insurance contracts (insurance brokers );(c) The offering of insurance advice (insurance consultants );(d) The provision of insurance management services (insurance managers ); and(e) Operators of an insurance exchange (insurance exchange operators ).Amended: October 2009

Amended: October 2007

Amended: January 2007ES-1.2.2

With the exception of

captive insurers andpure reinsurers , aninsurance firm cannot undertake bothlong-term insurance business andgeneral insurance business .Insurance firms (includingcaptive insurers ), must operate on either conventional insurance principles or ontakaful principles: they cannot combine the two. Grandfathering provisions apply for those companies whose past license granted them the right to undertake bothlong-term insurance business and general business.Amended: January 2007

Amended: October 2007ES-1.2.3

Module AU deals with the requirements and conditions for

approved persons , i.e. those wishing to undertake acontrolled function in aninsurance licensee .Controlled functions are those of:(a)Director ;(b)Chief executive orgeneral manager ;(c)Head of function ;(d) Head of risk management;(e) Compliance officer;(f) Money Laundering Reporting Officer;(g) Member ofShari'a Supervisory Board ;(h) Internal Shari'a reviewer;(i)Unit-linked investment adviser ; and(j)Signing Actuary (where the function is undertaken by aDirector or anemployee of theinsurance firm ).Amended: April 2014

Amended: October 2009

Amended: January 2007ES-1.2.4

The licensing conditions that must be abided by all

insurance licensees are outlined as part of Chapter AU-2 of the Module.Amended: January 2007ES-1.2.5

The Module outlines the information requirements and procedures that must be followed as part of the process for:

(a) Licensing;(b)Approved persons ; and(c) Registration ofactuaries ,loss adjusters andappointed representatives .Amended: October 2009

Amended: January 2007ES-1.3 ES-1.3 Module PB — Principles of Business

ES-1.3.1

The 10 Principles of Business covered in Module PB are a general statement of the fundamental obligations of all CBB

insurance licensees andapproved persons . They have the status of Rules and provide a basis for other more detailed Rules elsewhere in Volume 3.Amended: January 2007ES-1.3.2

All Principles of Business apply to activities carried out by the licensees, including activities carried out through overseas branches. Principles 1 to 8 also apply to

approved persons , in respect ofcontrolled functions for which they have been approved. Principles 9 (Adequate Resources) and Principles 10 (Management, Systems and Controls) also take into account any activities of other members of the group of which the licensee is a member.Amended: January 2007ES-1.3.3

The Principles of Business are:

Principle 1 — Integrity

Principle 2 — Conflicts of Interest

Principle 3 — Due Skill, Care and Diligence

Principle 4 — Confidentiality

Principle 5 — Market Conduct

Principle 6 — Customer Assets

Principle 7 — Customer Interests

Principle 8 — Relations with Regulators/Supervisors

Principle 9 — Adequate Resources

Principle 10 — Management, Systems and Controls

ES-1.4 ES-1.4 Module HC — High-Level Controls

ES-1.4.1

Module HC outlines the requirements that must be met by

insurance licensees with respect to:(a) Corporate governance principles issued by the Ministry of Industry and Commerce as The Corporate Governance Code; and(b) Related high-level controls and policies.Amended: April 2011

Amended: January 2007ES-1.4.1A

The Principles referred to in this Module are in line with the Principles relating to the Corporate Governance Code issued by the Ministry of Industry and Commerce.

Added: April 2011ES-1.4.1B

The requirements distinguish between different types of

insurance licensees . Forinsurance brokers , Sections HC-3.2 Audit Committee and HC-3.3 Audit Committee Charter are to be considered as Guidance and the Comply or Explain Principle (see Paragraph HC-A.1.8) applies. In addition references to the Nominating and Remuneration Committees do not apply forinsurance brokers . Because of their limited business activities, and consequent lesser risk to customers,insurance consultants ,insurance managers andcaptive insurance firms are subject to applicable Guidance Paragraphs included in Chapter HC-10.Added: April 2011ES-1.4.2

The high-level controls covered by this Module deal with:

(a) The function ofchief executive officer andgeneral manager ;(b) The mapping of risks and responsibilities;(c) Internal audit;(d) Compliance;(e) Remuneration policies forapproved persons ;(f) Corporate ethics; and(g) Transparency and disclosure.(h) Committees of the Board;(i) Financial statements certification;(j) Appointment, training and evaluation of the Board;(k) Management structure;(l) Communication between the Board and shareholders; and(m) Governance and disclosure per Shari'a principles.Amended: April 2011

Amended: January 2007ES-1.4.3

Module HC also includes requirements for an annual Board review and certification, on the implementation of internal governance processes and their effectiveness in achieving the Board's objectives, and whether the Board can attest that it has fulfilled its responsibilities for directing and monitoring the overall conduct of the licensee's affairs.

ES-1.5 ES-1.5 Module AA — Auditors and Actuaries

ES-1.5.1

Module AA deals with requirements on the appointment and functions of

auditors andactuaries ofinsurance licensees . Requirements dealing withactuaries only apply toinsurance firms and are not applicable toinsurance intermediaries andinsurance managers .Amended: January 2007ES-1.5.2

The auditor requirements deal with:

(a) The appointment ofauditors ;(b) The removal and resignation ofauditors ;(c) Audit partner rotation;(d)Auditor independence; and(e) Restrictions on the relationship between theinsurance licensee and theauditor .Amended: January 2007ES-1.5.3

The Module covers the CBB's requirements regarding access to

auditors andactuaries as well as theauditors' access tooutsourcing providers . In addition, the Module outlines the requirement forinsurance licensees to arrange for theirauditors to review the licensee's annual return submitted to the CBB.Amended: January 2007ES-1.5.4

Module AA provides requirements for both

Registered Actuaries andSigning Actuaries .Amended: October 2009

Amended: January 2007ES-1.6 ES-1.6 Module GR — General Requirements

ES-1.6.1

Module GR covers requirements dealing with areas not covered in other Modules. The areas covered are:

(a) Books and records;(b) Corporate and trade names;(c) Dividends;(d) Business transfers;(e)Controllers ;(f) Close links;(g) Statutory deposits and compulsory reserve;(h) Cessation of business;(i)Appointed representatives ; and(j) Professional indemnity coverage.Amended: January 2007

Amended: October 2007ES-1.6.2

Item (i) applies only to

insurance firms ; item (g) applies toinsurance firms andinsurance brokers , whereas item (j) only applies toinsurance brokers andinsurance consultants .Amended: January 2007

Amended: October 2007ES-1.7 ES-1.7 Module CA — Capital Adequacy

ES-1.7.1

Module CA covers requirements governing the minimum capital and solvency requirements as well as the valuation of assets and liabilities.

Amended: January 2007ES-1.7.2

Considering the nature of their business, the requirements regarding capital and solvency for

insurance firms are far more detailed than forinsurance intermediaries andinsurance managers .Amended: January 2007ES-1.7.3

Similarly the rules dealing with the valuation of assets and valuation of liabilities are only applicable to

insurance firms .Amended: January 2007ES-1.7.4

For

insurance firms , Module CA outlines various currency matching and localisation requirements as well as whole firm and group solvency requirements.Amended: January 2007ES-1.7.5

The Module provides detailed rules for requirements dealing with

takaful andretakaful specifically addressing:(a) General capital requirements;(b) The basis of operating atakaful business;(c) The segregation of funds;(d) The capital adequacy and solvency requirements forboththeTakaful firm ; and(e) The distribution of surplus.Amended: April 2014

Amended: January 2007ES-1.8 ES-1.8 Module BC — Business Conduct

ES-1.8.1

This Module presents under the form of an Insurance Code of Practice the minimum standards of good practice for market conduct in relation to direct insurance activities. This Module applies to

domestic business .Reinsurance business is exempted from the requirements of this Module.Amended: January 2007ES-1.8.2

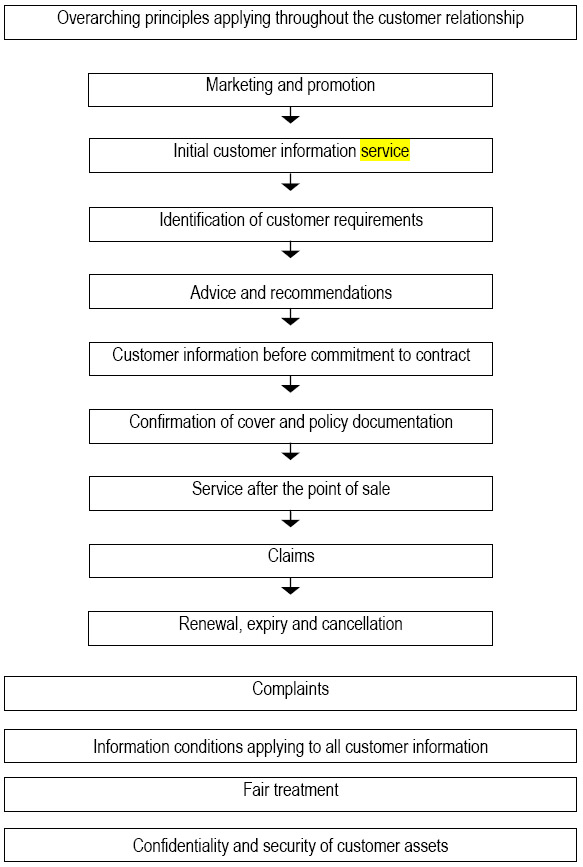

The Insurance Code of Practice is made up of overarching principles applied throughout the customer relationship. These principles cover:

(a) Marketing and promotion;(b) Initial customer information service;(c) Identification of customer requirements;(d) Advice and recommendation;(e) Customer identification before commitment to contract;(f) Confirmation of cover and policy documentation;(g) Service after the point of sale;(h) Claims;(i) Renewal, expiry and cancellation;(j) Complaints;(k) Information conditions applying to all customer information;(l) Fair treatment; and(m) Confidentiality and security of customer assets.Amended: January 2007ES-1.8.3

Module BC has additional requirements dealing specifically with requirements unique to

takaful andretakaful , including the requirement to clearly disclose to participants the calculation of wakala and mudaraba fees paid by thetakaful fund(s) to thetakaful operator.Amended: January 2007ES-1.8A ES-1.8A Module CL – Client Money

ES-1.8A.1

This Module provides detailed Rules and Guidance with respect to the holding of

client money byinsurance brokers andappointed representatives . They are aimed at ensuring proper protection ofclient money to minimise the risk ofclient money being used byinsurance brokers andappointed representatives and to prevent the commingling ofclient money with theinsurance brokers' andappointed representatives' assets.Added: April 2012ES-1.8A.2

As a general rule,

client monies are required to be segregated from a firm's own assets, andclient money must be held in aclient money account . Various other restrictions and protections apply toclient money , whilst the rules also apply certain reconciliation and reporting requirements.Added: April 2012ES-1.8A.3

Rules applying to

appointed representatives are applicable based on the type ofappointed representatives . The Module deals with:(a) Individualappointed representatives ;(b) Corporateappointed representatives that are financial institutions; and(c) Corporateappointed representatives , other than financial institutions.Added: April 2012ES-1.9 ES-1.9 Module RM — Risk Management

ES-1.9.1

This Module provides detailed Rules and Guidance on risk management systems and controls required for

insurance firms andinsurance brokers . The Module imposes on these licensees the obligation to identify the range of risks that they face and to effectively manage these through the implementation of risk management systems that monitor and control all material risks.Amended: January 2007ES-1.9.2

Module RM specifically addresses certain risk categories. However,

insurance firms andinsurance brokers must determine any additional risk categories relevant to their business and how these are addressed.Amended: January 2007ES-1.9.3

The risk management standards addressed in Module RM are:

(a)Credit risk ;(b)Liquidity risk ;(c)Market risk ;(d)Insurance technical risk ;(e)Operational risk ;(f)Outsourcing risk ; and(g) Group risk.Amended: January 2007

Amended: October 2007ES-1.10 ES-1.10 Module FC — Financial Crime

ES-1.10.1

Module FC implements the Financial Action Task Force (FATF) recommendations on money laundering and special recommendations on terrorism financing that are relevant to the insurance sector in Bahrain.

ES-1.10.2

The Module covers the detailed procedures required for:

(a) Customer identification;(b) Reporting;(c) Staff awareness and training;(d) The appointment of a money laundering reporting officer;(e) Compliance monitoring;(f) Record keeping arrangements;(g) Segregation of duties;(h) Special measures for non-cooperative countries; and(i) Contact with relevant authorities.Amended: January 2007ES-1.10.3

Item FC (iv) in Part B of Volume 3 (Insurance) provides further examples of transactions that may be suspicious or unusual.

ES-1.10.4

In addition, Module FC has a chapter dealing with the area of insurance fraud and steps that must be taken by

insurance licensees to address this area.Amended: January 2007ES-1.11 ES-1.11 Module TC — Training and Competency

ES-1.11.1

This Module is to be issued at a later date.

Amended: January 2007

Amended: October 2007ES-1.11.2

When finalised, the Module will provide detailed Rules and Guidance on training and competency requirements for employees of

insurance licensees as well as foractuaries ,loss adjusters andappointed representatives .Amended: October 2009

Amended: January 2007ES-1.12 ES-1.12 Module BR — BMA Reporting

ES-1.12.1

Module BR outlines the CBB's reporting requirements. The reporting requirements are broken down into three main categories:

(a) Financial reporting;(b) Notifications; and(c) Approvals.Amended: January 2007ES-1.12.2

Annual financial reporting is required for all

insurance licensees . Group and quarterly reporting are required only forinsurance firms . The financial reporting Chapter contains various Rules, Directives and Guidance which underpin the reporting forms included in Part B of Volume 3 (Insurance).Amended: January 2007

Amended: October 2007ES-1.12.3

The Module outlines instances and procedures to be followed where

insurance licensees must submit written notifications to the CBB. These include matters having a serious supervisory impact, breaches of Regulations and Directives and other requirements and the removal or resignation ofauditors orReporting Actuaries .Amended: January 2007ES-1.12.4

The Module also outlines where

insurance licensees must seek the CBB's prior approval for changes in their operations, such as change in legal status, mergers, acquisitions, disposals and establishment of new subsidiaries. The CBB's prior approval is also required forinsurance licensees undertaking business transfers and forrelated party transactions above a specified threshold.Amended: January 2007

Amended: October 2007ES-1.12.5

Finally, the Module outlines the various ways in which the CBB gathers its information from

insurance licensees including onsite visits by the CBB, and where deemed necessary the use ofAppointed Experts .Amended: January 2007ES-1.13 ES-1.13 Module PD — Public Disclosure

ES-1.13.1

Module PD governs the minimum requirements to be followed by

insurance firms with respect to corporate and financial transparency through meaningful public disclosures. Public disclosures help protectcustomers ofinsurance firms and facilitate market discipline.Amended: October 2007ES-1.13.2

The disclosure requirements for

insurance firms cover both annual and semi-annual disclosure requirements.ES-1.13.3

Module PD outlines what information and by what means this information must be disclosed, distinguishing the type of information to be disclosed by the

insurance firm subject to these requirements.ES-1.13.4

To assist those

insurance firms subject to this Module wishing to go further than the CBB's minimum requirements, further guidance and best practice are set out in Chapter PD-3.Amended: January 2007ES-1.14 ES-1.14 Module EN — Enforcement

ES-1.14.1

This Module outlines enforcement powers and processes that may be applied by the CBB to address failures by

insurance licensees ,approved persons or registered persons. The purpose of such measures is to encourage a high standard of compliance by all those authorised by the CBB, thus reducing risk topolicyholders and the financial system.Amended: January 2007ES-1.14.2

The enforcement measures contained in the Module are of varying severity and will be used in keeping with the CBB's assessment of the contravention, reserving the most serious enforcement measures for the most serious of contraventions.

Amended: January 2007ES-1.14.3

The CBB follows a proportionality principle in its enforcement measures, and will usually opt for the least severe of appropriate enforcement measures, consistent with the desired outcome. The CBB's enforcement approach includes:

(a) Formal requests for information;(b) Investigations;(c) Formal warnings;(d) Directions;(e) Financial penalties;(f) Administration;(g) Cancellation of license;(h) Cancellation of "fit and proper" approval; and(i) Cancellation of registration (foractuaries ,loss adjusters andappointed representatives only).Amended: October 2009

Amended: January 2007ES-1.14.4

A reminder of criminal sanctions in the CBB Law and other legislation is set out in Chapter EN-10.

Amended: January 2007ES-1.15 ES-1.15 [This Section was deleted in October 2012 as it is included in Chapter BC-4]

ES-1.15.1

[This Paragraph was deleted in October 2012].

Deleted: October 2012

Amended: January 2007

Amended: October 2007ES-1.15.2

[This Paragraph was deleted in October 2012].

Deleted: October 2012

Adopted: January 2007ES-1.16 ES-1.16 Module CP — Compensation

ES-1.16.1

This Module provides space, for possible inclusion at a later date, for a description of a

policyholder protection scheme, should such a scheme be developed in cooperation with the industry.Amended: January 2007ES-1.17 ES-1.17 Module CI — Captive Insurers

ES-1.17.1

This Module provides a summary of Rules and Guidance applicable to

captive insurance firms , that are contained in the main subject Modules of Volume 3 (Insurance). Module CI (Captive Insurers) only contains Guidance material.Amended: January 2007ES-1.17.2

While Module CI is primarily focused for

captive insurers , it contains the requirements that would need to be fulfilled by captive management firms (insurance managers ), in meeting the regulatory obligations ofcaptive insurers .Amended: January 2007ES-1.17.3

The Module extracts several of the rules applicable to

captive insurers , and tailored to meet the unique nature ofcaptive insurers , including:(a) The option to be licensed as a special purpose vehicle (SPV), specifically established to carry out the activities of acaptive insurer (Module AU);(b) Lighter requirements with respect to high-level controls (Module HC);(c) Exemptions to rules in respect of due diligence requirement for client records, approval for corporate and trade names and pre-approval for distribution of dividends toshareholders (Module GR);(d) Capital requirements based on the type (Category C1 orCategory C2 firm) ofcaptive insurers (Module CA);(e) Exemptions from quarterly and group financial reporting (Module BR); and(f) The non-application of public disclosure requirements forcaptive insurers (Module PD).Amended: April 2011

Amended: January 2007

Amended: October 2007ES-1.18 ES-1.18 Module IM — Insurance Intermediaries and Managers

ES-1.18.1

This Module provides a summary of Rules and Guidance applicable to

insurance intermediaries (insurance brokers andinsurance consultants ) andinsurance managers , that are contained in the main subject Modules of Volume 3 (Insurance). Module IM (Insurance Intermediaries and Managers) only contains Guidance material.Amended: January 2007ES-1.18.2

The

regulated insurance services ofinsurance consultants andinsurance managers are defined in Section AU-1.4, detailing the type of services that can be offered by these intermediaries.Amended: January 2007ES-1.18.3

The category of

insurance manager is being introduced in the Rulebook, as the CBB has also introduced a regulatory framework to cater to the unique nature ofcaptive insurers . The CBB recognises that, in most cases, the operations ofcaptive insurers are sub-contracted toinsurance managers . To simplify the approval of the management subcontracted by acaptive insurer , the licensing ofinsurance managers will have been considered by the CBB in detail as part of its licensing process.Amended: January 2007ES-1.18.4

The Module extracts the rules applicable to

insurance intermediaries andinsurance managers , including:(a) The requirements to have in place professional indemnity coverage forinsurance brokers andinsurance consultants . (Module GR);(c) Exemptions from quarterly and group financial reporting (Module BR).Amended: January 2007

Amended: October 2007ES-1.19 ES-1.19 Module TA — Takaful/retakaful

ES-1.19.1

This Module provides a summary of Rules and Guidance applicable to

takaful andretakaful business that are contained in the main subject Modules of Volume 3 (Insurance). Module TA (Takaful/retakaful) only contains Guidance material.Amended: January 2007ES-1.19.2

Module TA recognises the unique nature of the

takaful /retakaful business and has carved out Rules in instances where conventional Rules could not be applied to atakaful entity.Amended: January 2007ES-1.19.3

Included in the Rules tailored to meet the requirements of the

takaful industry are:(a) The requirement fortakaful firms to have aShari'a Supervisory Board in addition to a Board of Directors (Module HC); and(b) Capital and solvency Rules taking into account the participants' funds and the possibility of Qard Hassan from the shareholder fund in instances where thetakaful fund does not fully meet the liquidity requirements (Module CA).Amended: April 2014

Amended: January 2007ES-2 ES-2 Transition Rules

ES-2.1 ES-2.1 General Requirements

ES-2.1.1

Insurance licensees who were licensed prior to the publication of Volume 3 (Insurance), do not need to resubmit an application for a license.ES-2.1.2

Insurance licensees licensed prior to 1 June 2005 will have their license category, and the scope of their authorisation, confirmed in an exchange of letters.Amended: January 2007ES-2.1.3

Insurance licensees licensed prior to 1 June 2005, must comply with all other requirements of the Rulebook, when these take effect on 1 June 2005, unless different transition arrangements have been agreed in writing with the CBB beforehand or in accordance with the transition rules incorporated throughout in this Module.Amended: January 2007ES-2.2 ES-2.2 Module AU — Authorisation

ES-2.2.1

In instances where an

insurance licensee carries on a commercial business, at the time where the Insurance Rulebook becomes effective, theinsurance licensee must notify the CBB to establish the transitional rules in relation to this prohibited activity (refer to AU-1.1.11).Amended: January 2007ES-2.3 ES-2.3 Module HC — High-Level Controls

ES-2.3.1

Insurance brokers who were licensed prior to the introduction of Volume 3 (Insurance), and who were unincorporated entities or natural persons at that time, may continue as such until 31 December 2006.ES-2.3.2

[This Paragraph was deleted in April 2011].

Deleted: April 2011

Amended: January 2007ES-2.3.3

The updated Module is effective on 1st January 2011. All

insurance licensees to which Module HC applies must be in full compliance by the financial year end 2011.Added: April 2011ES-2.4 ES-2.4 Module AA — Auditors and Actuaries

ES-2.4.1

[This Paragraph was deleted in April 2014.]

Deleted: April 2014

Amended: July 2007ES-2.4.2

[This Paragraph was deleted in April 2014.]

Deleted: April 2014

Amended: April 2008

Adopted: January 2007ES-2.4.3

The first five year-period where the requirement for the rotation of audit partner referred to in Paragraph AA-1.3.1 takes effect, ends 31 December 2010. Therefore, unless there has been a change in the partner appointed since the Rulebook was issued in May 2005, or if a company has been licensed since the Rulebook has been issued, insurance licensees will need to have a new partner responsible for the audit engagement for the year 2011.

Adopted: October 2007ES-2.5 ES-2.5 Module GR — General Requirements

Books and Records (GR-1)

ES-2.5.1

All

insurance licensees must comply with the requirements for books and records outlined in Chapter GR-1, effective 1 July 2005.Professional Indemnity Coverage (GR-10)

ES-2.5.2

Except as provided for by Paragraph ES-2.5.3, professional indemnity coverage requirements must be met by

insurance brokers andinsurance consultants by 31 December 2005.ES-2.5.3

Unincorporated

Bahraini insurance brokers licensed prior to 1 June 2005 must meet the professional indemnity coverage requirements by 31 December 2006.Appointed Representatives (GR-9)

ES-2.5.4

Requirements for the registration of appointed representatives and minimum qualifications as outlined in Chapter GR-9 are effective 1st January 2010.

Adopted: October 2009ES-2.6 ES-2.6 Module CA — Capital Adequacy

ES-2.6.1

Except as otherwise noted below, the requirements of Module CA are to be implemented, effective 31 December 2005.

Insurance Firm

ES-2.6.2

Bahraini insurance firms licensed prior to 1 April 2005 that do not meet the requirements of Paragraph CA-1.2.1, will be required to meet the requirements for minimum Tier 1 capital by 31 December 2007. In addition, the requirements to maintain a capital available in excess of the greater of the Required Solvency Margin and minimum fund must be met byinsurance firms by 31 December 2005.Insurance firms who are in run-off and whose license is restricted from entering into new contracts of insurance as per Paragraph GR-8.1.8, are grandfathered and not required to apply the requirements of Paragraph CA-1.2.1.Amended: January 2007

Amended: October 2007Insurance Broker

ES-2.6.3

In respect of licensees who were carrying out activities that fall within the definition of the regulated activity of

insurance broker prior to 1 April 2005, the requirements of Paragraph CA-1.3.1 (capital requirements) will apply from 1 January 2007.Amended: January 2007Takaful Firms

ES-2.6.4

Where a

takaful firm was licensed prior to the Rulebook coming into force, Section ES-2.6.5 applies.Amended: April 2014

Amended: October 2007

Amended: January 2007ES-2.6.5

A

takaful firm operating on a basis other than that prescribed by Paragraph CA-8.2.1 at the date the Rulebook comes into force, must in respect of alltakaful contracts written after this date, manage those contracts in accordance with Paragraph CA-8.2.1.Takaful contracts written before this date hereafter referred to as pre-existing contracts, must continue to be managed in accordance with thetakaful model or models operated by thetakaful firm prior to Paragraph CA-8.2.1 coming into force, until such time as all obligations of thetakaful fund or funds under those pre-existing contracts have been discharged in full.Amended: April 2014

Amended: October 2007

Amended: January 2007ES-2.6.6

[This Paragraph was deleted in April 2014.]

Deleted: April 2014

Amended: January 2007ES-2.6.7

[This Paragraph was deleted in April 2014.]

Deleted: April 2014

Amended: October 2007

Amended: January 2007ES-2.6.8

[This Paragraph was deleted in April 2014.]

Deleted: April 2014

Amended: January 2007ES-2.6AA1 ES-2.6AA1 Module BC – Business Conduct

ES-2.6AA1.1

All

insurance licensees must have appropriate customer complaints handling procedures and systems for effective handling of complaints made by customers by 31st March 2012.Added: April 2012ES-2.6AA2 ES-2.6AA2 Module CL – Client Money

ES-2.6A ES-2.6A Module RM — Risk Management

ES-2.6B ES-2.6B Module FC — Financial Crime

ES-2.6B.1

For the year ending 31 December 2006,

insurance licensees must submit the report required as per Paragraph FC-3.3.1 (d), no later than 30 June 2007.Adopted: January 2007ES-2.7 ES-2.7 Module BR — CBB Reporting

ES-2.7.1

The first Insurance Firm Return (IFR) for both

conventional insurance firms andtakaful firms , required under Section BR-1.1, must be submitted to the CBB for the financial year ending 31 December 2006.Amended: January 2007ES-2.7.2

The first Group Insurance Firm Return (GIFR) for

insurance firms , required under Section BR-1.3, must be submitted to the CBB for the financial year ending 31 December 2006.Amended: January 2007ES-2.7.3

The first quarterly return (IFRQ) for insurance firms, required under Section BR-1.4, must be submitted to the CBB for the quarter ending 31 March 2007.

Amended: January 2007ES-2.7.4

The first annual return (IBR) for

insurance brokers , required under Section BR-1.2A, must be submitted to the CBB for the semi-annual period ending 31 December 2012.Added: April 2012ES-2.7.5

The first semi-annual return (IBRS) for

insurance brokers , required under Section BR-1.4A, must be submitted to the CBB for the semi-annual period ending 30 June 2012.Added: April 2012ES-2.8 ES-2.8 Module PD — Public Disclosure

ES-2.8.1

For purposes of Chapter PD-2, semi-annual disclosure requirements are effective for the period ending 30 June 2008.

Amended: January 2007High Level Standards

AU AU Authorisation

AU-A AU-A Introduction

AU-A.1 AU-A.1 Purpose

Executive Summary

AU-A.1.1

The Authorisation Module sets out the Central Bank of Bahrain's (CBB) approach to licensing providers of

regulated insurance services in the Kingdom of Bahrain. It also sets out CBB requirements for approving persons undertaking key functions in those providers. Finally, it sets out requirements for registering certain support services (actuaries ,loss adjusters andappointed representatives ).Amended: October 2011

Amended: October 2009

Amended: July 2007AU-A.1.2 [Deleted]

Deleted July 2007AU-A.1.2

Persons who provide any of the following

regulated insurance services within or from the Kingdom of Bahrain require a license:(a) The carrying on of insurance business;(b) The broking of insurance contracts;(c) The offering of advice to third parties regarding individual insurance requirements and products;(d) The provision of insurance management services (such as captive managers); and(e) The operating of a recognised insurance exchange.Amended: July 2007AU-A.1.3

The categories of

regulated insurance services listed in AU-A.1.2 in turn determine the license category of the provider. The requirements in Volume 3 (Insurance) are tailored in certain respects, according to the license category concerned, in order to address the specific features and risks associated with each type ofregulated insurance services .Amended: July 2007AU-A.1.4

For the purposes of Volume 3 (Insurance), providers licensed to undertake activities falling under AU-A.1.2 (a) are categorised as '

insurance firms '; those under (b), as 'insurance brokers '; those under (c), as 'insurance consultants '; those under (d), as 'insurance managers '; and those under (e), as 'insurance exchange operators '. A provider ofregulated insurance services can only hold one of the above license categories; different categories may not be combined.Amended: July 2007AU-A.1.5

Collectively, licensed providers of

regulated insurance services are calledinsurance licensees . Bahrain-incorporatedinsurance licensees are calledBahraini insurance licensees .Insurance licensees that are incorporated in an overseas jurisdiction and operate via a branch presence in the Kingdom of Bahrain are calledoverseas insurance licensees . The same naming convention applies to the various categories of license holders: for example,Bahraini insurance brokers are incorporated in Bahrain andoverseas insurance brokers operate via a branch presence.Amended: July 2007Licensing

Approved Persons

AU-A.1.6

Persons undertaking certain functions in relation to CBB

insurance licensees require prior CBB approval. These functions (called 'controlled functions ') includeDirectors and members of senior management. Thecontrolled functions regime supplements the licensing regime by ensuring that key persons involved in the running ofinsurance licensees are fit and proper. Those authorised by the CBB to undertakecontrolled functions are calledapproved persons .Amended: July 2007Registration

AU-A.1.7

Persons wishing to carry on the business of an

actuary ,loss adjuster orlicensed principal wishing to appointappointed representative within the Kingdom of Bahrain are required to register with the CBB. Registrants are subject to basic screening to verify their expertise and general suitability, at the point of application. Unlikeinsurance licensees , they are not subject to detailed Directives and Regulations and continuous, risk-based supervision.Amended: October 2009

Amended: July 2007Retaining Authorised Status

Ancillary Services Providers

AU-A.1.9

Ancillary services providers are not covered in Volume 3 (Insurance) of the Rulebook. Requirements covering these types of activities will instead be included in Volume 5.Amended: October 2011

Amended: July 2007AU-A.1.10

Until such time as Volume 5 (Specialised Activities) of the CBB Rulebook is issued,

ancillary services providers remain subject to the requirements contained in the CBB's 'Standard Conditions and Licensing Criteria', a copy of which is available from the CBB Licensing Directorate.Amended: April 2018

Amended: October 2011

Amended: July 2007AU-A.1.11

[This Paragraph was merged with Paragraph AU-A.1.9 above, in January 2007].

Amended: July 2007AU-A.1.12

[This Paragraph was merged with Paragraph AU-A.1.10 above, in January 2007]

Amended: July 2007Legal Basis

AU-A.1.13

This Module contains the CBB's Regulations, Resolutions and Directive (as amended from time to time) regarding authorisation requirements applicable to

insurance licensees ,approved persons and registered bodies and is issued under the powers available to the CBB under Articles 37 to 42, 44 to 48 and 180 of the Central Bank of Bahrain and Financial Institutions Law 2006 ('CBB Law'). Requirements regarding regulated insurance services as per Article 39 (see Chapter AU-1), licensing conditions and processes as per Articles 44 to 48 (see Chapters AU-2 and AU-5) and licensing and registrations fees as per Article 180 (see Chapter AU-6) are also included in Resolutions and included in this Module. Module AU includes the requirements contained in Resolution No (1) of 2007 with respect to determining fees categories due for licensees and services provided by the CBB. Module AU also contains the minimum qualifications and fit and proper requirements forappointed representatives issued in 2009 under Resolution 11 in accordance with Article 74 of the CBB Law. The Module contains requirements governing the conditions of granting a license for the provision of regulated services as prescribed under Resolution No (43) of 2011 and issued under the powers available to the CBB under Article 44(c). Finally, the Module contains requirements under Resolution No.(16) for the year 2012 including the prohibition of marketing financial services pursuant to Article 42 of the CBB Law. This Module contains the prior approval requirements for approved persons under Resolution No (23) of 2015.Amended: July 2015

Amended: January 2013

Amended: October 2011

Amended: January 2011

Amended: October 2009

Added: July 2007AU-A.1.14

For an explanation of the CBB’s rule-making powers and different regulatory instruments, see Section UG-1.1.

Added: July 2007AU-A.2 AU-A.2 Module History

AU-A.2.1

This Module was first issued in April 2005 by the BMA, together with the rest of Volume 3 (Insurance). Any material changes that have subsequently been made to this Module are annotated with the calendar quarter date in which the change was made. UG-3 provides further details on Rulebook maintenance and version control.

Amended: July 2007AU-A.2.2

When the CBB replaced the BMA in September 2006, the provisions of this Module remained in force. Volume 3 was updated in January 2007 to reflect the switch to the CBB; however, new calendar quarter dates were only issued where these involved changes in the substance of Rules.

Added: July 2007AU-A.2.3

A list of recent changes made to this Module is provided below: