CA-6.4.81

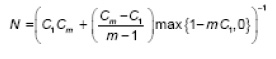

Under the conditions provided below, banks may employ a simplified method for calculating the effective number of exposures and the exposure-weighted average LGD. Let Cm in the simplified calculation denote the share of the pool corresponding to the sum of the largest 'm' exposures (e.g. a 15% share corresponds to a value of 0.15). The level of m is set by each bank:

(a) If the portfolio share associated with the largest exposure, C1, is no more than 0.03 (or 3% of the underlying pool), then for purposes of the SF, the bank may set LGD=0.50 and N equal to the following amount:

5.

(b) Alternatively, if only C1 is available and this amount is no more than 0.03, then the bank may set LGD=0.50 and N=1/ C1.

Amended: April 2011

Apr 08

Apr 08