CA-6.4.79

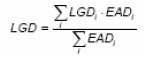

The exposure-weighted average LGD is calculated as follows:

4.

where LGDI represents the average LGD associated with all exposures to the ith obligor. In the case of re-securitisation, an LGD of 100% must be assumed for the underlying securitised exposures. When default and dilution risks for purchased receivables are treated in an aggregate manner (e.g. a single reserve or over-collateralisation is available to cover losses from either source) within a securitisation, the LGD input must be constructed as a weighted-average of the LGD for default risk and the 100% LGD for dilution risk. The weights are the stand-alone IRB capital charges for default risk and dilution risk, respectively.

Apr 08