BC BC Business and Market Conduct

BC-A BC-A Introduction

BC-A.1 BC-A.1 Purpose

Executive Summary

BC-A.1.1

This Module presents requirements that have to be met by

insurance licensees with regards to their dealings withcustomers . Reinsurance business is exempted from the scope of these requirements.BC-A.1.2

The requirements contained in this Module aim to ensure that

insurance licensees deal with theircustomers in a fair and open manner, and address theircustomers' information needs.Amended: January 2007BC-A.1.3

The requirements build upon several of the Principles of Business (see Module PB (Principles of Business)). Principle 1 (Integrity) requires

insurance licensees to observe high standards of integrity and fair dealing, and to be honest and straightforward in their dealings withcustomers . Principle 7 (Customer Interests), requiresinsurance licensees to pay due regard to the legitimate interests and information needs of theircustomers , and to communicate with them in a fair and transparent manner.Amended: January 2007BC-A.1.4

The requirements contained in this Module are largely principles-based and focus on desired outputs rather than on prescribing detailed processes. This gives

insurance licensees flexibility in how to implement the basic standards prescribed in this Module.Amended: January 2007Legal Basis

BC-A.1.5

This Module contains the Central Bank of Bahrain's ('CBB') (as amended from time to time) Directive relating to business conduct and is issued under the powers available to the CBB under Article 38 of the Central Bank of Bahrain and Financial Institutions Law 2006 ('CBB Law'). The Directive in this Module is applicable to

insurance licensees (including theirapproved persons ).Amended: January 2011

Added: January 2007BC-A.1.6

For an explanation of the CBB’s rule-making powers and different regulatory instruments, see Section UG-1.1.

Added: January 2007BC-A.2 BC-A.2 Module History

BC-A.2.1

This Module was first issued in April 2005 by the BMA, together with the rest of Volume 3 (Insurance). Any material changes that have been subsequently been made to this Module are annotated with the calendar quarter date in which the change was made: Chapter UG-3 provides further details on Rulebook maintenance and version control.

Amended: January 2007BC-A.2.2

When the CBB replaced the BMA in September 2006, the provisions of this Module remained in force. Volume 3 was updated in January 2007 to reflect the switch to the CBB; however, new calendar quarter dates were only issued where the update necessitated changes to actual requirements.

Added: January 2007BC-A.2.3

A list of recent changes made to this Module is detailed in the table below:

Module Ref. Change Date Description of Changes BC-3.4 01/07/05 Clarified language of takaful disclosure. BC-A.1.5 01/2007 New Rule introduced, categorising this Module as a Directive. BC-A.1.5 01/2011 Clarified legal basis BC-2.11 and BC-4 10/2011 Replaced Complaints Section BC-2.11 with new Chapter BC-4 Customer Complaints Procedures. BC-4.2 and BC-4.3 01/2012 Minor corrections to correct typos and clarify language. BC-4.3.9 01/2012 Paragraph deleted as it repeats what is in Paragraph BC-4.3.7. BC-4.1.3A 10/2012 Added guidance on the appointment of the customer complaints officer. BC-4.7 07/2013 Additional details provided on reporting of complaints. BC-2.9 04/2016 Added requirements for insurance firms when dealing with medical insurance. BC-4.3.16 04/2020 Amended Paragraph adding reference to CBB consumer protection. BC-4.5.6 04/2020 Amended Paragraph adding reference to CBB consumer protection. BC-4.7.1 - BC-4.7.3 04/2020 Amended Paragraph adding reference to CBB consumer protection. BC-C 10/2020 Added a new Chapter on Provision of Financial Services on a Non-discriminatory Basis. BC-A.2.3 [Deleted]

Deleted: January 2007BC-A.2.4

Guidance on the implementation and transition to Volume 3 (Insurance) is given in Module ES (Executive Summary).

Amended: January 2007BC-B BC-B Scope of Application

BC-B.1 BC-B.1 Insurance Licensees

BC-B.1.1

Except as noted in this section, the requirements in this Module apply to all

insurance licensees , with respect to theirdirect insurance activities carried on from the Kingdom of Bahrain with a person who is a resident of Bahrain ('domestic business ').Amended: October 2011BC-B.1.2

The requirements of this Module therefore apply to

insurance firms andinsurance intermediaries who are selling, intermediating or advising ondirect insurance contracts from their offices in Bahrain, with respect tocustomers who are resident of Bahrain. The requirements in this Module do not, therefore, apply todirect insurance activities carried on from overseas branches and subsidiaries ofBahraini insurance licensees , or to activities carried on with non-residents.BC-B.1.3

Reinsurance business is exempted from the requirements of this Module because the reinsurance market is limited to dealings between insurance market professionals.

BC-B.1.4

The activities of

insurance managers and operators of insurance exchanges do not fall within the scope of this Module. However, the CBB expects theinsurance manager to consider the requirements of this Module in relation to the service provided, on behalf of thecaptive insurer orinsurance firm , to its 'clients', namely insured members of the group.Amended: January 2007BC-B.1.5

Although the requirements of this Module apply in full to all

direct insurance activities in relation todomestic business , the CBB recognises that customers' needs vary. For example, because acaptive insurer is insuring the risks of its parent group, it would be acceptable for the level of sales documentation and written disclosure to be less than would be required for retailcustomers . Large corporatecustomers may also require less extensive written disclosures than retailcustomers . The requirements in this Module giveinsurance licensees the flexibility to adapt their processes to suit the different needs of differentcustomer types.Amended: January 2007BC-C BC-C Provision of Financial Services on a Non-discriminatory Basis

BC-C.1 BC-C.1 Provision of Financial Services on a Non-discriminatory Basis

BC-C.1.1

Insurance licensees must ensure that all regulated financial services are provided without any discrimination based on gender, nationality, origin, language, faith, religion, physical ability or social standing.Added: October 2020BC-1 BC-1 General Requirements

BC-1.1 BC-1.1 General Rules

BC-1.1.1

This Module applies to the

direct insurance activities of all licensees in relation todomestic business .BC-1.1.2

This Module aims to encourage high standards of business conduct, which are broadly applicable to all licensees, all types of

direct insurance business (i.e. excluding reinsurance), and all types ofcustomers . However, it is recognized that some types of licensees or business (such as captive insurance or commercial insurance) may present lower regulatory risks in relation to business conduct. For these types of business, the CBB therefore accepts that less detailed arrangements are likely to be sufficient to implement the principles contained in this Module. The CBB will monitor the regulatory performance of the market, and may in due course allow for specific exemptions or relaxations for certain types of business or licensees (see also BC-1.1.11 and BC-1.1.12).Amended: January 2007BC-1.1.3

Where packaged investment products include insurance elements, this Module applies to the insurance elements.

BC-1.1.4

It is recognised that investment products represent different features and risks that require separate regulatory treatment. Specific rules applying to business conduct in relation to investment products will be developed over time.

Amended: January 2007BC-1.1.5

All licensees must comply with the Insurance Code of Practice for business conduct with

customers , which sets out the minimum standards of good practice for market conduct in relation todirect insurance activities.BC-1.1.6

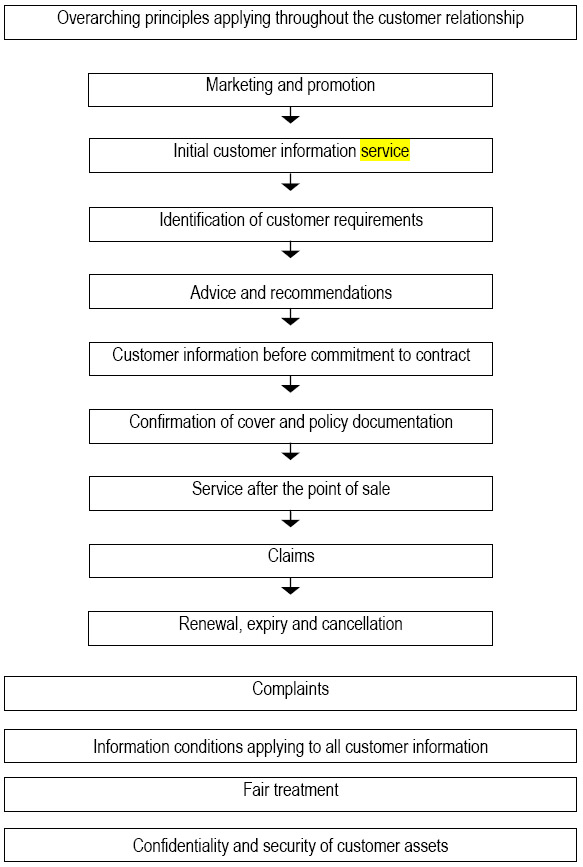

The Code comprises a number of overarching principles and a number of principles-based requirements rules in relation to the conduct of

direct insurance business withcustomers . The structure of the Insurance Code of Practice for Business Conduct withcustomers reflects the key stages and activities over the lifetime of thecustomer relationship for insurance products and services (see Illustration 1).Illustration 1: Structure of Insurance Code of Practice for Business Conduct

Amended: January 2007

Amended: January 2007BC-1.1.7

Licensees must maintain compliance with the Code throughout the lifetime of their relationships with all of their

customers .BC-1.1.8

The Code focuses on desired outcomes, rather than prescribing in detail measures required to achieve those outcomes. Licensees therefore have the flexibility to design arrangements that implement the Code, in a way that suits the particular nature of their business.

BC-1.1.9

Insurance licensees must take responsibility for compliance with the Code of all persons carrying outdirect insurance activities on their behalf (including, but not limited to,appointed representatives andinsurance managers ).Amended: October 2007BC-1.1.10

Licensees must put in place appropriate measures across all their business operations and distribution channels to ensure compliance with the Code. Licensees must maintain adequate records to demonstrate compliance with the Code.

BC-1.1.11

The CBB will monitor compliance with the Code and standards of business conduct. If required, the CBB may develop more detailed rules and guidance to supplement the existing Code.

Amended: January 2007BC-1.1.12

The CBB will apply these requirements in a way that allows them to be adapted to fit the circumstances of licensees' businesses, to be achieved through a pragmatic approach to supervision. However, in exceptional circumstances, it may be appropriate for the CBB to consider and grant waivers where strict compliance would be unduly burdensome or would not achieve the purpose for which the requirement was intended. Each application for waiver will be considered on its individual merits. The fact that a waiver has been granted to a particular licensee should not be regarded as an indication that similar waivers will be issued to any other licensee.

Amended: January 2007BC-2 BC-2 The Insurance Code of Practice

BC-2.1 BC-2.1 Overarching Principles

BC-2.1.1

In the course of

direct insurance activities, licensees must:(a) Act with due skill, care and diligence in all dealings withcustomers ;(b) Act fairly and reasonably in all dealings withcustomers ;(c) Identifycustomers' specific requirements in relation to the products and services about which they are enquiring;(d) Ensure that any advice tocustomers is aimed at thecustomers' interests and based on adequate standards of research and analysis;(e) Provide sufficient information to enablecustomers to make informed decisions when purchasing insurance products and services offered to them;(f) Provide sufficient and timely documentation tocustomers to confirm that their insurance arrangements are in place and provide all necessary information about their products, rights and responsibilities;(g) Maintain fair treatment ofcustomers through the lifetime of their insurance products andcustomer relationships, and ensure thatcustomers are kept informed of important events;(h) Handle claims fairly and promptly;(i) Ensure that all information provided tocustomers is clear, fair and not misleading, and appropriate tocustomers' information needs; and(j) Take appropriate measures to safeguard any money and property handled on behalf ofcustomers and maintain confidentiality ofcustomer information.Amended: January 2007

Amended: October 2007BC-2.2 BC-2.2 Marketing and Promotion

BC-2.2.1

Licensees must ensure that all advertising and promotional material is clear, fair and not misleading.

BC-2.3 BC-2.3 Initial Customer Information about Service

BC-2.3.1

At the initial point of contact, before any contract is concluded between the

customer and theinsurance licensee , licensees must advisecustomers of the nature of the service they can offer and their relationship with thecustomer , including:(a) The types of services that can be provided;(b) The choice of products and services that can be offered; and(c) Whether the licensee acts on behalf of an insurer or insurers, or acts independently on behalf of thecustomer in arranging insurance.Amended: January 2007BC-2.4 BC-2.4 Identification of Customer Requirements

BC-2.4.1

Licensees must identify

customers' requirements by seeking fromcustomers such information about their circumstances and objectives as might reasonably be expected to be relevant in establishing their specific insurance needs in relation to the products and services about which they are enquiring.BC-2.5 BC-2.5 Advice and Recommendations

BC-2.5.1

Any recommendations made must be appropriate to the

customer's needs. The recommendation must include an explanation as to how the recommended product suits thecustomer's identified needs. Where more than one product is recommended as appropriate to thecustomer's needs, the recommendation must include an explanation of the differences in and relative costs in the alternative options.Amended: January 2007BC-2.5.2

In the case of compulsory insurance, such as third party motor liability insurance, the explanation of the product's suitability may be limited to a brief explanation of the obligation to hold such insurance, and the options available to satisfy the obligation.

BC-2.5.3

The objective of Paragraph BC-2.5.1 is to ensure that a

customer is provided with sufficient information with which to make an informed decision. Aninsurance firm is able to rely on thecustomer's explanation of his insurance needs and is not otherwise required to verify thecustomer's own assessment of his needs. Given thecustomer's stated needs, theinsurance firm must explain how the proposed contract(s) would meet those needs, and provide sufficient information regarding the different options so that thecustomer is able to make an informed decision.Amended: January 2007BC-2.6 BC-2.6 Customer Information before Commitment to the Contract

BC-2.6.1

Before

customers make their final commitment to enter into acontract of insurance , licensees must provide to thecustomer sufficient information on the key features of the product being proposed to enable thecustomer to make an informed purchasing decision, including:(a) The identity of theinsurance licensee ;(b) All the important details of cover and benefits;(c) Any significant or unusual restrictions or exclusions, conditions or obligations attaching to thecustomer ; and(d) The period of cover.Amended: January 2007

Amended: October 2007BC-2.6.2

Before

customers make their final commitment to enter into acontract of insurance , licensees must provide to thecustomer full details of costs of the insurance products and services being offered, including:(a) The level of insurance premiums, the periodicity of payment and any grace periods allowed for payment;(b) The consequences of discontinuing the payment of any premium; and(c) Any fees and charges other than the insurance premium.Amended: January 2007

Amended: October 2007BC-2.6.3

While an

insurance broker may not approach every possible underwriter for each risk, he should make reasonable efforts to make his selection from a panel ofinsurance firms . Aninsurance broker's submission of quotations should incorporate the reasons for recommending or choosing aninsurance firm .BC-2.6.4

Except for

clients with turnover exceeding BD 1 million per year, aninsurance intermediary must draw theclient's attention to the status of theinsurance firm : i.e. whether or not theinsurance firm is locally licensed (as aBahraini insurance firm oroverseas insurance firm ) and, if not, the reasons for recommending or choosing thatinsurance firm . In respect of theseclients , this advice must be delivered in writing.Amended: January 2007BC-2.6.5

An

insurance intermediary should recommend, in the first instance, a policy from a CBB licensed insurer (which, for the avoidance of doubt, may be anoverseas insurance firm ) that he considers best suited to the needs of hisclient , and offering ease of client service, claims handling, etc. Paragraph BC-2.6.4 covers the situation where aninsurance intermediary proposes use of an overseas insurer not licensed or incorporated in Bahrain, because of the lack of availability of local cover.Amended: January 2007BC-2.6.6

Insurance intermediaries acting on behalf ofcustomers in arranging their insurance must, on request, disclose the amount of commission payable to them from the insurance premium, and any other remuneration received for arranging the insurance contract.BC-2.6.7

Before

customers make a final commitment to enter into acontract of insurance , licensees must inform thecustomer of their key obligations and rights with regard to the transaction, including:(a) Thecustomer's duty of disclosure to theinsurance licensee ;(b) Cancellation rights and conditions;(c) The licensee's internal complaints procedure; and(d) The licensee's obligations in respect of this Code.Amended: January 2007

Amended: October 2007BC-2.6.8

There are no specific requirements prescribing

customers' cancellation rights or required standards of cancellation terms for insurance products andcustomers . It is expected that licensees will put in place cancellation terms that are fair, reasonable and appropriate with respect to theircustomers and the products provided, in line with the overarching principles requiring fair dealings withcustomers (see Paragraph BC-2.1.1). The CBB will monitor the regulatory performance of the market in this area, and may make amendments over time (see Paragraphs BC-1.1.11, BC-1.1.12).Amended: January 2007BC-2.7 BC-2.7 Confirmation of Cover and Policy Documentation

BC-2.7.1

On the conclusion of contracts, licensees must provide

customers with prompt written confirmation and details of the insurance that has been effected, including:(a) The date when cover starts and the period of cover;(b) Any certificates or documents which thecustomer is required to have by law;(c) Details of how thecustomer can make a claim, and their responsibilities in relation to making claims;(d) The address of the insurer to which all communications in respect of the policy should be sent; and(e) Proof of payment where applicable.Amended: January 2007BC-2.7.2

Licensees must provide full policy documentation promptly following the conclusion of contracts, unless this has already been issued with the confirmation of cover.

BC-2.8 BC-2.8 Service after the Point of Sale

BC-2.8.1

Licensees must respond to and administer

customers' requests for amendments to their insurance policies in a timely manner. In particular, licensees must:(a) Provide written confirmation of any changes/amendments to the policy;(b) Provide full details of any additional premium or charges to be paid by or returned to thecustomer ;(c) Provide any certificate or documentation which thecustomer is required to have by law;(d) Provide proof of payment of additional premium or charges where applicable; and(e) Remit any refunds of premiums or charges due tocustomers without undue delay.Amended: January 2007BC-2.9 BC-2.9 Claims

BC-2.9.1

In addition to the requirements under Paragraph BC-2.9.2, where licensees' insurance activities include the handling of claims, they must:

(a) Respond promptly when claims are first notified, and providecustomers with an explanation about how the claim will be handled and any actions required of thecustomer ;(b) Provide reasonable guidance tocustomers in pursuing their claim;(c) Consider and handle claims fairly and promptly, and keep thecustomer informed of progress;(d) Informcustomers in writing, with an explanation, if thelicensee is unable to deal with all or any part of the claim; and(e) Forward settlement of claims without undue delay, once settlement has been agreed.Amended: April 2016

Amended: October 2007

January 2007BC-2.9.2

Where an

insurance firm deals with medical insurance and handles all the claim processing activities directly, i.e. without using a TPA:(a) It must process and settle all medical claims with policyholders within 15 calendar days from the receipt of all necessary documents; and(b) It must process and settle claims from healthcare service providers within 30 calendar days from the receipt of all necessary documents from the healthcare service providers.April 2016BC-2.9.3

Insurance firms must comply with Paragraph BC-2.9.2 by 30th September 2016 at the latest.April 2016BC-2.10 BC-2.10 Renewal, Expiry and Cancellation

BC-2.10.1

Licensees must notify

customers of the renewal or expiry of their policy in time to allow thecustomer to consider and rearrange any continuing cover they may need, including:(a) Details of the renewal terms, if offered; and(b) Details of any changes to the cover, service orinsurance firm being offered.Amended: January 2007BC-2.10.2

On expiry or cancellation of insurance policies, at the request of the

customer , licensees must make available all documentation and information to which thecustomer is entitled in a timely manner.BC-2.11 BC-2.11 [This section was deleted in October 2011]

BC-2.11.1

[This paragraph was deleted in October 2011]

Deleted: October 2011BC-2.11.2

[This paragraph was deleted in October 2011]

Deleted: October 2011

Amended: January 2007BC-2.11.3

[This paragraph was deleted in October 2011]

Deleted: October 2011

Amended: January 2007BC-2.11.4

[This paragraph was deleted in October 2011]

Deleted: October 2011

Amended: January 2007BC-2.11.5

[This paragraph was deleted in October 2011]

Deleted: October 2011

Amended: October 2007

Amended: January 2007

BC-2.12 BC-2.12 Information Conditions

BC-2.12.1

Licensees must ensure that all information presented to

customers in accordance with this Code shall be clear, fair and not misleading, and comprehensible to thecustomer having regard to the complexity of the products and services being offered and thecustomer's knowledge.BC-2.12.2

Licensees must ensure that

customer information presented tocustomers in accordance with this Code is provided in an appropriate format with regard to the complexity of the product being discussed. In particular:(a) As a general rule, all information to be provided to thecustomer in accordance with this Code is to be in writing, on paper or other durable medium available and accessible to thecustomer . If the information is initially presented orally, supporting written information must be provided in addition;(b) In the case of telephone selling and other forms of selling where it is impractical to provide information to thecustomer in writing at the point of sale, information shall be provided to thecustomer in accordance with Subparagraph BC-2.12.2(a) immediately following conclusion of the contract; and(c) By way of derogation from Subparagraph BC-2.12.2(a), information may be provided orally without supporting written information where thecustomer requests it, or where immediate cover is necessary.Amended: January 2007BC-2.13 BC-2.13 Fair Treatment and Conflicts of Interest

BC-2.13.1

Licensees must avoid conflicts of interest, or if conflicts are unavoidable, must explain the position fully and manage the situation so as to avoid prejudice to any party. In particular, licensees who act on behalf of their

customers must not put their own interests above their duty to anycustomers for whom they act.BC-2.13.2

Insurance intermediaries must disclose in writing to theclient any relationship that he may have with aninsurance firm that he is recommending to hisclient and which may result in a potential conflict of interest including, but not limited to, disclosure in writing any association arising from commonshareholder /controller /Director .Amended: January 2007BC-2.14 BC-2.14 Confidentiality and Security of Customer Assets

BC-2.14.1

Licensees must ensure that any information obtained from

customers must not be used or disclosed except in the normal course of negotiating, maintaining or renewing insurance for thatcustomer , unless:(a) They have thecustomer's consent;(b) Disclosure is made in accordance with the licensee's regulatory obligations; or(c) The licensee is legally obliged to disclose the information.Amended: January 2007BC-2.14.2

Licensees must take appropriate steps to ensure the security of any money, documents, other property or information handled or held on behalf of

customers .BC-3 BC-3 Takaful Firms

BC-3.1 BC-3.1 General Requirements

BC-3.1.1

This Chapter applies only to those

insurance firms licensed to conduct insurance business under takaful principles.Amended: January 2007BC-3.1.2

The CBB acknowledges that the nature of takaful and the operation of a takaful business are not entirely equivalent to and in some respects different from a conventional insurance business. The specific requirements set out in this Chapter aim not only to allow

takaful firms to operate in Bahrain within the CBB's insurance regulatory regime on a basis consistent with conventional insurers but also to recognise some of the differences in takaful that are relevant to the way in which takaful business is carried on.Amended: January 2007

Amended: October 2007BC-3.2 BC-3.2 Restriction on the Use of Terms

BC-3.2.1

The use of the terms '

takaful ', 'retakaful ', 'general takaful' and 'family takaful ' may only be used to describe the products ofinsurance firms that are Islamic financial institutions within the meaning of the CBB Rulebook.Amended: January 2007

Amended: October 2007BC-3.2.2

For the purposes of this Module, references to

takaful shall be taken as including 'takaful ', 'retakaful ', 'general takaful' and 'family takaful '.Amended: January 2007

Amended: October 2007BC-3.2.3

The use of the term 'Islamic insurance' should be avoided and may never be used by a firm not licensed to conduct the regulated activity of

takaful .Amended: January 2007

Amended: October 2007BC-3.3 BC-3.3 Marketing and Promotion

BC-3.3.1

An

insurance firm may only offertakaful products if it is licensed to do so. Aninsurance intermediary may offer both conventional insurance andtakaful products but must provide clear information to enable consumers to make informed choices.Amended: October 2007BC-3.3.2

Any comparison between

takaful and conventional insurance products must draw thecustomer's attention to the principal differences between these products. These differences may include:(a) Whether there is a contractual right to claims or benefits or whether these are discretionary on the part of the firm;(b) The basis on which benefits and surpluses are allocated to, and between,policyholders and participants; and(c) Whether there is any future liability ofpolicyholders (or participants), individually or collectively, for deficits in thepolicyholders' (participants') funds.Amended: January 2007

Amended: October 2007BC-3.4 BC-3.4 Disclosure

BC-3.4.1

Takaful firms must provide participants andshareholders with clear information about the performance of their business. This information must, as a minimum, comply with relevant AAOIFI standards, in particular Standard 13 (Disclosure of Bases for Determining and Allocating Surplus or Deficit in Islamic Insurance Companies) and 12 (General Presentation and Disclosure in the Financial Statements of Islamic Insurance Companies).Amended: January 2007BC-3.4.2

Takaful firms must clearly disclose to participants the calculation (percentage) and amount of wakala fee and mudaraba share of profits paid by the takaful fund to the takaful operator.Amended: January 2007BC-4 BC-4 Customer Complaints Procedures

BC-4.1 BC-4.1 General Requirements

BC-4.1.1

All

insurance licensees must have appropriate customer complaints handling procedures and systems for effective handling of complaints made by customers by 31st March 2012.Added: October 2011BC-4.1.2

Customer complaints procedures must be documented appropriately and their customers must be informed of their availability.

Added: October 2011BC-4.1.3

All

insurance licensees must appoint a customer complaints officer and publicise his/ her contact details at all departments and branches. The customer complaints officer must be of a senior level at theinsurance licensee and must be independent of the parties to the complaint to minimize any potential conflict of interest.Added: October 2011BC-4.1.3A

The position of customer complaints officer may be combined with that of compliance officer.

Added: October 2012BC-4.1.4

In the case of an

overseas insurance licensee , a local complaints officer must be present and must report all complaints to the head office complaints unit.Added: October 2011BC-4.2 BC-4.2 Documenting Customer Complaints Handling Procedures

BC-4.2.1

In order to make customer complaints handling procedures as transparent and accessible as possible, all

insurance licensees must document their customer complaints handling procedures. These include setting out in writing:(a) The procedures and policies for:(i) Receiving and acknowledging complaints;(ii) Investigating complaints;(iii) Responding to complaints within appropriate time limits;(iv) Recording information about complaints; and(v) Identifying recurring system failure issues; and(b) The types of remedies available for resolving complaints; and(c) The organisational reporting structure for the complaints handling function.Amended: January 2012

Added: October 2011BC-4.2.2

Insurance licensees must provide a copy of the procedures to all relevant staff, so that they may be able to inform customers. A simple and easy-to-use guide to the procedures must also be made available to all customers, on request, and when they want to make a complaint.Added: October 2011BC-4.2.3

Insurance licensees are required to ensure that claims forms and claim notification documents include a statement informing the customer of the availability of a simple and easy-to-use guide on customer complaints procedures in the event the customer is not satisfied with the services provided.Amended: January 2012

Added: October 2011BC-4.3 BC-4.3 Principles for Effective Handling of Complaints

BC-4.3.1

Adherence to the following principles is required for effective handling of complaints:

Added: October 2011Visibility

BC-4.3.2

"How and where to complain" must be well publicised to customers and other interested parties, in both English and Arabic languages.

Added: October 2011Accessibility

BC-4.3.3

A complaints handling process must be easily accessible to all customers and must be free of charge.

Added: October 2011BC-4.3.4

While an

insurance licensee's website is considered an acceptable mean for dealing with customer complaints, it should not be the only means available to customers as not all customers have access to the internet.Amended: January 2012

Added: October 2011BC-4.3.5

Process information must be readily accessible and must include flexibility in the method of making complaints.

Added: October 2011BC-4.3.6

Support for customers in interpreting the complaints procedures must be provided, upon request.

Added: October 2011BC-4.3.7

Information and assistance must be available on details of making and resolving a complaint.

Added: October 2011BC-4.3.8

Supporting information must be easy to understand and use.

Added: October 2011BC-4.3.9

[This Paragraph was deleted in January 2012].

Deleted: January 2012BC-4.3.10

Insurance licensees should incorporate the complaints procedure as a clause within the insurance policies provided to their customers.Added: October 2011Responsiveness

BC-4.3.11

Receipt of complaints must be acknowledged in accordance with Section BC-4.5 "Response to Complaints".

Added: October 2011BC-4.3.12

Complaints must be addressed promptly in accordance with their urgency.

Added: October 2011BC-4.3.13

Customers must be treated with courtesy.

Added: October 2011BC-4.3.14

Customers must be kept informed of the progress of their complaint.

Added: October 2011BC-4.3.15

If a customer is not satisfied with an

insurance licensee's response, theinsurance licensee must advise the customer on how to take the complaint further within the organisation.Added: October 2011BC-4.3.16

In the event that they are unable to resolve a complaint,

insurance licensees must outline the options that are open to that customer to pursue the matter further, including, where appropriate, referring the matter to the Consumer Protection Unit at the CBB.Amended: April 2020

Added: October 2011Objectivity and Efficiency

BC-4.3.17

Complaints must be addressed in an equitable, objective, unbiased and efficient manner.

Amended: January 2012

Added: October 2011BC-4.3.18

General principles for objectivity in the complaints handling process include:

(a) Openness:

The process must be clear and well publicised so that both staff and customers can understand.(b) Impartiality:(i) Measures must be taken to protect the person the complaint is made against from bias;(ii) Emphasis must be placed on resolution of the complaint not blame; and(iii) The investigation must be carried out by a person independent of the person complained about.(c) Accessibility:(i) Theinsurance licensee must allow customer access to the process at any reasonable point in time; and(ii) A joint response must be made when the complaint affects different participants.(d) Completeness:

The complaints officer must find the relevant facts, talk to both sides, establish common ground and verify explanations wherever possible;(e) Equitability:

Give equal treatment to all parties.(f) Sensitivity:

Each complaint must be treated on its merits and paying due care to individual circumstances.(g) Objectivity for personnel — complaints handling procedures must ensure those complained about are treated fairly which implies:(i) Informing them immediately and completely on complaints about performance;(ii) Giving them an opportunity to explain and providing appropriate support;(iii) Keeping them informed of the progress and result of the complaint investigation;(iv) Full details of the complaint are given to those the complaint is made against prior to interview; and(v) Personnel must be assured they are supported by the process and should be encouraged to learn from the experience and develop a better understanding of the complaints process;(h) Confidentiality:(i) In addition to customer confidentiality, the process must ensure confidentiality for staff who have a complaint made against them and the details must only be known to those directly concerned;(ii) Customer information must be protected and not disclosed, unless the customer consents otherwise; and(iii) Protect the customer and customer's identity as far as is reasonable to avoid deterring complaints due to fear of inconvenience or discrimination.(i) Objectivity monitoring:

insurance licensees must monitor responses to customers to ensure objectivity which could include random monitoring of resolved complaints.(j) Charges:

The process must be free of charge to customers;(k) Customer Focused Approach:(i)Insurance licensees must have a customer focused approach;(ii)Insurance licensees must be open to feedback; and(iii)Insurance licensees must show commitment to resolving problems.(l) Accountability:

Insurance licensees must ensure accountability for reporting actions and decisions with respect to complaints handling; and(m) Continual improvement:

Continual improvement of the complaints handling process and the quality of products and services must be a permanent objective of theinsurance licensees .Amended: January 2012

Added: October 2011BC-4.4 BC-4.4 Internal Complaint Handling Procedures

BC-4.4.1

An

insurance licensee's internal complaint handling procedures must provide for:(a) The receipt of written complaints;(b) The appropriate investigation of complaints;(c) An appropriate decision-making process in relation to the response to a customer complaint;(d) Notification of the decision to the customer;(e) The recording of complaints; and(f) How to deal with complaints when a business continuity plan (BCP) is operative.Added: October 2011BC-4.4.2

An

insurance licensee's internal complaint handling procedures must be designed to ensure that:(a) All complaints are handled fairly, effectively and promptly;(b) Recurring systems failures are identified, investigated and remedied;(c) The number of unresolved complaints referred to the CBB is minimized;(d) The employee responsible for the resolution of complaints has the necessary authority to resolve complaints or has ready access to an employee who has the necessary authority; and(e) Relevant employees are aware of theinsurance licensee's internal complaint handling procedures and comply with them and receive training periodically to be kept abreast of changes in procedures.Added: October 2011BC-4.5 BC-4.5 Response to Complaints

BC-4.5.1

An

insurance licensee must acknowledge in writing within the same day of receipt of customer written complaints for non-life insurance policies and within 5 business days of receipt of customer written complaints for life insurance policies.Added: October 2011BC-4.5.2

An

insurance licensee must respond in writing to a customer's complaint within one week of receiving non-life insurance policies complaint and within 2 weeks of receiving life insurance policies complaint, explaining their position and how they propose to deal with the complaint.Added: October 2011Redress

BC-4.5.3

An

insurance licensee should decide and communicate how it proposes (if at all) to provide the customer with redress. Where appropriate, theinsurance licensee must explain the options open to the customer and the procedures necessary to obtain the redress.Added: October 2011BC-4.5.4

Where an

insurance licensee decides that redress in the form of compensation is appropriate, theinsurance licensee must provide the complainant with fair compensation and must comply with any offer of compensation made by it which the complainant accepts.Added: October 2011BC-4.5.5

Where an

insurance licensee decides that redress in a form other than compensation is appropriate, it must provide the redress as soon as practicable.Added: October 2011BC-4.5.6

Should the customer that filed a complaint not be satisfied with the response received as per Paragraph BC-4.5.2, he can forward the complaint to the Consumer Protection Unit at the CBB within 30 calendar days from the date of receiving the letter from the

insurance licensee .Amended: April 2020

Added: October 2011BC-4.6 BC-4.6 Records of Complaints

BC-4.6.1

An

insurance licensee must maintain a record of all customers' complaints. The record of each complaint must include:(a) The identity of the complainant;(b) The substance of the complaint;(c) The status of the complaint, including whether resolved or not, and whether redress was provided; and(d) All correspondence in relation to the complaint. Such records must be retained by theinsurance licensee for a period of 5 years from the date of receipt of the complaint.Added: October 2011BC-4.7 BC-4.7 Reporting of Complaints

BC-4.7.1

An

insurance licensee must submit to the CBB's Consumer Protection Unit a quarterly report summarising the following:(a) The number of complaints received;(b) The substance of the complaints;(c) The number of days it took theinsurance licensee to acknowledge and to respond to the complaints; and(d) The status of the complaint, including whether resolved or not, and whether redress was provided.Amended: April 2020

Added: October 2011BC-4.7.2

The report referred to in Paragraph BC-4.7.1 must be sent electronically to Complaint@cbb.gov.bh.

Amended: April 2020

Added: July 2013BC-4.7.3

Where no complaints have been received by the licensee within the quarter, a 'nil' report should be submitted to the CBB’s Consumer Protection Unit.

Amended: April 2020

Added: July 2013BC-4.8 BC-4.8 Monitoring and Enforcement

BC-4.8.1

Compliance with these requirements is subject to the ongoing supervision of the CBB as well as being part of any CBB inspection of a

licensee . Failure to comply with these requirements is subject to enforcement measures as outlined in Module EN (Enforcement).Added: October 2011