PART 1: PART 1: Definition of Capital

CA-A CA-A Introduction

CA-A.1 CA-A.1 Application

CA-A.1.1

Rules in this Module are applicable to locally incorporated banks on both a stand-alone basis (i.e. including their foreign

branches ), and on a consolidated group basis (i.e. including their subsidiaries and any other investments which are included or consolidated into the group accounts or are required to be consolidated for regulatory purposes by the Central Bank of Bahrain ('CBB')).Amended: January 2011

Apr 08CA-A.1.2

In addition to licensees mentioned in Paragraph CA-A.1.1, certain of these Rules (in particular gearing and market risk requirements) are also applicable to Bahrain

branches of foreign retail bank licensees.Amended: January 2011

Apr 08CA-A.1.3

Rules in this Module are applicable to locally incorporated Islamic banks (hereinafter referred to as "the banks") on both a stand-alone and consolidated group basis.

Amended: January 2011

Apr 08CA-A.1.4

If the banks have investments in other entities, the banks must also apply the Rules set out in the Prudential Consolidation and Deduction Requirements Module (Module PCD) for the calculation of their solo and consolidated Capital Adequacy Ratio (CAR).

Amended: January 2011

Apr 08CA-A.2 CA-A.2 Purpose

Executive Summary

CA-A.2.1

The purpose of this Module is to set out the CBB's

capital adequacy Rules and provide guidance on the risk measurement for the calculation of capital requirements by banks referred to under Paragraph CA-A.1.1. This requirement is supported by Article 44(c) of the Central Bank of Bahrain and Financial Institutions Law (Decree No. 64 of 2006).Amended: January 2011

Apr 08CA-A.2.2

The Module also sets out the minimum gearing requirements which relevant banks (referred to in Section CA-A.1) must meet as a condition of their licensing.

Apr 08CA-A.2.3

Principle 9 of the Principles of Business requires that

Islamic bank licensees maintain adequate human, financial and other resources, sufficient to run their business in an orderly manner (see Section PB-1.1.9). In addition, Condition 5 of CBB's Licensing Conditions (Section LR-2.5) requiresIslamic bank licensees to maintain financial resources in excess of the minimum requirements specified in Module CA (Capital Adequacy).Apr 08CA-A.2.4

The requirements specified in this Module vary according to the Category of

Islamic bank licensee concerned, their inherent risk profile, and the volume and type of business undertaken. The purpose of such requirements is to ensure thatIslamic bank licensees hold sufficient capital to provide some protection against unexpected losses, and otherwise allow conventional banks to effect an orderly wind-down of their operations, without loss to their depositors. The minimum capital requirements specified here may not be sufficient to absorb all unexpected losses.Apr 08Legal Basis

CA-A.2.5

This Module contains the CBB's Directive (as amended from time to time) relating to the capital adequacy of

Islamic bank licensees , and is issued under the powers available to the CBB under Article 38 of the CBB Law. The Directive in this Module is applicable to allIslamic bank licensees .Amended: January 2011

Apr 08CA-A.2.6

For an explanation of the CBB's rule-making powers and different regulatory instruments, see Section UG-1.1.

Apr 08CA-A.2.7

The CBB requires in particular that the banks maintain adequate capital, in accordance with the Rules in this Module, against their risks as capital provides banks with a cushion to absorb losses without endangering customer accounts. As such, the CBB also requires the relevant banks to maintain adequate liquidity and identify and control their large

exposures which might otherwise be a source of loss to a licensee on a scale that might threaten its solvency.Amended: January 2011

Apr 08CA-A.2.8

These Rules are consistent in all substantial respects with the approach recommended by the Basel Committee on Banking Supervision and Islamic Financial Services Board (IFSB) for capital adequacy.

Amended: January 2011

Apr 08CA-A.2.9

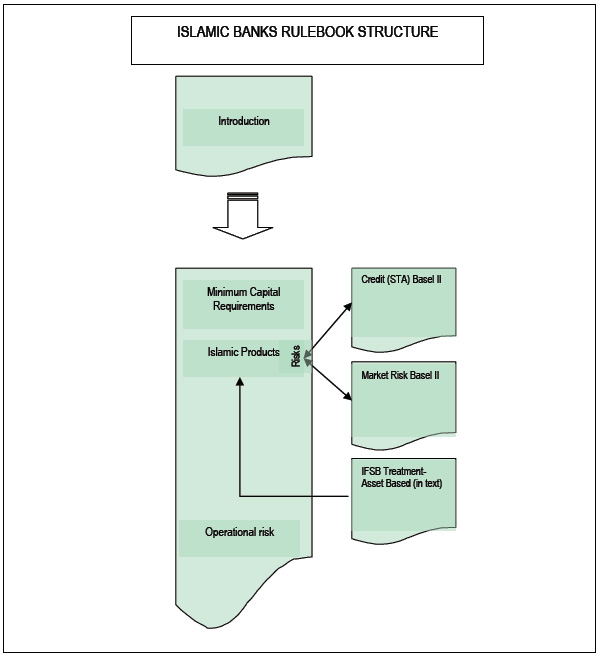

The CBB recognises that the Basel Committee guidelines may not address specific characteristics of the various products and services offered by Islamic banks. Therefore, the CBB has adopted a risk-based approach and has tailored the Rules to address the specific risk characteristics of Islamic banks. The structure of these Rules is explained on the next page.

Amended: January 2011

Apr 08CA-A.2.10

This Module provides support for certain other parts of the Rulebook, mainly:

(a) Prudential Consolidation and Deduction Requirements;(b) Licensing and Authorisation Requirements;(c) CBB Reporting Requirements;(d) Credit Risk Management;(e) Market Risk Management;(f) Operational Risk Management;(g) Liquidity Risk Management;(h) High Level Controls;(i) Relationship with Audit Firms; and(j) Penalties and Fines.

Amended: January 2011

Amended: January 2011

Apr 08CA-A.3 CA-A.3 Capital Adequacy Ratio

CA-A.3.1

Historically, on a consolidated basis, the CBB has set a minimum Capital Adequacy Ratio ("CAR") of 12.0% for all locally incorporated banks. Furthermore, on a solo basis, the parent bank has been required to maintain a minimum CAR of 8.0% (i.e. unconsolidated). The arrangements outlined below will apply once banks have been subject to a Pillar 2 risk profile assessment by the CBB or an acceptable audit firm. Until such an assessment has been completed, the existing 12% and 8% minimum capital ratio requirements (as outlined in Module CA-2.5 October 2006 edition) will remain in place.

Apr 08CA-A.3.2

CAR will be calculated by applying the regulatory capital to the numerator and risk-weighted assets (RWAs) to the denominator.

Eligible Capital

{ Total Risk-weighted Assets (Creditb + Marketb Risks) Plus Operational Risks

Less

Risk-weighted Assets funded by Restricted PSIAc (Creditb + Marketb Risks)

Less

(1 - α) [Risk-weighted Assets funded by Unrestricted PSIAc (Creditb + Marketb Risks)]

Less

α [Risk-weighted Assets funded by PER and IRR of Unrestricted PSIAe (Creditb +

Marketb Risks)]}(a) Total RWA include those financed by both restricted and unrestricted Profit Sharing Investment Accounts (PSIA);(b) Credit and market risks for on- and off-balance sheet exposures;(c) Where the funds are commingled, the RWA funded by PSIA are calculated based on their pro-rata share of the relevant assets. PSIA balances include PER and Investment risk reserve (IRR) or equivalent reserves;(d) — α refers to the proportion assets funded by unrestricted PSIA which, as determined by the CBB, is 30%; and(e) The relevant proportion of risk-weighted assets funded by the PSIA's share of PER and by IRR is deducted from the denominator. The PER has the effect of reducing the displaced commercial risk and the IRR has the effect of reducing any future losses on the investment financed by the PSIA.

The above formula is applicable as the Islamic banks may smooth income to the Investment Account Holders (IAHs) as part of a mechanism to minimise withdrawal risk and is concerned with systemic risk.Amended: April 2011

April 2008CA-A.3.3

All locally incorporated banks are required to maintain a capital ratio both on a solo (and a consolidated basis where applicable) above the minimum "trigger" CAR of 8%. Failure to remain above the trigger ratio will result in Enforcement and other measures as outlined in Section CA-1.4.

Apr 08CA-A.3.4

All locally incorporated banks will be required to maintain capital ratios above individually set "target" CARs on a solo and on a consolidated basis. These target CARs will be set at an initial minimum of 8.5% and may in the case of high risk banks be set at levels above the 12.5% target ratio set prior to January 2008. Failure to remain above the target ratio will result in Enforcement and other measures as outlined in Section CA-1.4.

Apr 08Eligible Capital

CA-A.3.5

Banks are allowed two classes of capital (see section CA-2.2) to meet their capital requirements for credit risk, operational risk and market risk, as set out below:

Tier 1: Core capital — Supports the calculation of credit risk weighted assets, operational risk and market risk.

Tier 2: Supplementary capital — Supports credit risk, operational risk and market risk subject to limitations.

Apr 08Risk-weighted Assets

CA-A.3.6

Total risk-weighted assets are determined by:

(i) Multiplying the capital requirements for market risk and operational risk by 12.5; and(ii) Adding the resulting figures to the sum of risk-weighted assets for credit risk.Amended: January 2011

Apr 08CA-A.3.7

Islamic banks are not contractually obliged to make good losses arising from Islamic financing assets funded by the investment accounts, unless these losses arise from the negligence on the part of the Islamic bank as manager (Mudarib) or as agent (Wakeel). However to be prudent, the CBB requires Islamic banks to provide regulatory capital to cover minimum requirement arising from 30% of the risk weighted assets and contingencies financed by the unrestricted investment accounts. Therefore, for the purpose of calculating its Capital Adequacy Ratio (CAR), the risk-weighted assets of an Islamic bank consist of the sum of the risk-weighted assets financed by the Islamic bank's own capital and liabilities, plus 30% of the risk-weighted assets financed by the Islamic bank's unrestricted PSIAs.

Amended: January 2011

Apr 08CA-A.3.8

In measuring credit risk for the purpose of

capital adequacy , banks must apply the standardised approach through which claims of different categories of counterparties are assigned risk weights (RWs) according to broad categories of relative riskiness.Apr 08CA-A.3.9

For the measurement of their operational risks, banks have a choice, subject to the written approval of the CBB, between two broad methodologies:

(a) One alternative is to measure the risks using a basic indicator approach, applying the measurement framework described in Chapter CA-6 of this Module; and(b) The second methodology (i.e. the standardised approach) is set out in detail in Chapter CA-6 including the procedure for obtaining the CBB's approval. This methodology is subject to the fulfillment of certain conditions. The use of this methodology is, therefore, conditional upon the explicit approval of the CBB.Amended: January 2011

Apr 08CA-A.3.10

In measuring market risk for the purpose of

capital adequacy , banks must apply the approach set out in relevant sections.Apr 08CA-A.3.11

If an Islamic bank wants to adopt an advanced approach (IRB for credit risk and/or IMA for market risk), it will need to apply to the CBB for prior approval.

Apr 08CA-A.4 CA-A.4 Module History

CA-A.4.1

This Module was first issued in January 2005 as part of the Islamic principles volume. Any material changes that have subsequently been made to this Module are annotated with the calendar quarter date in which the change was made. Chapter UG-3 provides further details on Rulebook maintenance and version control.

Apr 08CA-A.4.2

A list of most recent changes made to this Module are detailed in the table below:

Summary of ChangesModule Ref. Change Date Description of Changes CA-A.2 10/2007 New Rule CA-A.2.5 introduced, categorising this Module as a Directive. CA-1 to CA-6 01/2008 Basel II implementation. CA-1.5 01/2008 Review of PIR by external auditors CA-4.6 04/2008 Recognition of IIRA as ECAI and mapping of ratings CA-4.2.15–18 01/2009 New guidance and rules on SMEs CA-A 01/2011 Various minor amendments to ensure consistency in CBB Rulebook. CA-A.2.5 01/2011 Clarified legal basis. CA-5.1 & CA-5.3 01/2012 Changes in respect of July 2009 and February 2011 amendments to Basel II. CA-4.2.10 and CA-4.2.11A 04/2012 Amendment made for claims on banks dealing with self-liquidating letters of credit. CA-2.1.4(g) 10/2013 Added Rule to include limited general provision against unidentified future losses as part of Tier 2. CA-2.1.4(f), CA-2.1.4A to CA-2.1.4C and CA-2.2.1 10/2013 Added Rules to deal with subordinated issued for Tier 2 capital. CA-5.5.13 10/2013 Clarified Rules on structural positions for foreign exchange risk. Evolution of the Module

CA-A.4.3

Prior to the development of this Rulebook, the CBB issued various circulars representing regulations relating to

capital adequacy requirements. These circulars were consolidated into this Module and are listed below:Circular Ref. Date of Issue Module Ref. Circular Subject OG/78/01 20 Feb 2001 CA-A.3 and CA-1.4 Monitoring of Capital Adequacy BC/01/98 10 Jan 1998 CA-A.3 and CA-1.4 Capital Adequacy Ratio Apr 08Effective Date

CA-A.4.4

The contents retained from the previous module (Capital Adequacy-Islamic banks) are effective from the date depicted in the above circulars from which the requirements are compiled. The updated module is effective from January 01, 2008.

Apr 08CA-1 CA-1 Scope and Coverage of Capital Charges

CA-1.1 CA-1.1 Application

CA-1.1.1

All locally incorporated banks are required to measure and apply capital charges with respect to their credit, operational, market risk fiduciary and displacement risk, capital requirements.

Apr 08CA-1.1.2

Credit risk is defined as the potential that a bank's

counterparty will fail to meet its obligations in accordance with agreed terms. Credit risk exists throughout the activities of a bank in the banking book and in the trading book including both on-and off-balance-sheetexposures .Apr 08CA-1.1.3

Operational risk is defined as the risk of losses resulting from inadequate or failed internal processes, people and systems or from external events, which includes but is not limited to, legal risk and Sharia compliance risk. This definition excludes strategic and reputational risks.

Apr 08CA-1.1.4

Market risk is defined as the risk of losses in on- or off-balance-sheet positions arising from movements in market prices. The risks subject to the capital requirement of this module are:

(a) The risks pertaining to equities in the trading book;(b) Foreign exchange risk throughout the bank; and(c) Commodity risk throughout the bank.Amended: April 2011

April 2008CA-1.1.5

The CBB has adopted the IFSB definitions of fiduciary and displacement risk for the purpose of this volume.

Apr 08CA-1.1.6

Banks must compute capital charges for own funds as well as those of the unrestricted PSIAs. For the purpose of computing the Capital Adequacy Ratio, 30% of the bank's risk weighted assets relating to the unrestricted PSIAs must be included in accordance with the IFSB guidelines.

Apr 08CA-1.2 CA-1.2 Monitoring of Risks

CA-1.2.1

Banks are required to manage their risks, especially market risks, in such a way that the capital requirements are being met on a continuous basis i.e. at the close of each business day and not merely at the end of each calendar quarter. Banks are also required to maintain strict risk management systems to ensure that their intra-day

exposures are not excessive.Apr 08CA-1.2.2

Banks' daily compliance with the capital requirements for credit and market risks must be verified by an independent risk management department and internal audit. It is expected that external auditors will perform appropriate tests of the bank's daily compliance with the capital requirements for credit and market risks. Where a bank fails to meet the minimum capital requirements for credit and market risk on any business day, the CBB must be informed in writing by no later than the following business day. The CBB will then seek to ensure that the bank takes immediate measures to rectify the situation.

Apr 08CA-1.3 CA-1.3 Investments in other Entities and Consolidation

CA-1.3.1

The banks must also apply the rules set in the Prudential Consolidation and Deduction Requirements Module where the bank has investments in other entities.

Apr 08CA-1.3.2

These capital adequacy regulations must be applied on a worldwide consolidated basis as well as on a solo basis. Guidance on consolidation and related matters is provided in the Prudential Consolidation and Deduction Requirements Module.

Apr 08CA-1.4 CA-1.4 Reporting

CA-1.4.1

Formal reporting, to the CBB, of capital adequacy must be made in accordance with the requirements set out under section BR 3.1.

Apr 08CA-1.4.2

Where a bank's CAR falls below its individual target ratio either on a solo basis (or on a consolidated basis), the General Manager of the bank must notify the CBB by the following business day, however no formal action plan will be necessary. The General Manager must explain what measures are being implemented to ensure that the bank will remain above its minimum target CAR(s).

Apr 08CA-1.4.3

The bank will be required to submit form PIRI to the CBB on a monthly basis, until the concerned CAR exceeds its target ratio.

Apr 08CA-1.4.4

The CBB will notify banks in writing of any action required of them with regard to the corrective and preventive action (as appropriate) proposed by the bank pursuant to the above, as well as of any other requirement of the CBB in any particular case.

Apr 08CA-1.4.5

All locally incorporated banks must provide the CBB, with immediate written notification (i.e. by no later than the following business day) of any actual breach of the minimum trigger CAR of 8%. Where such notification is given, the bank must also provide the CBB:

(a) No later than one calendar week after the notification, with a written action plan setting out how the bank proposes to restore the relevant CAR(s) to the required minimum level(s) set out above and, further, describing how the bank will ensure that a breach of such CAR(s) will not occur again in the future; and(b) Report on a weekly basis thereafter on the bank's relevant CAR(s) until such CAR(s) have reached the required target level(s) described above.Amended: April 2011

April 2008CA-1.4.6

Banks must note that the CBB considers the breach of CARs to be a very serious matter. Consequently, the CBB may (at its discretion) subject a bank which breaches its CAR(s) to a formal licensing reappraisal. Such reappraisal may be effected either through the CBB's own inspection function or through the use of Reporting Accountants, as appropriate. Following such appraisal, the CBB will notify the bank concerned in writing of its conclusions with regard to the continued licensing of the bank.

Apr 08CA-1.4.7

The CBB recommends that the bank's compliance officer support and cooperate with the CBB in the monitoring and reporting of the CARs and other regulatory reporting matters. Compliance officers should ensure that their banks have adequate internal systems and controls to comply with these regulations.

Apr 08CA-1.5 CA-1.5 Review of Prudential Information Returns by External Auditors

CA-1.5.1

The CBB requires all relevant banks to request their external auditors to conduct a review of the prudential returns on a quarterly basis in accordance with the requirements set out under section BR . However, if a bank provides prudential returns without any reservation from auditors for two consecutive quarters, it can apply for exemption from such review for a period to be decided by CBB.

Apr 08CA-2 CA-2 Regulatory Capital

CA-2.1 CA-2.1 Regulatory Capital

CA-2.1.1

Islamic banks are allowed two types of own funds to meet their capital requirements for credit risk, market risk and operational risk as set out below:

Tier 1: Core capital — Supports the calculation of credit risk weighted assets, operational risk and market risk.

Tier 2: Supplementary capital — Supports credit risk, operational risk and market risk subject to limitations.

Apr 08CA-2.1.2

For the purpose of defining Tier capital, the CBB has broadly adopted the recommendations contained in IFSB's guidelines. However, some restrictions have been placed on the inclusion of profit equalisation and investment risk reserve as Tier 2 capital. For components of Tier 1 and Tier 2 capital refer to paragraphs CA-2.1.3 to CA-2.1.4.

Apr 08Tier 1: Core Capital

CA-2.1.3

Tier 1 capital shall consist of the sum of items (a) to (e) below, less the sum of items (f) through (j) below:

(a) Issued and fully paid ordinary shares;

For Islamic funds with participation and / or "B" class shares (not carrying voting rights), the treatment for the purpose of these regulations must be agreed with the CBB. The CBB will consider each case on its merit.(b) Disclosed reserves• General reserves• Legal / statutory reserves• Share premium• Capital redemption reserves• Excluding fair value reserves1(c) Retained profit brought forward;(d) Unrealized net gains arising from fair valuing equities2; and(e) Minority interests in subsidiaries Tier 1 equity, arising on consolidation, in the equity of subsidiaries that are less than wholly owned. Further guidance on minority interests is provided in the Prudential Consolidation and Deduction Requirements Module.LESS:

(f) Goodwill;(g) Current interim cumulative net losses;(h) Unrealized gross losses arising from fair valuing equity securities3;(i) Other deductions made on a pro-rata basis between Tier 1 and Tier 2;(j) Reciprocal cross holdings of other banks' capital.

1 This refers to unrealised fair value gains reported directly in equity (such gross gains are included in Tier 2).

2This refers to unrealised net fair value gains taken through P&L (which have been audited). Please note that the unrealised net gains related to unlisted equities taken through P&L arising on or after January 1, 2008 will be subject to 55% discount as stated in CA-2.1.4(c)ii.

3 This refers to both 'net losses taken through P&L' and 'gross losses reported directly in equity'.

Apr 08Tier 2: Supplementary Capital

CA-2.1.4

Tier 2 capital shall consist of the following items:

(a) Current interim retained profits that have been reviewed as per the ISA by the external auditors;(b)Asset revaluation reserves , which arise from the revaluation of fixed assets and real estate from time to time in line with the change in market values, and are reflected on the face of the balance sheet as a revaluation reserve. Similarly, gains may also arise from revaluation of Investment Properties (real estate). These reserves (including the net gains on investment properties) may be included in Tier 2 capital, with the concurrence of the external auditors, provided that the assets are prudently valued, fully reflecting the possibility of price and forced sale. A discount of 55% will be applied to the difference between the historical cost book value and the market value to reflect the potential volatility of this form of unrealised capital;(c) Unrealised gains arising from fair valuing equities:(i) For unrealized gross gains reported directly in equity, a discount factor of 55% will be applied before inclusion in Tier 2 capital. Note for gross losses, the whole amount of such unrealised loss should be deducted from the Tier 1 capital;(ii) For unrealized net gains reported in income, a discount factor of 55% will apply on any such unrealized net gains from unlisted equity instruments before inclusion in Tier 1 capital (for audited gains) or Tier 2 capital (for reviewed gains) as appropriate. This discount factor will be applied to the incremental net gains related to unlisted equities arising on or after January 1, 2008;(d) Banks should note that the Central bank will discuss the applicability of the discount factor under paragraph (c) above with individual banks. This discount factor relating to CA-2.1.4(c)ii may be reassessed by the CBB if the bank arranges an independent review (which has been performed for the bank's systems and controls relating to FV gains on financial instruments) and meets all the requirements of the paper 'Supervisory guidance on the use of the fair value option for financial instruments by banks' issued by Basel Committee on Banking Supervision in June 2006;(e) Profit equalisation reserve and investment risk reserve, up to a maximum amount equal to the capital charge pertaining to 30% of the risk weighted assets financed by unrestricted investment account holders;(f) Subordinated term capital instruments, which comprise all unsecured term instruments subordinated (with respect to both profit and principal) to all other liabilities of the bank except the share capital. To be eligible for inclusion in Tier 2 capital, subordinated term capital instruments should have a minimum original fixed term to maturity of over five years. During the last five years to maturity, a cumulative discount (or amortisation) factor of 20% per year will be applied to reflect the diminishing value of these instruments as a continuing source of strength. These instruments are not normally available to participate in the losses of a bank which continues trading. For this reason, these instruments will be limited to a maximum of 50% of Tier 1 capital. Subordinated term capital instruments must also satisfy the conditions outlined in the paragraphs below; and(g) Credit facilities loss provisions held against future, presently unidentified losses and are freely available to meet such losses which subsequently materialise. Such general provisions/general credit facilities-loss reserves eligible for inclusion in Tier 2 will be limited to a maximum of 1.25 percentage points of credit risk-weighted risk assets. Provisions ascribed to identified deterioration of particular assets or known liabilities, whether individual or grouped, must be excluded.Amended: October 2013

Amended: April 2011

April 2008CA-2.1.4A

Subordinated term capital instruments agreed to on a case by case basis by CBB, must meet the following conditions. They must be:

(a) Issued and fully paid;(b) Neither be secured nor covered by a guarantee of the issuer or related entity or other arrangement that legally or economically enhances the seniority of the claim vis-à-vis bank creditors;(c) The main features of such instruments must be easily understood and publicly disclosed;(d) Proceeds must be immediately available without limitation to the issuing bank; and(e) The bank must have discretion over the amount and timing of distributions, subject only to prior waiver of distributions on the bank's common stock, and banks must have full access to waived payments.Added: October 2013

CA-2.1.4B

A bank may not exercise a call on a subordinated term capital instrument, partially or in full, prior to the end of its term, unless it has received the CBB's prior written approval, and there is a clear statement in support of the call in the original documentation.

Added: October 2013

CA-2.1.4C

Where Paragraph CA-2.1.4B applies, the CBB will take into consideration whether the bank has received confirmation from its external auditor that the bank will continue to satisfy the CBB's capital adequacy requirements after such early call and the bank has sufficient liquidity to repay the subordinated term capital instrument. This can be done by assessing the impact of such redemption on the capital adequacy ratio of the bank.

Added: October 2013

CA-2.2 CA-2.2 Limits on the use of Different Forms of Capital

CA-2.2.1

Tier 1 capital should represent at least half of the total eligible capital, i.e., Tier 2 capital is limited to the 100% of Tier 1 capital. Subordinated term capital instruments are limited to a maximum of 50% of Tier 1 capital.

Amended: October 2013

Apr 08CA-2.2.2

The limit on Tier 2 capital is based on the amount of Tier 1 capital after all deductions of investments pursuant to Prudential Consolidation and Deduction Requirements Module (see Appendix PCD-2 of PCD module for an example of the deduction effects and the caps).

Apr 08