Legal Basis

CA-A.2.5

This Module contains the CBB's Directive (as amended from time to time) relating to the capital adequacy of

Islamic bank licensees , and is issued under the powers available to the CBB under Article 38 of the CBB Law. The Directive in this Module is applicable to allIslamic bank licensees .Amended: January 2011

Apr 08CA-A.2.6

For an explanation of the CBB's rule-making powers and different regulatory instruments, see Section UG-1.1.

Apr 08CA-A.2.7

The CBB requires in particular that the banks maintain adequate capital, in accordance with the Rules in this Module, against their risks as capital provides banks with a cushion to absorb losses without endangering customer accounts. As such, the CBB also requires the relevant banks to maintain adequate liquidity and identify and control their large

exposures which might otherwise be a source of loss to a licensee on a scale that might threaten its solvency.Amended: January 2011

Apr 08CA-A.2.8

These Rules are consistent in all substantial respects with the approach recommended by the Basel Committee on Banking Supervision and Islamic Financial Services Board (IFSB) for capital adequacy.

Amended: January 2011

Apr 08CA-A.2.9

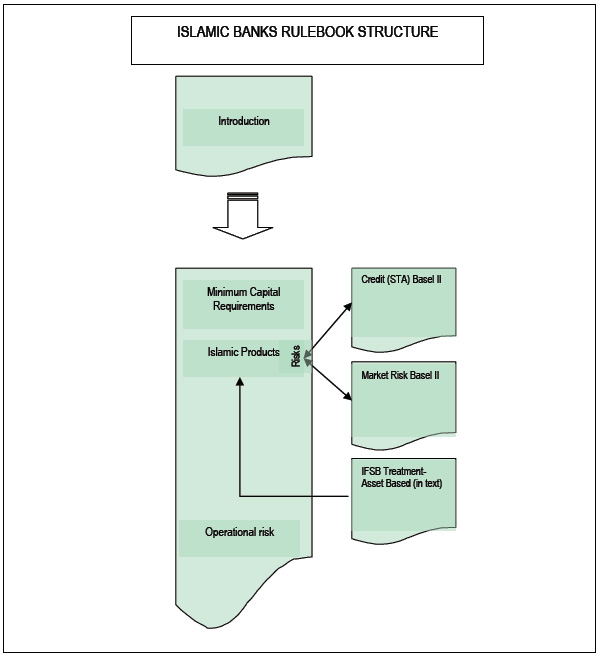

The CBB recognises that the Basel Committee guidelines may not address specific characteristics of the various products and services offered by Islamic banks. Therefore, the CBB has adopted a risk-based approach and has tailored the Rules to address the specific risk characteristics of Islamic banks. The structure of these Rules is explained on the next page.

Amended: January 2011

Apr 08CA-A.2.10

This Module provides support for certain other parts of the Rulebook, mainly:

(a) Prudential Consolidation and Deduction Requirements;(b) Licensing and Authorisation Requirements;(c) CBB Reporting Requirements;(d) Credit Risk Management;(e) Market Risk Management;(f) Operational Risk Management;(g) Liquidity Risk Management;(h) High Level Controls;(i) Relationship with Audit Firms; and(j) Penalties and Fines.

Amended: January 2011

Amended: January 2011

Apr 08