CA-9 CA-9 Market Risk — Interest Rate Risk — (STA)

CA-9.1 CA-9.1 Introduction

CA-9.1.1

This chapter describes the standardised approach for the measurement of the interest rate risk in the bank's trading book, in order to determine the capital requirement for this risk. The interest rate

exposure captured includesexposure arising from interest-bearing and discounted financial instruments,derivatives which are based on the movement of interest rates, foreign exchange forwards, and interest rateexposure embedded inderivatives which are based on non-interest rate related instruments.Apr 08CA-9.1.2

For the guidance of the banks, and without being exhaustive, the following list includes financial instruments in the trading book to which interest rate risk capital requirements will apply, irrespective of whether or not the instruments carry coupons:

(a) Bonds/loan stocks, debentures etc.;(b) Non-convertible preference shares;(c) Convertible securities such as preference shares and bonds, which are treated as debt instruments63;(d) Mortgage backed securities and other securitised assets64;(e) Certificates of Deposit;(f) Treasury bills, local authority bills, banker's acceptances;(g) Commercial paper;(h) Euronotes, medium term notes, etc.;(i) Floating rate notes, FRCDs etc.;(j) Foreign exchange forward positions;(k) Derivatives based on the above instruments and interest rates; and(l) Interest rate exposure embedded in other financial instruments.

63See Section CA-10.1 for an explanation of the circumstances in which convertible

securities should be treated as equity instruments. In other circumstances, they should be treated as debt instruments.64Traded mortgage

securities and mortgage derivative products possess unique characteristics because of the risk of pre-payment. It is possible that including such products within the standardised methodology as if they were similar to other securitised assets may not capture all the risks of holding positions in them. Banks which have traded mortgagesecurities and mortgage derivative products should discuss their proposed treatment with the CBB and obtain the CBB's prior written approval for it.Amended: January 2012

Amended: April 2011

Apr 08CA-9.1.3

A

security which is the subject of a repurchase orsecurities lending agreement will be treated as if it were still owned by the lender of thesecurity , i.e., it will be treated in the same manner as othersecurities positions.Apr 08CA-9.1.4

The minimum capital requirement is expressed in terms of two separately calculated charges, one applying to the "specific risk" of each security, whether it is a short or a long position, and the other to the interest rate risk in the portfolio (termed "general market risk") where long and short positions in different securities or instruments can be offset. The bank must, however, determine the specific risk capital charge for the correlation trading portfolio as follows: The bank computes (i) the total specific risk capital charges that would apply just to the net long positions from the net long correlation trading exposures combined, and (ii) the total specific risk capital charges that would apply just to the net short positions from the net short correlation trading exposures combined. The larger of these total amounts is then the specific risk capital charge for the correlation trading portfolio.

Amended: January 2012

Apr 08CA-9.1.4A

During a transitional period until 31 December 2013, the bank may exclude positions in securitisation instruments which are not included in the correlation trading portfolio from the calculation according to Paragraph CA-9.1.4 and determine the specific risk capital charge as follows: The bank computes (i) the total specific risk capital charge that would apply just to the net long positions in securitisation instruments in the trading book, and (ii) the total specific risk capital charge that would apply just to the net short positions in securitisation instruments in the trading book. The larger of these total amounts is then specific risk capital charge for the securitisation positions in the trading book. This calculation must be undertaken separately from the calculation for the correlation trading portfolio.

Added: January 2012CA-9.1.5

The specific risk capital requirement recognises that individual instruments may change in value for reasons other than shifts in the

yield curve of a given currency. The general risk capital requirement reflects the price change of these products caused by parallel and non-parallel shifts in theyield curve , as well as the difficulty of constructing perfect hedges.Apr 08CA-9.1.6

There is general market risk inherent in all interest rate risk positions. This may be accompanied by one or more out of specific interest rate risk,

counterparty risk, equity risk and foreign exchange risk, depending on the nature of the position. Banks must consider carefully which risks are generated by each individual position. It should be recognised that the identification of the risks will require the application of the appropriate level of technical skills and professional judgment.Apr 08CA-9.1.7

Banks which have the intention and capability to use internal models for the measurement of general and specific interest rate risks and, hence, for the calculation of the capital requirement, should seek the prior written approval of the CBB for those models. The CBB's detailed rules for the recognition and use of internal models are included in chapter CA-14. Banks which do not use internal models should adopt the standardised approach to calculate the interest rate risk capital requirement, as set out in detail in this chapter.

Apr 08CA-9.2 CA-9.2 Specific Risk Calculation

CA-9.2.1

The capital charge for specific risk is designed to protect against a movement in the price of an individual instrument, owing to factors related to the individual issuer.

Apr 08CA-9.2.2

In measuring the specific risk for interest rate related instruments, a bank may net, by value, long and short positions (including positions in

derivatives ) in the same debt instrument to generate the individual net position in that instrument. Instruments will be considered to be the same where the issuer is the same, they have an equivalent ranking in a liquidation, and the currency, the coupon and the maturity are the same.Apr 08CA-9.2.3

The specific risk capital requirement is determined by weighting the current market value of each individual net position, whether long or short, according to its allocation among the following broad categories:

Categories External credit assessment Specific risk capital charge Government (including GCC governments) AAA to AA- 0% A+ to BBB- 0.25% (residual term to final maturity 6 months or less)

1.00% (residual term to final maturity greater than 6 and up to and including 24 months)

1.60% (residual term to final maturity exceeding 24 months)BB+ to B- 8.00% Below B- 12.00% Unrated 8.00% Qualifying 0.25% (residual term to final maturity 6 months or less)

1.00% (residual term to final maturity greater than 6 and up to and including 24 months)

1.60% (residual term to final maturity exceeding 24 months)Other Similar to credit risk charges under the standardised approach, e.g.: BB+ to BB- 8.00% Below BB- 12.00% Unrated 8.00% Apr 08CA-9.2.4

When the government paper is denominated in the domestic currency and funded by the bank in the same currency, a 0% specific risk charge may be applied.

Apr 08CA-9.2.5

Central "government" debt instruments will include all forms of government paper, including bonds, treasury bills and other short-term instruments.

Apr 08CA-9.2.6

The CBB reserves the right to apply a specific risk weight to

securities issued by certain foreign governments, especially tosecurities denominated in a currency other than that of the issuing government.Apr 08CA-9.2.7

The "qualifying" category includes

securities issued by or fully guaranteed by public sector entities and multilateral development banks (refer to Paragraph CA-3.2.8), plus othersecurities that are:(a) Rated investment grade by at least two internationally recognised credit rating agencies (to be agreed with the CBB); or(b) Deemed to be of comparable investment quality by the reporting bank, provided that the issuer is rated investment grade by at least two internationally recognised credit rating agencies (to be agreed with the CBB); or(c) Rated investment grade by one credit rating agency and not less than investment grade by any internationally recognised credit rating agencies (to be agreed with the CBB); or(d) Unrated (subject to the approval of the CBB), but deemed to be of comparable investment quality by the reporting bank and where the issuer hassecurities listed on a recognised stock exchange, may also be included.Amended: January 2012

Amended: April 2011

Apr 08Specific Risk Rules for Unrated Debt Securities

CA-9.2.8

Unrated securities may be included in the "qualifying" category when they are (subject to CBB's approval) unrated, but deemed to be of comparable investment quality by the reporting bank, and the issuer has securities listed on a recognised stock exchange. This will remain unchanged for banks applying the standardised approach. For banks applying the IRB approach for a portfolio, unrated securities can be included in the "qualifying" category if both of the following conditions are met:

(a) The securities are rated equivalent65 to investment grade under the reporting bank's internal rating system, which the CBB has confirmed complies with the requirements for an IRB approach; and(b) The issuer has securities listed on a recognised stock exchange.Amended: April 2011

Apr 08Specific Risk Rules for Non-qualifying Issuers

CA-9.2.9

Instruments issued by a non-qualifying issuer will receive the same specific risk charge as a non-investment grade corporate borrower under the standardised approach for credit risk under chapter CA-4.

Apr 08CA-9.2.10

However, since this may in certain cases considerably underestimate the specific risk for debt instruments which have a high yield to redemption relative to government debt securities, CBB will have the discretion, on a case by case basis:

(a) To apply a higher specific risk charge to such instruments; and/or(b) To disallow offsetting for the purposes of defining the extent of general market risk between such instruments and any other debt instruments.Amended: April 2011

Apr 08CA-9.2.11

In that respect, securitisation exposures that would be subject to a deduction treatment under the securitisation framework set forth in chapter CA-6 (e.g. equity tranches that absorb first loss), as well as securitisation exposures that are unrated liquidity lines or letters of credit must be subject to a capital charge that is no less than the charge set forth in the securitisation framework.

Apr 08Specific Risk Rules for Positions Covered under the Securitisation Framework

CA-9.2.11A

The specific risk of securitisation positions as defined in Paragraphs CA-6.1.1 to CA-6.1.6 which are held in the trading book is to be calculated according to the method used for such positions in the banking book unless specified otherwise below. To that effect, the risk weight has to be calculated as specified below and applied to the net positions in securitisation instruments in the trading book. The total specific risk capital charge for the correlation trading portfolio is to be computed according to Paragraph CA-9.2.17, and the total specific risk capital charge for securitisation exposures is to be computed according to Paragraph CA-9.1.4.

Added: January 2012CA-9.2.11B

The specific risk capital charges for positions covered under the standardised approach for securitisation exposures are defined in the table below. These charges must be applied by banks using the standardised approach for credit risk. For positions with long-term ratings of B+ and below and short-term ratings other than A-1/P-1, A-2/P-2, A-3/P-3, deduction from capital as defined in Paragraph CA-6.4.2 is required. Deduction is also required for unrated positions with the exception of the circumstances described in Paragraphs CA-6.4.12 to CA-6.4.16. The operational requirements for the recognition of external credit assessments outlined in Paragraph CA-6.4.6 apply.

Specific Risk Capital Charges under the Standardised Approach Based on External Credit Ratings

External Credit Assessment AAA to AA-

A-1/P-1A+ to A-

A-2/P-2BBB+ to BBB-

A-3/P-3BB+ to BB- Below BB- and below

A-3/P-3 or unratedSecuritisation Exposures 1.6% 4% 8% 28% Deduction Re-securitisation Exposures 3.2% 8% 18% 52% Deduction Added: January 2012CA-9.2.11C

The specific risk capital charges for rated positions covered under the internal ratings-based approach for securitisation exposures are defined in the table below. For positions with long-term ratings of B+ and below and short-term ratings other than A-1/P-1, A-2/P-2, A-3/P-3, deduction from capital as defined in Paragraph CA-6.4.2 is required. The operational requirements for the recognition of external credit assessments outlined in Paragraph CA-6.4.6 apply:

(a) For securitisation exposures, banks may apply the capital charges defined in the table below for senior granular positions if the effective number of underlying exposures (N, as defined in CA-6.4.77) is 6 or more and the position is senior as defined in CA-6.4.55. When N is less than 6, the capital charges for non-granular securitisation exposures of the table below apply. In all other cases, the capital charges for non-senior granular securitisation exposures of the table below apply; and(b) Re-securitisation exposures as defined in Paragraph CA-6.1.5 are subject to specific risk capital charges depending on whether or not the exposure is senior as defined in Paragraph CA-6.4.55.

Specific risk capital charges based on external credit ratings (IRB) External rating

(illustrative)Securitisation exposures Re-securitisation exposures Senior, granular Non-senior, granular Non-granular Senior Non-senior AAA/A-1/P-1 0.56% 0.96% 1.60% 1.60% 2.40% AA 0.64% 1.20% 2.00% 2.00% 3.20% A+ 0.80% 1.44% 2.80% 2.80% 4.00% A/A-2/P-2 0.96% 1.60% 3.20% 5.20% A- 1.60% 2.80% 4.80% 8.00% BBB+ 2.80% 4.00% 8.00% 12.00% BBB/A-3/P-3 4.80% 6.00% 12.00% 18.00% BBB- 8.00% 16.00% 28.00% BB+ 20.00% 24.00% 40.00% BB 34.00% 40.00% 52.00% BB- 52.00% 60.00% 68.00% Below BB-/ A-3/P-3 Deduction

Added: January 2012CA-9.2.11D

The specific risk capital charges for unrated positions under the securitisation framework as defined in Paragraphs CA-6.1.1 to CA-6.1.6 will be calculated as set out below, subject to CBB approval:

(a) If a bank has approval for the internal ratings-based approach for the asset classes which include the underlying exposures, the bank may apply the supervisory formula approach (Paragraphs CA-6.4.66 to CA-6.4.81). When estimating PDs and LGDs for calculating KIRB, the bank must meet the minimum requirements for the IRB approach;(b) To the extent that a bank has approval to apply the internally developed approach referred to in CA-14.11.1B to the underlying exposures and the bank derives estimates for PDs and LGDs from the internally developed approach specified in Paragraphs CA-14.11.7 and CA-14.11.8 that are in line with the quantitative standards for the internal ratings-based approach, the bank may use these estimates for calculating KIRB and, consequently, for applying the supervisory formula approach (Paragraphs CA-6.4.66 to CA-6.4.81); and(c) In all other cases the capital charge can be calculated as 12% of the weighted average risk weight that would be applied to the securitised exposures under the standardised approach, multiplied by a concentration ratio. If the concentration ratio is 12.5 or higher the position has to be deducted from capital as defined in Paragraph CA-6.4.2. This concentration ratio is equal to the sum of the nominal amounts of all the tranches divided by the sum of the nominal amounts of the tranches junior to or pari passu with the tranche in which the position is held including that tranche itself.The resulting specific risk capital charge must not be lower than any specific risk capital charge applicable to a rated more senior tranche. If a bank is unable to determine the specific risk capital charge as described above or prefers not to apply the treatment described above to a position, it must deduct that position from capital.

Added: January 2012CA-9.2.11E

A position subject to deduction according to Paragraphs CA-9.2.11B to CA-9.2.11D may be excluded from the calculation of the capital charge for general market risk whether the bank applies the standardised measurement method or the internal models method for the calculation of its general market risk capital charge.

Added: January 2012Specific Risk Capital Charges for Positions Hedged by Credit Derivatives

CA-9.2.12

Full allowance will be recognised when the values of two legs (i.e. long and short) always move in the opposite direction and broadly to the same extent. This would be the case in the following situations:

(a) The two legs consist of completely identical instruments; or(b) A long cash position is hedged by a total rate of return swap (or vice versa) and there is an exact match between the reference obligation and the underlying exposure (i.e. the cash position).66In these cases, no specific risk capital requirement applies to both sides of the position.

65 Equivalent means the debt security has a one-year PD equal to or less than the one year PD implied by the long-run average one-year PD of a security rated investment grade or better by a qualifying rating agency.

66 The maturity of the swap itself may be different from that of the underlying exposure.

Amended: April 2011

Apr 08CA-9.2.13

An 80% offset will be recognised when the value of two legs (i.e. long and short) always moves in the opposite direction but not broadly to the same extent. This would be the case when a long cash position is hedged by a credit default swap or a credit linked note (or vice versa) and there is an exact match in terms of the reference obligation, the maturity of both the reference obligation and the credit derivative, and the currency to the underlying exposure. In addition, key features of the credit derivative contract (e.g. credit event definitions, settlement mechanisms) should not cause the price movement of the credit derivative to materially deviate from the price movements of the cash position. To the extent that the transaction transfers risk (i.e. taking account of restrictive payout provisions such as fixed payouts and materiality thresholds), an 80% specific risk offset will be applied to the side of the transaction with the higher capital charge, while the specific risk requirement on the other side will be zero.

Apr 08CA-9.2.14

Partial allowance will be recognised when the value of the two legs (i.e. long and short) usually moves in the opposite direction. This would be the case in the following situations:

(a) The position is captured in Paragraph CA-9.2.12 under (b), but there is an asset mismatch between the reference obligation and the underlying exposure. Nonetheless, the position meets the requirements in Paragraph CA-4.5.3 (g);(b) The position is captured in Paragraph CA-9.2.12 under (a) or CA-9.2.13 but there is a currency or maturity mismatch67 between the credit protection and the underlying asset; or(c) The position is captured in Paragraph CA-9.2.13 but there is an asset mismatch between the cash position and the credit derivative. However, the underlying asset is included in the (deliverable) obligations in the credit derivative documentation.

67 Currency mismatches should feed into the normal reporting of foreign exchange risk.

Amended: January 2012

Amended: April 2011

Apr 08CA-9.2.15

In each of these cases in Paragraphs CA-9.2.12 to CA-9.2.14, the following rule applies. Rather than adding the specific risk capital requirements for each side of the transaction (i.e. the credit protection and the underlying asset) only the higher of the two capital requirements will apply.

Amended: January 2012

Apr 08CA-9.2.16

In cases not captured in Paragraphs CA-9.2.12 to CA-9.2.14, a specific risk capital charge will be assessed against both sides of the position.

Amended: January 2012

Apr 08CA-9.2.17

An n-th-to-default credit derivative is a contract where the payoff is based on the n-th asset to default in a basket of underlying reference instruments. Once the n-th default occurs the transaction terminates and is settled:

(a) The capital charge for specific risk for a first-to-default credit derivative is the lesser of (1) the sum of the specific risk capital charges for the individual reference credit instruments in the basket, and (2) the maximum possible credit event payment under the contract. Where a bank has a risk position in one of the reference credit instruments underlying a first-to-default credit derivative and this credit derivative hedges the bank's risk position, the bank is allowed to reduce with respect to the hedged amount both the capital charge for specific risk for the reference credit instrument and that part of the capital charge for specific risk for the credit derivative that relates to this particular reference credit instrument. Where a bank has multiple risk positions in reference credit instruments underlying a first-to-default credit derivative this offset is allowed only for that underlying reference credit instrument having the lowest specific risk capital charge;(b) The capital charge for specific risk for an n-th-to-default credit derivative with n greater than one is the lesser of (1) the sum of the specific risk capital charges for the individual reference credit instruments in the basket but disregarding the (n-1) obligations with the lowest specific risk capital charges; and (2) the maximum possible credit event payment under the contract. For n-th-to-default credit derivatives with n greater than 1 no offset of the capital charge for specific risk with any underlying reference credit instrument is allowed;(c) If a first or other n-th-to-default credit derivative is externally rated, then the protection seller must calculate the specific risk capital charge using the rating of the derivative and apply the respective securitisation risk weights as specified in Paragraphs CA-9.2.11B or CA-9.2.11C, as applicable; and(d) The capital charge against each net n-th-to-default credit derivative position applies irrespective of whether the bank has a long or short position, i.e. obtains or provides protection.Amended: January 2012

Apr 08CA-9.3 CA-9.3 General Market Risk Calculation

CA-9.3.1

The capital requirements for general market risk are designed to capture the risk of loss arising from changes in market interest rates, i.e. the risk of parallel and non-parallel shifts in the

yield curve . A choice between two principal methods of measuring the general market risk is permitted, a "maturity" method and a "duration" method. In each method, the capital charge is the sum of the following four components:(a) The net short or long position in the whole trading book;(b) A small proportion of the matched positions in each time-band (the "vertical disallowance");(c) A larger proportion of the matched positions across different time-bands (the "horizontal disallowance"); and(d) A net charge for positions in options, where appropriate (see Section CA-13).Amended: January 2012

Amended: April 2011

Apr 08CA-9.3.2

Separate maturity ladders should be used for each currency and capital charges should be calculated for each currency separately and then summed, by applying the prevailing foreign exchange spot rates, with no off-setting between positions of opposite sign.

Apr 08CA-9.3.3

In the case of those currencies in which the value and volume of business is insignificant, separate maturity ladders for each currency are not required. Instead, the bank may construct a single maturity ladder and slot, within each appropriate time-band, the net long or short position for each currency. However, these individual net positions are to be summed within each time-band, irrespective of whether they are long or short positions, to arrive at the gross position figure for the time-band.

Apr 08CA-9.3.4

A combination of the two methods (referred to under Paragraph CA-9.3.1) is not permitted. Any exceptions to this rule will require the prior written approval of the CBB. It is expected that such approval will only be given in cases where a bank clearly demonstrates to the CBB, the difficulty in applying, to a definite category of trading instruments, the method otherwise chosen by the bank as the normal method. It is further expected that the CBB may, in future years, consider recognising the duration method as the approved method, and the use of the maturity method may be discontinued.

Amended: January 2012

Apr 08CA-9.4 CA-9.4 Maturity Method

CA-9.4.1

A worked example of the maturity method is included in Appendix CA-11. The various time-bands and their risk weights, relevant to the maturity method, are illustrated in Paragraph CA-9.4.2(a) below.

Amended: January 2012

Apr 08CA-9.4.2

The steps in the calculation of the general market risk for interest rate positions, under this method, are set out below:

(a) Individual long or short positions in interest-rate related instruments, including derivatives, are slotted into a maturity ladder comprising thirteen time-bands (or fifteen time-bands in the case of zero-coupon and deep-discount instruments, defined as those with a coupon of less than 3%), on the following basis:(i) Fixed rate instruments are allocated according to their residual term to maturity (irrespective of embedded puts and calls), and whether their coupon is below 3%;(ii) Floating rate instruments are allocated according to the residual term to the next repricing date;(iii) Positions in derivatives, and all positions in repos, reverse repos and similar products are decomposed into their components within each time band. Derivative instruments are covered in greater detail in Sections CA-9.6 to CA-9.9;(iv) Opposite positions of the same amount in the same issues (but not different issues by the same issuer), whether actual or notional, can be omitted from the interest rate maturity framework, as well as closely matched swaps, forwards, futures and FRAs which meet the conditions set out in Section CA-9.8. In other words, these positions are netted within their relevant time-bands; and(v) The CBB's advice must be sought on the treatment of instruments that deviate from the above structures, or which may be considered sufficiently complex to warrant the CBB's attention.Maturity Method: Time-bands and Risk Weights

Coupon 3% or more Coupon < 3% Risk weight Zone 1 1 month or less 1 month or less 0.00% 1 to 3 months 1 to 3 months 0.20% 3 to 6 months 3 to 6 months 0.40% 6 to 12 months 6 to 12 months 0.70% Zone 2 1 to 2 years 1 to 1.9 years 1.25% 2 to 3 years 1.9 to 2.8 years 1.75% 3 to 4 years 2.8 to 3.6 years 2.25% Zone 3 4 to 5 years 3.6 to 4.3 years 2.75% 5 to 7 years 4.3 to 5.7 years 3.25% 7 to 10 years 5.7 to 7.3 years 3.75% 10 to 15 years 7.3 to 9.3 years 4.50% 15 to 20 years 9.3 to 10.6 years 5.25% > 20 years 10.6 to 12 years 6.00% 12 to 20 years 8.00% > 20 years 12.50% (b) The market values of the individual long and short net positions in each maturity band are multiplied by the respective risk weighting factors given in Paragraph CA-9.4.2(a) above;(c) Matching of positions within each maturity band (i.e. vertical matching) is done as follows:(i) Where a maturity band has both weighted long and short positions, the extent to which the one offsets the other is called the matched weighted position. The remainder (i.e. the excess of the weighted long positions over the weighted short positions, or vice versa, within a band) is called the unmatched weighted position for that band.(d) Matching of positions, across maturity bands, within each zone (i.e. horizontal matching - level 1), is done as follows:(i) Where a zone has both unmatched weighted long and short positions for various bands, the extent to which the one offsets the other is called the matched weighted position for that zone. The remainder (i.e. the excess of the weighted long positions over the weighted short positions, or vice versa, within a zone) is called the unmatched weighted position for that zone.(e) Matching of positions, across zones (i.e. horizontal matching - level 2), is done as follows:(i) The unmatched weighted long or short position in zone 1 may be offset against the unmatched weighted short or long position in zone 2. The extent to which the unmatched weighted positions in zones 1 and 2 are offsetting is described as the matched weighted position between zones 1 and 2.(ii) After step (i) above, any residual unmatched weighted long or short position in zone 2 may be matched by offsetting the unmatched weighted short or long position in zone 3. The extent to which the unmatched positions in zones 2 and 3 are offsetting is described as the matched weighted position between zones 2 and 3.The calculations in steps (i) and (ii) above may be carried out in reverse order (i.e. zones 2 and 3, followed by zones 1 and 2).(i) After steps (i) and (ii) above, any residual unmatched weighted long or short position in zone 1 may be matched by offsetting the unmatched weighted short or long position in zone 3. The extent to which the unmatched positions in zones 1 and 3 are offsetting is described as the matched weighted position between zones 1 and 3.(f) Any residual unmatched weighted positions, following the matching within and between maturity bands and zones as described above, will be summed.(g) The general interest rate risk capital requirement is the sum of:(i) Matched weighted positions in all maturity bandsx 10% (ii) Matched weighted positions in zone 1x 40% (iii) Matched weighted positions in zone 2x 30% (iv) Matched weighted positions in zone 3x 30% (v) Matched weighted positions between zones 1 & 2x 40% (vi) Matched weighted positions between zones 2 & 3x 40% (vii) Matched weighted positions between zones 1 & 3x 100% (viii) Residual unmatched weighted positionsx 100% Item (i) is referred to as the vertical disallowance, items (ii) through (iv) as the first set of horizontal disallowances, and items (v) through (vii) as the second set of horizontal disallowances.

Amended: January 2012

Amended: April 2011

Apr 08CA-9.5 CA-9.5 Duration Method

CA-9.5.1

The duration method is an alternative approach to measuring the

exposure to parallel and non-parallel shifts in theyield curve , and recognises the use of duration as an indicator of the sensitivity of individual positions to changes in market yields. Under this method, banks may use a duration-based system for determining their general interest rate risk capital requirements for traded debt instruments and other sources of interest rateexposures includingderivatives . A worked example of the duration method is included in Appendix CA-12. The various time-bands and assumed changes in yield, relevant to the duration method, are illustrated below.Duration Method: Time-bands and Assumed Changes in Yield

Time-band Assumed change in yield Zone 1 1 month or less 1.00 1 to 3 months 1.00 3 to 6 months 1.00 6 to 12 months 1.00 Zone 2 1 to 1.9 years 0.90 1.9 to 2.8 years 0.80 2.8 to 3.6 years 0.75 Zone 3 3.6 to 4.3 years 0.75 4.3 to 5.7 years 0.70 5.7 to 7.3 years 0.65 7.3 to 9.3 years 0.60 9.3 to 10.6 years 0.60 10.6 to 12 years 0.60 12 to 20 years 0.60 > 20 years 0.60 Amended: April 2011

Apr 08CA-9.5.2

Banks must notify the CBB of the circumstances in which they elect to use this method. Once chosen, the duration method must be consistently applied, in accordance with the requirements of Section CA-9.3.

Amended: January 2012

Apr 08CA-9.5.3

Where a bank has chosen to use the duration method, it is possible that it will not be suitable for certain instruments. In such cases, the bank must seek the advice of the CBB or obtain approval for application of the maturity method to the specific category(ies) of instruments, in accordance with the provisions of Section CA-9.3.

Amended: January 2012

Apr 08CA-9.5.4

The steps in the calculation of the general market risk for interest rate positions, under this method, are set out below:

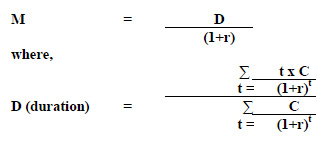

(a) The bank will determine theYield-to-Maturity (YTM) for each individual net position in fixed rate and floating rate instruments, based on the current market value. The basis of arriving at individual net positions is explained in Section CA-9.4 above. TheYTM for fixed rate instruments is determined without any regard to whether the instrument is coupon bearing, or whether the instrument has any embedded options. In all cases,YTM for fixed rate instruments is calculated with reference to the final maturity date and, for floating rate instruments, with reference to the next repricing date;(b) The bank will calculate, for each debt instrument, the modified duration (M) on the basis of the following formula:

r =YTM % per annum expressed as a decimal

C = Cash flow at time t

t = time at which cash flows occur, in years

m = time to maturity, in years(c) Individual net positions, at current market value, are allocated to the time-bands illustrated in Paragraph CA-9.5.1, based on their modified duration;(d) The bank will then calculate the modified duration-weighted position for each individual net position by multiplying its current market value by the modified duration and the assumed change in yield;(e) Matching of positions within each time band (i.e. vertical matching) is done as follows:• Where a time band has both weighted long and short positions, the extent to which the one offsets the other is called the matched weighted position. The remainder (i.e. the excess of the weighted long positions over the weighted short positions, or vice versa, within a band) is called the unmatched weighted position for that band.(f) Matching of positions, across time bands, within each zone (i.e. horizontal matching - level 1), is done as follows:• Where a zone has both unmatched weighted long and short positions for various bands, the extent to which the one offsets the other is called the matched weighted position for that zone. The remainder (i.e. the excess of the weighted long positions over the weighted short positions, or vice versa, within a zone) is called the unmatched weighted position for that zone.(g) Matching of positions, across zones (i.e. horizontal matching - level 2), is done as follows:(i) The unmatched weighted long or short position in zone 1 may be offset against the unmatched weighted short or long position in zone 2. The extent to which the unmatched weighted positions in zones 1 and 2 are offsetting is described as the matched weighted position between zones 1 and 2.(ii) After step (i) above, any residual unmatched weighted long or short position in zone 2 may be matched by offsetting the unmatched weighted short or long position in zone 3. The extent to which the unmatched positions in zones 2 and 3 are offsetting is described as the matched weighted position between zones 2 and 3.The calculations in steps (i) and (ii) above may be carried out in reverse order (i.e. zones 2 and 3, followed by zones 1 and 2).(iii) After steps (a) and (b) above, any residual unmatched weighted long or short position in zone 1 may be matched by offsetting the unmatched weighted short or long position in zone 3. The extent to which the unmatched positions in zones 1 and 3 are offsetting is described as the matched weighted position between zones 1 and 3.(h) Any residual unmatched weighted positions, following the matching within and between maturity bands and zones as described above, will be summed; and(i) The general interest rate risk capital requirement is the sum of:(i) Matched weighted positions in all maturity bandsx 5% (ii) Matched weighted positions in zone 1x 40% (iii) Matched weighted positions in zone 2x 30% (iv) Matched weighted positions in zone 3x 30% (v) Matched weighted positions between zones 1 & 2x 40% (vi) Matched weighted positions between zones 2 & 3x 40% (vii) Matched weighted positions between zones 1 & 3x 100% (viii) Residual unmatched weighted positionsx 100% Item (i) is referred to as the vertical disallowance, items (ii) through (iv) as the first set of horizontal disallowances, and items (v) through (vii) as the second set of horizontal disallowances.

Amended: January 2012

Amended: April 2011

Apr 08CA-9.6 CA-9.6 Derivatives

CA-9.6.1

Banks which propose to use internal models to measure the interest rate risk inherent in

derivatives will seek the prior written approval of the CBB for applying those models. The use of internal models to measure market risk, and the CBB's rules applicable to them, are discussed in detail in chapter CA-14.Apr 08CA-9.6.2

Where a bank, with the prior written approval of the CBB, uses an interest rate sensitivity model, the output of that model is used, by the duration method, to calculate the general market risk as described in Section CA-9.5.

Amended: January 2012

Apr 08CA-9.6.3

Where a bank does not propose to use models, it must use the techniques described in the following Paragraphs, for measuring the market risk on interest rate

derivatives . The measurement system should include all interest ratederivatives and off-balance-sheet instruments in the trading book which react to changes in interest rates (e.g. forward rate agreements, other forward contracts, bond futures, interest rate and cross-currencyswaps , options and forward foreign exchange contracts). Where a bank has obtained the approval of the CBB for the use of non-interest ratederivatives models, the embedded interest rateexposures should be incorporated in the standardised measurement framework described in Sections CA-9.7 to CA-9.9.Amended: January 2012

Apr 08CA-9.6.4

Derivative positions will attract specific risk only when they are based on an underlying instrument or

security . For instance, where the underlyingexposure is an interest rateexposure , as in aswap based upon inter-bank rates, there will be no specific risk, but onlycounterparty risk. A similar treatment applies to FRAs, forward foreign exchange contracts and interest rate futures. However, for aswap based on a bond yield, or a futures contract based on a debtsecurity or an index representing a basket of debtsecurities , the credit risk of the issuer of the underlying bond will generate a specific risk capital requirement. Future cash flows derived from positions inderivatives will generatecounterparty risk requirements related to thecounterparty in the trade, in addition to position risk requirements (specific and general market risk) related to the underlyingsecurity .Apr 08CA-9.7 CA-9.7 Calculation of Derivative Positions

CA-9.7.1

The

derivatives should be converted to positions in the relevant underlying and become subject to specific and general market risk charges as described in Sections CA-9.2 and CA-9.3, respectively. For the purpose of calculation by the standard formulae, the amounts reported are the market values of the principal amounts of the underlying or of the notional underlying. For instruments where the apparent notional amount differs from the effective notional amount, banks must use the latter.Amended: January 2012

Apr 08CA-9.7.2

The remaining Paragraphs in this Section include the guidelines for the calculation of positions in different categories of interest rate

derivatives . Banks which need further assistance in the calculation, particularly in relation to complex instruments, should contact the CBB in writing.Amended: January 2012

Apr 08Forward Foreign Exchange Contracts

CA-9.7.3

A forward foreign exchange position is decomposed into legs representing the paying and receiving currencies. Each of the legs is treated as if it were a zero coupon bond, with zero specific risk, in the relevant currency and included in the measurement framework as follows:

(a) If the maturity method is used, each leg is included at the notional amount; and(b) If the duration method is used, each leg is included at the present value of the notional zero coupon bond.Amended: April 2011

Apr 08Deposit Futures and FRAs

CA-9.7.4

Deposit futures, forward rate agreements and other instruments where the underlying is a money market

exposure will be split into two legs as follows:(a) The first leg will represent the time to expiry of the futures contract, or settlement date of the FRA as the case may be;(b) The second leg will represent the time to expiry of the underlying instrument;(c) Each leg will be treated as a zero coupon bond with zero specific risk; and(d) For deposit futures, the size of each leg is the notional amount of the underlying money marketexposure . For FRAs, the size of each leg is the notional amount of the underlying money marketexposure discounted to present value, although in the maturity method, the notional amount may be used without discountingFor example, under the maturity method, a single 3-month Euro$ 1,000,000 deposit futures contract expiring in 3 months' time will have one leg of $ 1,000,000 representing the 8 months to contract expiry, and another leg of $ 1,000,000 in the 11 months' time-band representing the time to expiry of thedeposit underlying the futures contract.Amended: April 2011

Apr 08Bond futures and Forward Bond Transactions

CA-9.7.5

Bond futures, forward bond transactions and the forward leg of repos, reverse repos and other similar transactions will use the two-legged approach. A forward bond transaction is one where the settlement is for a period other than the prevailing norm for the market:

(a) The first leg is a zero coupon bond with zero specific risk. Its maturity is the time to expiry of the futures or forward contract. Its size is the cash flow on maturity discounted to present value, although in the maturity method, the cash flow on maturity may be used without discounting;(b) The second leg is the underlying bond. Its maturity is that of the underlying bond for fixed rate bonds, or the time to the next reset for floating rate bonds. Its size is as set out in (c) and (d) below;(c) For forward bond transactions, the underlying bond and amount is used at the present spot price;(d) For bond futures, the principal amounts for each of the two legs is reckoned as the futures price times the notional underlying bond amount;(e) Where a range of deliverable instruments may be delivered to fulfill a futures contract (at theoption of the "short"), then the following rules are used to determine the principal amount, taking account of any conversion factors defined by the exchange:(i) The "long" may use one of the deliverable bonds, or the notional bond on which the contract is based, as the underlying instrument, but this notional long leg may not be offset against a short cash position in the same bond.(ii) The "short" may treat the notional underlying bond as if it were one of the deliverable bonds, and it may be offset against a short cash position in the same bond;(f) For futures contracts based on a corporate bond index, the positions will be included at the market value of the notional underlying portfolio ofsecurities ;(g) Arepo (or sell-buy or stock lending) involving exchange of asecurity for cash should be represented as a cash borrowing - i.e. a short position in a government bond with maturity equal to therepo and coupon equal to therepo rate. A reverserepo (or buy-sell or stock borrowing) should be represented as a cash loan - i.e. a long position in a government bond with maturity equal to the reverserepo and coupon equal to therepo rate. These positions are referred to as "cash legs"; and(h) It should be noted that, where asecurity owned by the bank (and included in its calculation of market risk) isrepo 'd, it continues to contribute to the bank's interest rate or equity position risk calculation.Amended: April 2011

Apr 08Swaps

CA-9.7.6

Swaps are treated as two notional positions in governmentsecurities with the relevant maturities:(a) Interest rateswaps will be decomposed into two legs, and each leg will be allocated to the maturity band equating to the time remaining to repricing or maturity. For example, an interest rateswap in which a bank is receiving floating rate interest and paying fixed is treated as a long position in a floating rate instrument of maturity equivalent to the period until the next interest fixing and a short position in a fixed rate instrument of maturity equivalent to the residual life of theswap ;(b) Forswaps that pay or receive a fixed or floating interest rate against some other reference price, e.g. a stock index, the interest rate component should be slotted into the appropriate repricing or maturity category, with the equity component being included in the equity risk measurement framework as described in chapter CA-10;(c) For cross currencyswaps , the separate legs are included in the interest rate risk measurement for the currencies concerned, as having a fixed/floating leg in each currency. Alternatively, the two parts of a currencyswap transaction are split into forward foreign exchange contracts and treated accordingly;(d) Where aswap has a deferred start, and one or both legs have been fixed, then the fixed leg(s) will be sub-divided into the time to the commencement of the leg and the actualswap leg with fixed or floating rate. Aswap is deemed to have a deferred start when the commencement of the interest rate calculation periods is more than two business days from the transaction date, and one or both legs have been fixed at the time of the commitment. However, when aswap has a deferred start and neither leg has been fixed, there is no interest rateexposure , albeit there will becounterparty exposure ; and(e) Where aswap has a different structure from those discussed above, it may be necessary to adjust the underlying notional principal amount, or the notional maturity of one or both legs of the transaction.Amended: April 2011

Apr 08CA-9.7.7

Banks with large

swap books may use alternative formulae for theseswaps to calculate the positions to be included in the maturity or duration ladder. One method would be to first convert the cash flows required by theswap into their present values. For this purpose, each cash flow should be discounted using the zero coupon yields, and a single net figure for the present value of the cash flows entered into the appropriate time-band using procedures that apply to zero or low coupon (less than 3%) instruments. An alternative method would be to calculate the sensitivity of the net present value implied by the change in yield used in the duration method (as set out in Section CA-9.5), and allocate these sensitivities into the appropriate time-bands.Amended: January 2012

Apr 08CA-9.7.8

Banks which propose to use the approaches described in Paragraph CA-9.7.7, or any other similar alternative formulae, should obtain the prior written approval of the CBB. The CBB will consider the following factors before approving any alternative methods for calculating the

swap positions:(a) Whether the systems proposed to be used are accurate;(b) Whether the positions calculated fully reflect the sensitivity of the cash flows to interest rate changes and are entered into the appropriate time-bands; and(c) Whether the positions are denominated in the same currency.Amended: January 2012

Apr 08CA-9.8 CA-9.8 Netting of Derivative Positions

Permissible Offsetting of Fully Matched Positions for Both Specific and General Market Risk

CA-9.8.1

Banks may exclude from the interest rate risk calculation, altogether, the long and short positions (both actual and notional) in identical instruments with exactly the same issuer, coupon, currency and maturity. A matched position in a future or a forward and its corresponding underlying may also be fully offset, albeit the leg representing the time to expiry of the future is included in the calculation.

Apr 08CA-9.8.2

When the future or the forward comprises a range of deliverable instruments, offsetting of positions in the futures or forward contract and its underlying is only permitted in cases where there is a readily identifiable underlying

security which is most profitable for the trader with a short position to deliver. The price of thissecurity , sometimes called the "cheapest-to-deliver", and the price of the future or forward contract should, in such cases, move in close alignment. No offsetting will be allowed between positions in different currencies. The separate legs of cross-currencyswaps or forward foreign exchange contracts are treated as notional positions in the relevant instruments and included in the appropriate calculation for each currency.Apr 08Permissible Offsetting of Closely Matched Positions for General Market Risk Only

CA-9.8.3

For the purpose of calculation of the general market risk, in addition to the permissible offsetting of fully matched positions as described in Paragraph CA-9.8.1 above, opposite positions giving rise to interest rate

exposure can be offset if they relate to the same underlying instruments, are of the same nominal value and are denominated in the same currency and, in addition, fulfill the following conditions:(a) For futures:

Offsetting positions in the notional or underlying instruments to which the futures contract relates should be for identical products and mature within seven days of each other.(b) Forswaps and FRAs:

The reference rate (for floating rate positions) must be identical and the coupons must be within 15 basis points of each other.(c) Forswaps , FRAs and forwards:

The next interest fixing date or, for fixed coupon positions or forwards, the residual maturity must correspond within the following limits:• Less than one month:same day; • Between one month and one year:within 7 days; • Over one year:within 30 days. Amended: January 2012

Amended: April 2011

Apr 08CA-9.9 CA-9.9 Calculation of Capital Charge for Derivatives

CA-9.9.1

After calculating the

derivatives positions, taking account of the permissible offsetting of matched positions, as explained in Section CA-9.8, the capital charges for specific and general market risk for interest ratederivatives are calculated in the same manner as for cash positions, as described earlier in this chapter.Summary of Treatment of Interest Rate Derivatives

Instrument Specific risk charge* General market risk charge Exchange-traded futures -Government** debt security No Yes, as two positions -Corporate debt security Yes Yes, as two positions -Index on interest rates (e.g. LIBOR) No Yes, as two positions -Index on basket of debt securities Yes Yes, as two positions OTC forwards-Government** debt security No Yes, as two positions -Corporate debt security Yes Yes, as two positions -Index on interest rates No Yes, as two positions FRAs No Yes, as two positions Swaps -Based on inter-bank rates No Yes, as two positions -Based on Government** bond yields No Yes, as two positions -Based on corporate bond yields Yes Yes, as two positions Forward foreign exchange No Yes, as one position in each currency Options -Government** debt security No Either (a) or (b) as below (see chapter CA-13 for a detailed description): (a) Carve out together with the associatedhedging positions, and use:-simplified approach; or-scenario analysis; or-internal models (see chapter CA-14).(b) General market risk charge according to the delta-plus method (gamma and vega should receive separate capital charges).-Corporate debt security Yes -Index on interest rates No -FRAs, swaps No * This is the specific risk charge relating to the issuer of the instrument. Under the credit risk rules, there remains a separate capital charge for the counterparty risk.

** As defined in Section CA-9.2.Amended: January 2012

Amended: April 2011

Apr 08