CA-6.4.74

L is measured (in decimal form) as the ratio of (a) the amount of all securitisation exposures subordinate to the tranche in question to (b) the amount of exposures in the pool. Banks must determine L before considering the effects of any tranche-specific credit enhancements, such as third-party guarantees that benefit only a single tranche. Any gain-on-sale and/or credit enhancing I/Os associated with the securitisation are not to be included in the measurement of L. The size of interest rate or currency swaps that are more junior than the tranche in question may be measured at their current values (without the potential future exposures) in calculating the enhancement level. If the current value of the instrument cannot be measured, the instrument should be ignored in the calculation of L.

Apr 08

CA-6.4.81

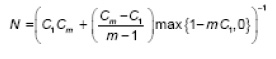

Under the conditions provided below, banks may employ a simplified method for calculating the effective number of exposures and the exposure-weighted average LGD. Let Cm in the simplified calculation denote the share of the pool corresponding to the sum of the largest 'm' exposures (e.g. a 15% share corresponds to a value of 0.15). The level of m is set by each bank:

(a) If the portfolio share associated with the largest exposure, C1, is no more than 0.03 (or 3% of the underlying pool), then for purposes of the SF, the bank may set LGD=0.50 and N equal to the following amount:5.

(b) Alternatively, if only C1 is available and this amount is no more than 0.03, then the bank may set LGD=0.50 and N=1/ C1.Amended: April 2011

(b) Alternatively, if only C1 is available and this amount is no more than 0.03, then the bank may set LGD=0.50 and N=1/ C1.Amended: April 2011

Apr 08

CA-6.4.80

For securitisations involving retail exposures, subject to CBB review, the SF may be implemented by applying the simplifications: h = 0 and v = 0.

Apr 08