(iv) Effective Maturity (M)

CA-5.3.45

Effective maturity (M) will be 2.5 years except for repo-style transactions where the effective maturity will be 6 months. However, banks can apply to CBB for approval to measure M for each facility using the definition provided below.

Apr 08CA-5.3.46

Except as noted in proceeding paragraph, M is defined as the greater of one year and the remaining effective maturity in years as defined below. In all cases, M will be no greater than 5 years:

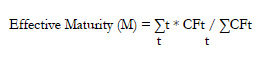

(a) For an instrument subject to a determined cash flow schedule, effective maturity M is defined as:

where CFt denotes the cash flows (principal, interest payments and fees) contractually payable by the borrower in period t.(b) If a bank is not in a position to calculate the effective maturity of the contracted payments as noted above, it is allowed to use a more conservative measure of M such as that it equals the maximum remaining time (in years) that the borrower is permitted to take to fully discharge its contractual obligation (principal, interest, and fees) under the terms of loan agreement. Normally, this will correspond to the nominal maturity of the instrument; and(c) For derivatives subject to a master netting agreement, the weighted average maturity of the transactions should be used when applying the explicit maturity adjustment. Further, the notional amount of each transaction should be used for weighting the maturity.Amended: April 2011

Apr 08CA-5.3.47

The one-year floor does not apply to certain short-term exposures, comprising fully or nearly-fully collateralised44 capital market-driven transactions (i.e. OTC derivatives transactions and margin lending) and repo-style transactions (i.e. repos/reverse repos and securities lending/borrowing) with an original maturity of less then one year, where the documentation contains daily remargining clauses. For all eligible transactions the documentation must require daily revaluation, and must include provisions that must allow for the prompt liquidation or setoff of the collateral in the event of default or failure to re-margin. The maturity of such transactions must be calculated as the greater of one-day, and the effective maturity (M, consistent with the definition above).

44 The intention is to include both parties of a transaction meeting these conditions where neither of the parties is systematically under-collateralised.

Apr 08CA-5.3.48

In addition to the transactions considered in the preceding paragraph above, other short-term exposures with an original maturity of less than one year that are not part of a bank's ongoing financing of an obligor are eligible for exemption from the one-year floor. Such transactions include:

(a) Some capital market-driven transactions and repo-style transactions that might not fall within the scope of the preceding paragraph;(b) Some short-term self-liquidating trade transactions. Import and export letters of credit and similar transactions could be accounted for at their actual remaining maturity;(c) Some exposures arising from settling securities purchases and sales. This could also include overdrafts arising from failed securities settlements provided that such overdrafts do not continue more than a short, fixed number of business days;(d) Some exposures arising from cash settlements by wire transfer, including overdrafts arising from failed transfers provided that such overdrafts do not continue more than a short, fixed number of business days;(e) Some exposures to banks arising from foreign exchange settlements; and(f) Some short-term loans and deposits.Apr 08CA-5.3.49

For transactions falling within the scope of paragraph CA-5.3.47 subject to a master netting agreement, the weighted average maturity of the transactions should be used when applying the explicit maturity adjustment. A floor equal to the minimum holding period for the transaction type set out in paragraph CA-4.3.11 will apply to the average. Where more than one transaction type is contained in the master netting agreement a floor equal to the highest holding period will apply to the average. Further, the notional amount of each transaction should be used for weighting maturity.

Apr 08CA-5.3.50

Where there is no explicit adjustment, the effective maturity (M) assigned to all exposures is set at 2.5 years unless otherwise specified in paragraph CA-5.3.45.

Apr 08