2. Risk Components

(i) Probability of Default (PD)

CA-5.3.17

For corporate and bank exposures, the PD is the greater of the one-year PD associated with the internal borrower grade to which that exposure is assigned, or 0.03%. For sovereign exposures, the PD is the one-year PD associated with the internal borrower grade to which that exposure is assigned. The PD of borrowers assigned to a default grade(s), consistent with the reference definition of default, is 100%. The minimum requirements for the derivation of the PD estimates associated with each internal borrower grade are outlined in paragraphs CA-5.8.72 to CA-5.8.74.

Apr 08(ii) Loss Given Default (LGD)

— Treatment of Unsecured Claims and Non-recognised Collateral

CA-5.3.18

Under the foundation approach, senior claims on corporates, sovereigns and banks not secured by recognised collateral will be assigned a 45% LGD.

Apr 08CA-5.3.19

All subordinated claims on corporates, sovereigns and banks must be assigned a 75% LGD. A subordinated loan is a facility that is expressly subordinated to another facility. This also includes economic subordination, such as cases where the facility is unsecured and the bulk of the borrower's assets are used to secure other exposures. CBB will review subordinated claims on a case by case basis. In case the subordinated claim (i) is on a banking, securities or other financial entity and (ii) exceeds (when combined with other investments in regulatory capital instruments of the investee) 20% of the concerned investee's eligible regulatory capital, such holding must be treated as described in Prudential Consolidation and Deduction Requirements Module.

Apr 08— Collateral under the Foundation Approach

CA-5.3.20

In addition to the eligible financial collateral recognised in the standardised approach, under the foundation IRB approach some other forms of collateral, known as eligible IRB collateral, are also recognised. These include receivables, specified commercial and residential real estate (CRE/RRE), and other collateral, where they meet the minimum requirements set out in paragraphs CA-5.8.119 to CA-5.8.134.40 For eligible financial collateral, the requirements are identical to the operational standards as set out in chapter CA-4.

40 The LGD applied to the collateralised portion of such exposures, subject to the limitations set out in paragraphs CA-4.2.1 to CA-4.3.25 of the standardised approach, will be set at 35%. The LGD applied to the remaining portion of this exposure will be set at 45%.

Apr 08— Methodology for Recognition of Eligible Financial Collateral under the Foundation Approach

CA-5.3.21

The methodology for the recognition of eligible financial collateral closely follows that outlined in the comprehensive approach to collateral in the standardised approach in paragraphs CA-4.3.3 to CA-4.3.25. The simple approach to collateral presented in the standardised approach will not be available to banks applying the IRB approach.

Apr 08CA-5.3.22

Following the comprehensive approach, the effective loss given default (LGD*) applicable to a collateralised transaction can be expressed as follows, where:

(a) LGD is that of the senior unsecured exposure before recognition of collateral (45%);(b) E is the current value of the exposure (i.e. cash lent or securities lent or posted);(c) E* is the exposure value after risk mitigation as determined in paragraphs CA-4.3.3 to CA-4.3.6 of the standardised approach. This concept is only used to calculate LGD*. Banks must continue to calculate EAD without taking into account the presence of any collateral, unless otherwise specified.LGD* = LGD × (E* / E)

Apr 08CA-5.3.23

Banks that qualify for the foundation IRB approach may calculate E* using any of the ways specified under the comprehensive approach for collateralised transactions under the standardised approach.

Apr 08CA-5.3.24

Where repo-style transactions are subject to a master netting agreement, a bank may choose not to recognise the netting effects in calculating capital. Banks that want to recognise the effect of master netting agreements on such transactions for capital purposes must satisfy the criteria provided in paragraph CA-4.3.17 and CA-4.3.18 of the standardised approach. The bank must calculate E* in accordance with paragraphs CA-4.3.20 and 4.3.21 or CA-4.3.22 to 4.3.25 and equate this to EAD. The impact of collateral on these transactions may not be reflected through an adjustment to LGD.

Apr 08— Carve Out from the Comprehensive Approach

— Methodology for Recognition of Eligible IRB Collateral

CA-5.3.26

The methodology for determining the effective LGD under the foundation approach for cases where banks have taken eligible IRB collateral to secure a corporate exposure is as follows:

(a) Exposures where the minimum eligibility requirements are met, but the ratio of the current value of the collateral received (C) to the current value of the exposure (E) is below a threshold level of C* (i.e. the required minimum collateralisation level for the exposure) would receive the appropriate LGD for unsecured exposures or those secured by collateral which is not eligible financial collateral or eligible IRB collateral;(b) Exposures where the ratio of C to E exceeds a second, higher threshold level of C** (i.e. the required level of over-collateralisation for full LGD recognition) would be assigned an LGD according to the following table.The following table displays the applicable LGD and required over-collateralisation levels for the secured parts of senior exposures:

Minimum LGD for Secured Portion of Senior Exposures

Minimum LGD Required minimum collateralisation level of the exposure (C*) Required level of over-collateralisation for full LGD recognition (C**) Eligible Financial collateral 0% 0% n.a. Receivables 35% 0% 125% CRE/RRE 35% 30% 140% Other collateral41 40% 30% 140% (a) Senior exposures are to be divided into fully collateralised and un-collateralised portions;(b) The part of the exposure considered to be fully collateralised, C/C**, receives the LGD associated with the type of collateral;(c) The remaining part of the exposure is regarded as unsecured and receives an LGD of 45%.

41 Other collateral excludes physical assets acquired by the bank as a result of a loan default.

Amended: April 2011

Apr 08— Methodology for the Treatment of Pools of Collateral

CA-5.3.27

The methodology for determining the effective LGD of a transaction under the foundation approach where banks have taken both financial collateral and other eligible IRB collateral is aligned to the treatment in the standardised approach and based on the following guidance:

(a) In the case where a bank has obtained multiple forms of CRM, it will be required to subdivide the adjusted value of the exposure (after the haircut for eligible financial collateral) into portions each covered by only one CRM type. That is, the bank must divide the exposure into the portion covered by eligible financial collateral, the portion covered by receivables, the portion covered by CRE/RRE collateral, a portion covered by other collateral, and an unsecured portion, where relevant;(b) Where the ratio of the sum of the value of CRE/RRE and other collateral to the reduced exposure (after recognising the effect of eligible financial collateral and receivables collateral) is below the associated threshold level (i.e. the minimum degree of collateralisation of the exposure), the exposure would receive the appropriate unsecured LGD value of 45%; and(c) The risk-weighted assets for each fully secured portion of exposure must be calculated separately.Amended: April 2011

Apr 08— Treatment of Certain Repo-style Transactions

CA-5.3.28

Banks that want to recognise the effects of master netting agreements on repo-style transactions for capital purposes must apply the methodology outlined in paragraph CA-5.3.24 for determining E* for use as the EAD.

Apr 08— Treatment of Guarantees and Credit Derivatives

CA-5.3.29

CRM in the form of guarantees and credit derivatives must not reflect the effect of double default (see paragraph CA-5.8.93). As such, to the extent that the CRM is recognised by the bank, the adjusted risk weight will not be less than that of a comparable direct exposure to the protection provider. Consistent with the standardised approach, banks may choose not to recognise credit protection if doing so would result in a higher capital requirement.

Apr 08CA-5.3.30

The approach to guarantees and credit derivatives closely follows the treatment under the standardised approach as specified in paragraphs CA-4.5.1 to CA-4.5.13. The range of eligible guarantors is the same as under the standardised approach except that companies that are internally rated and associated with a PD equivalent to A- or better may also be recognised. To receive recognition, the requirements outlined in paragraphs CA-4.5.1 to CA-4.5.6 must be met.

Apr 08CA-5.3.31

Eligible guarantees from eligible guarantors will be recognised as follows:

(a) For the covered portion of the exposure, a risk weight is derived by taking:• the risk-weight function appropriate to the type of guarantor, and• the PD appropriate to the guarantor's borrower grade, or some grade between the underlying obligor and the guarantor's borrower grade if the bank deems a full substitution treatment not to be warranted.(b) The bank may replace the LGD of the underlying transaction with the LGD applicable to the guarantee taking into account seniority and any collateralisation of a guaranteed commitment.Apr 08CA-5.3.32

The uncovered portion of the exposure is assigned the risk weight associated with the underlying obligor.

Apr 08CA-5.3.33

Where partial coverage exists, or where there is a currency mismatch between the underlying obligation and the credit protection, it is necessary to split the exposure into a covered and an uncovered amount. The treatment in this approach follows that outlined in the standardised approach in paragraphs CA-4.5.10 to CA-4.5.12, and depends upon whether the cover is proportional or tranched.

Apr 08CA-5.3.34

A bank using an IRB approach has the option of using the substitution approach in determining the appropriate capital requirement for an exposure. However, for exposures hedged by one of the following instruments the double default framework according to paragraphs CA-5.3.12 to CA-5.3.16 may be applied subject to the additional operational requirements set out in paragraph CA-5.3.39. A bank may decide separately for each eligible exposure to apply either the double default framework or the substitution approach:

(a) Single-name, unfunded credit derivatives (e.g. credit default swaps) or single-name guarantees;(b) First-to-default basket products — the double default treatment will be applied to the asset within the basket with the lowest risk-weighted amount; and(c) nth-to-default basket products — the protection obtained is only eligible for consideration under the double default framework if eligible (n-1)th default protection has also been obtained or where (n-1) of the assets within the basket have already defaulted.Amended: April 2011

Apr 08— Operational Requirements for Recognition of Double Default

CA-5.3.35

The double default framework is only applicable where the following conditions are met:

(a) The risk weight that is associated with the exposure prior to the application of the framework does not already factor in any aspect of the credit protection;(b) The entity selling credit protection is a bank42, investment firm or insurance company (but only those that are in the business of providing credit protection, including mono-lines, re-insurers, and non-sovereign credit export agencies43), referred to as a financial firm, that:• It is regulated in a manner broadly equivalent to that in this Module (where there is appropriate supervisory oversight and transparency/market discipline), or externally rated as at least investment grade by a credit rating agency deemed suitable for this purpose by CBB;• Had an internal rating with a PD equivalent to or lower than that associated with an external A- rating at the time the credit protection for an exposure was first provided or for any period of time thereafter; and• Has an internal rating with a PD equivalent to or lower than that associated with an external investment-grade rating.(c) The underlying obligation is:• A corporate exposure as defined in paragraphs CA-5.2.5 to CA-5.2.15 (excluding specialised lending exposures for which the supervisory slotting criteria approach described in paragraphs CA-5.3.6 to CA-5.3.11 is being used); or• A claim on a PSE that is not a sovereign exposure as defined in paragraph CA-5.2.16; or• A loan extended to a small business and classified as a retail exposure as defined in paragraph CA-5.2.18.(d) The underlying obligor is not:• A financial firm as defined in (b); or• A member of the same group as the protection provider.(e) The credit protection meets the minimum operational requirements for such instruments as outlined in paragraphs CA-4.5.1 to CA-4.5.5;(f) In keeping with paragraph CA-4.5.2 for guarantees, for any recognition of double default effects for both guarantees and credit derivatives a bank must have the right and expectation to receive payment from the credit protection provider without having to take legal action in order to pursue the counterparty for payment. To the extent possible, a bank must take steps to satisfy itself that the protection provider is willing to pay promptly if a credit event should occur;(g) The purchased credit protection absorbs all credit losses incurred on the hedged portion of an exposure that arise due to the credit events outlined in the contract;(h) If the payout structure provides for physical settlement, then there must be legal certainty with respect to the deliverability of a loan, bond, or contingent liability. If a bank intends to deliver an obligation other than the underlying exposure, it must ensure that the deliverable obligation is sufficiently liquid so that the bank would have the ability to purchase it for delivery in accordance with the contract;(i) The terms and conditions of credit protection arrangements must be legally confirmed in writing by both the credit protection provider and the bank;(j) In the case of protection against dilution risk, the seller of purchased receivables must not be a member of the same group as the protection provider; and(k) There is no excessive correlation between the creditworthiness of a protection provider and the obligor of the underlying exposure due to their performance being dependent on common factors beyond the systematic risk factor. The bank has a process to detect such excessive correlation. An example of a situation in which such excessive correlation would arise is when a protection provider guarantees the debt of a supplier of goods or services and the supplier derives a high proportion of its income or revenue from the protection provider.

42 This does not include PSEs and MDBs, even though claims on these may be treated as claims on banks according to paragraph CA-5.2.17.

43By non-sovereign it is meant that credit protection in question does not benefit from any explicit sovereign counter-guarantee.

Amended: April 2011

Apr 08(iii) Exposure at Default (EAD)

CA-5.3.36

The following sections apply to both on and off-balance sheet positions. All exposures are measured gross of specific provisions or partial write-offs. The EAD on drawn amounts should not be less than the sum of (i) the amount by which a bank's regulatory capital would be reduced if the exposure were written-off fully, and (ii) any specific provisions and partial write-offs. When the difference between the instrument's EAD and the sum of (i) and (ii) is positive, this amount is termed a discount. The calculation of risk-weighted assets is independent of any discounts. Under the limited circumstances described in paragraph CA-5.7.7, discounts may be included in the measurement of total eligible provisions for purposes of the EL-provision calculation set out in section CA-5.7.

Apr 08Exposure Measurement for On-balance Sheet Items

CA-5.3.37

On-balance sheet netting of loans and deposits will be recognised subject to the same conditions as under the standardised approach (see paragraph CA-4.4.1). Where currency or maturity mismatched on-balance sheet netting exists, the treatment follows the standardised approach, as set out in paragraphs CA-4.5.12 and CA-4.6.1 to CA-4.6.4.

Apr 08Exposure Measurement for Off-balance Sheet Items (with the Exception of FX and Interest-rate, Equity, and Commodity-related Derivatives)

CA-5.3.38

For off-balance sheet items, exposure is calculated as the committed but undrawn amount multiplied by a CCF.

Apr 08CA-5.3.39

The types of instruments and the CCFs applied to them are the same as those in the standardised approach, as outlined in paragraphs CA-3.3.1 to CA-3.3.15 with the exception of commitments, Note Issuance Facilities (NIFs) and Revolving Underwriting Facilities (RUFs).

Apr 08CA-5.3.40

A CCF of 75% will be applied to commitments, NIFs and RUFs regardless of the maturity of the underlying facility. This does not apply to those facilities which are uncommitted, that are unconditionally cancellable, or that effectively provide for automatic cancellation, for example due to deterioration in a borrower's creditworthiness, at any time by the bank without prior notice. A CCF of 0% will be applied to these facilities.

Apr 08CA-5.3.41

The amount to which the CCF is applied is the lower of the value of the unused committed credit line, and the value that reflects any possible constraining availability of the facility, such as the existence of a ceiling on the potential lending amount which is related to a borrower's reported cash flow. If the facility is constrained in this way, the bank must have sufficient line monitoring and management procedures to support this contention.

Apr 08CA-5.3.42

In order to apply a 0% CCF for unconditionally and immediately cancellable corporate overdrafts and other facilities, banks must demonstrate that they actively monitor the financial condition of the borrower, and that their internal control systems are such that they could cancel the facility upon evidence of a deterioration in the credit quality of the borrower.

Apr 08CA-5.3.43

Where a commitment is obtained on another off-balance sheet exposure, banks under the foundation approach are to apply the lower of the applicable CCFs.

Apr 08Exposure Measurement for Transactions that Expose Banks to Counterparty Credit risk

CA-5.3.44

Measures of exposure for SFTs and OTC derivatives that expose banks to counterparty credit risk under the IRB approach will be calculated as per the rules set forth in Appendix CA-2 of this Module.

Apr 08(iv) Effective Maturity (M)

CA-5.3.45

Effective maturity (M) will be 2.5 years except for repo-style transactions where the effective maturity will be 6 months. However, banks can apply to CBB for approval to measure M for each facility using the definition provided below.

Apr 08CA-5.3.46

Except as noted in proceeding paragraph, M is defined as the greater of one year and the remaining effective maturity in years as defined below. In all cases, M will be no greater than 5 years:

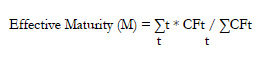

(a) For an instrument subject to a determined cash flow schedule, effective maturity M is defined as:

where CFt denotes the cash flows (principal, interest payments and fees) contractually payable by the borrower in period t.(b) If a bank is not in a position to calculate the effective maturity of the contracted payments as noted above, it is allowed to use a more conservative measure of M such as that it equals the maximum remaining time (in years) that the borrower is permitted to take to fully discharge its contractual obligation (principal, interest, and fees) under the terms of loan agreement. Normally, this will correspond to the nominal maturity of the instrument; and(c) For derivatives subject to a master netting agreement, the weighted average maturity of the transactions should be used when applying the explicit maturity adjustment. Further, the notional amount of each transaction should be used for weighting the maturity.Amended: April 2011

Apr 08CA-5.3.47

The one-year floor does not apply to certain short-term exposures, comprising fully or nearly-fully collateralised44 capital market-driven transactions (i.e. OTC derivatives transactions and margin lending) and repo-style transactions (i.e. repos/reverse repos and securities lending/borrowing) with an original maturity of less then one year, where the documentation contains daily remargining clauses. For all eligible transactions the documentation must require daily revaluation, and must include provisions that must allow for the prompt liquidation or setoff of the collateral in the event of default or failure to re-margin. The maturity of such transactions must be calculated as the greater of one-day, and the effective maturity (M, consistent with the definition above).

44 The intention is to include both parties of a transaction meeting these conditions where neither of the parties is systematically under-collateralised.

Apr 08CA-5.3.48

In addition to the transactions considered in the preceding paragraph above, other short-term exposures with an original maturity of less than one year that are not part of a bank's ongoing financing of an obligor are eligible for exemption from the one-year floor. Such transactions include:

(a) Some capital market-driven transactions and repo-style transactions that might not fall within the scope of the preceding paragraph;(b) Some short-term self-liquidating trade transactions. Import and export letters of credit and similar transactions could be accounted for at their actual remaining maturity;(c) Some exposures arising from settling securities purchases and sales. This could also include overdrafts arising from failed securities settlements provided that such overdrafts do not continue more than a short, fixed number of business days;(d) Some exposures arising from cash settlements by wire transfer, including overdrafts arising from failed transfers provided that such overdrafts do not continue more than a short, fixed number of business days;(e) Some exposures to banks arising from foreign exchange settlements; and(f) Some short-term loans and deposits.Apr 08CA-5.3.49

For transactions falling within the scope of paragraph CA-5.3.47 subject to a master netting agreement, the weighted average maturity of the transactions should be used when applying the explicit maturity adjustment. A floor equal to the minimum holding period for the transaction type set out in paragraph CA-4.3.11 will apply to the average. Where more than one transaction type is contained in the master netting agreement a floor equal to the highest holding period will apply to the average. Further, the notional amount of each transaction should be used for weighting maturity.

Apr 08CA-5.3.50

Where there is no explicit adjustment, the effective maturity (M) assigned to all exposures is set at 2.5 years unless otherwise specified in paragraph CA-5.3.45.

Apr 08