Environmental, Social and Governance Requirements

ESG-A: Introduction

ESG-A.1 Introduction and Scope

ESG-A.1.1

The ESG reporting landscape is in a state of constant change, as companies now face mounting pressure from investors, regulators, and other stakeholders to disclose information relating to their stance on climate change, social issues, and governance factors. This heightened interest has led to a surge in sustainable investments such as ESG funds and Green Bonds, as more and more investors recognise the significance of taking into account the financial and economic ramifications of environmental, social and governance ("ESG") issues when making investment decisions. ESG factors also have an influence on a company's capacity to execute its business plan and produce value in the long run. ESG refers to the following:

(a) Environmental: This factor includes a company's impact on the natural environment, such as its carbon emissions, energy use, waste management, and water usage.(b) Social: This factor encompasses a company's impact on society, including its treatment of employees, customer relations, community engagement, and human rights policies.(c) Governance: This factor relates to a company's internal management and oversight, including issues such as executive compensation, board diversity, and transparency.Added: January 2024ESG-A.1.2

ESG reporting is recognized as one of the diverse approaches accessible for assessing the company's overall performance. It offers insights into a company's performance that extend beyond the information conveyed in financial statements. Investors and other stakeholders seeking to evaluate the long-term sustainability and ethical impact of companies’ operations use such information in their decision-making process.

Added: January 2024ESG-A.1.3

Sustainability reporting and ESG are related but distinct concepts. ESG reports conform to a more specific set of criteria that companies can measure and report against, whereas sustainability reporting provides a wide-ranging overview of a company's sustainability initiatives, goals, and strategies, as well as its progress in achieving them. While reporting on ESG metrics is important from a stakeholder perspective, it is imperative that companies proactively implement strategies to improve environmental and social performance, and to ensure good governance practices.

Added: January 2024ESG-A.1.4

The Central Bank of Bahrain (“CBB”) views that ESG reporting is an effective tool for stakeholders to better examine a company’s efficiency, sustainability, and risk exposure. The objective of this Module is to establish a uniform framework for listed companies and licensees to disclose their ESG performance and sustainability efforts. Considering that companies are at different stages on their sustainability journey, this document contains information on important aspects of ESG reporting, such as stages involved in creating an ESG report, recommendations, resources, and requirements when preparing the report. These topics collectively offer a thorough approach to ESG reporting and are to be viewed in conjunction with relevant international best practices, frameworks and guidelines referred to within this document (Appendix 2).

Added: January 2024Purpose

ESG-A.1.5

The objective of this Module is to foster consistency and reliability in ESG reporting, with the goal of facilitating the development of transparent and comparable ESG disclosures that align with both national and international targets and commitments.

Added: January 2024Legal Basis

Scope

ESG-A.1.7

This Module applies to the following companies:

(a) Listed Companies;(b) Banks;(c) Insurance Firms;(d) Category 1 Investment Firms;(e) Category 2 Investment Firms; and(f) Financing Companies.Added: January 2024ESG-A.2 Module History

Evolution of the Module

ESG-A.2.1

This Module was first issued in November 2023. Any material changes that are subsequently made to this Module are annotated with the calendar quarter date in which the change is made.

Added: January 2024ESG-A.2.2

A list of recent changes made to this Module is provided below:

Module Ref. Change Date Description of Changes ESG-1: Reporting Requirements

ESG-1.1 ESG Key Performance Indicators

ESG-1.1.1

Listed companies and licensees must submit an ESG report to the CBB on an annual basis. The ESG report must incorporate the ESG Key Performance Indicators (KPIs) stipulated under Appendix 1. The ESG report can either be a separate document or be included as part of the company's annual report.

Added: January 2024ESG-1.1.2

The branches of foreign financial institutions must either submit the ESG Report of their respective head offices or provide a separate report. Similarly, companies operating under a group governance framework must either submit the consolidated group ESG Report or provide a separate report.

Added: January 2024ESG-1.1.3

Listed companies and licensees must comply with the following requirements with respect to their ESG reports:

(a) Disclosures must remain consistent over time. This entails using consistent formats, language, and metrics from one period to another to enable inter-period comparisons;(b) In cases where certain breakdowns are not easily discernible or relevant, alternative methods or simplified reporting mechanisms can be explored by the company. However, it is essential that the report adequately describes the mechanisms, assumptions, and other relevant details;(c) Organisations must refrain from providing generic or simplistic disclosures that offer little value. It is also important that any additional metrics are sufficiently descriptive;(d) Companies must avoid greenwashing1 their ESG reports. This can damage a company's reputation and erode stakeholder trust. Avoid making unsupported claims or using vague, undefined terms such as "green" or "sustainable" and instead provide specific and measurable information.(e) Provide definitions, reference period(s) and assumptions where relevant; and(f) Provide an explanation in case of non- or partial disclosure of KPIs stipulated under Appendix 1.Added: January 20241 Greenwashing refers to the practice of making misleading or exaggerated claims about the environmental or social benefits of a product, service, or business practice.

ESG-1.2 ESG Reporting Process

ESG-1.2.1

Listed companies and licensees must have in place an adequate governance framework and reporting process for ESG reporting.

Added: January 2024ESG-1.2.2

A standardised set of ESG metrics with clear definitions and guidance is advantageous for companies that are commencing their sustainability reporting journey (see diagram below).

Added: January 2024

Added: January 2024ESG-1.2.3

The ESG reporting process should include the following steps:

(a) First: Understand the purpose and importance of ESGs

A clear ‘ESG purpose’ should be determined to help align reporting efforts consistent with overall business strategy. ESG reporting leads to several benefits, for example:

Risk Management: ESG factors can affect a company's performance and future viability. Companies can identify potential risks and opportunities by assessing ESG factors.

Investor Attraction: More investors are considering ESG factors in their decision-making process. A company clearly conveying comparable and consistent ESG performance can gain a competitive edge and attract more investment.

Reputation Enhancement: Companies that report on ESG can improve their public image, fostering trust and loyalty among stakeholders.

(b) Second: Construct a working group

Establishing a cross-functional ESG team is one of the most crucial stages in taking the company’s ESG plan to the next level. This team includes members from various departments (such as finance, legal, risk management, investor relations etc.), to ensure a varied perspective and a comprehensive approach towards achieving the company’s sustainability and ESG reporting goals. Clear ownership should be established with key authorities to ensure that sustainability initiatives are prioritised and integrated into the company’s overall strategy and operations. The Board of Directors is responsible and accountable for ensuring ESG reporting.

The organisation should ideally construct a management-level committee to oversee sustainability objectives and goals. Where needed, expert advice should be sought.

(c) Third: Understand the Reporting Frameworks

The company should identify the relevant ESG issues and data sources, set targets, and establish a reporting process to ensure accurate disclosure of ESG information. The frameworks should be studied closely to determine which approach to use for each KPI. It is encouraged that the working group begin by reviewing the ESG issues raised in international reporting standards and guidelines to establish boundaries.

Detailed guidance on what topics to report on, how to measure and report on them, and what best practices to follow are presented in international frameworks/guidelines (see Appendix 2).

(d) Fourth: Conduct a Materiality Assessment

A key tool to prepare the company's ESG report is conducting an ESG materiality assessment to identify and prioritise ESG issues relevant to the organisation. Companies use the concept of materiality to guide their sustainability strategic planning processes. A material sustainability issue is an economic, environmental, social or governance issue on which a company has an impact or may be impacted by (both positive and negative). It may also be one that significantly influences the assessments and decisions of stakeholders. Materiality analysis includes determining where your company's value chain may generate externalities, its effects, and which issues, practices, and policies are most essential to ESG goals.

After the company’s most important ESG risks and opportunities have been identified, the insights can be utilised to improve strategic planning and reporting. Companies that focus on material ESG topics from a strategic perspective may benefit in the long run, while those that focus on immaterial elements may incur an implicit opportunity cost.

In the initial stages of materiality assessment, a company should identify its key stakeholders. Building support from significant internal and external stakeholders, while ensuring participation across all divisions and functions, maintains the objectivity and independence of the evaluation process.

Furthermore, it is imperative to establish robust data collection and management systems. The working group should develop a data collection plan that outlines the metrics and indicators to be tracked, taking into account both quantitative and qualitative data sources, encompassing internal and external data. The data collection process should prioritize accuracy, reliability, and the absence of errors or inconsistencies in the collected information. This entails implementing measures to verify the integrity of the data, ensure its accuracy, and promptly address any discrepancies or issues that may surface. It is also important to openly disclose any challenges or gaps encountered during the data collection process and provide a clear plan for addressing them.

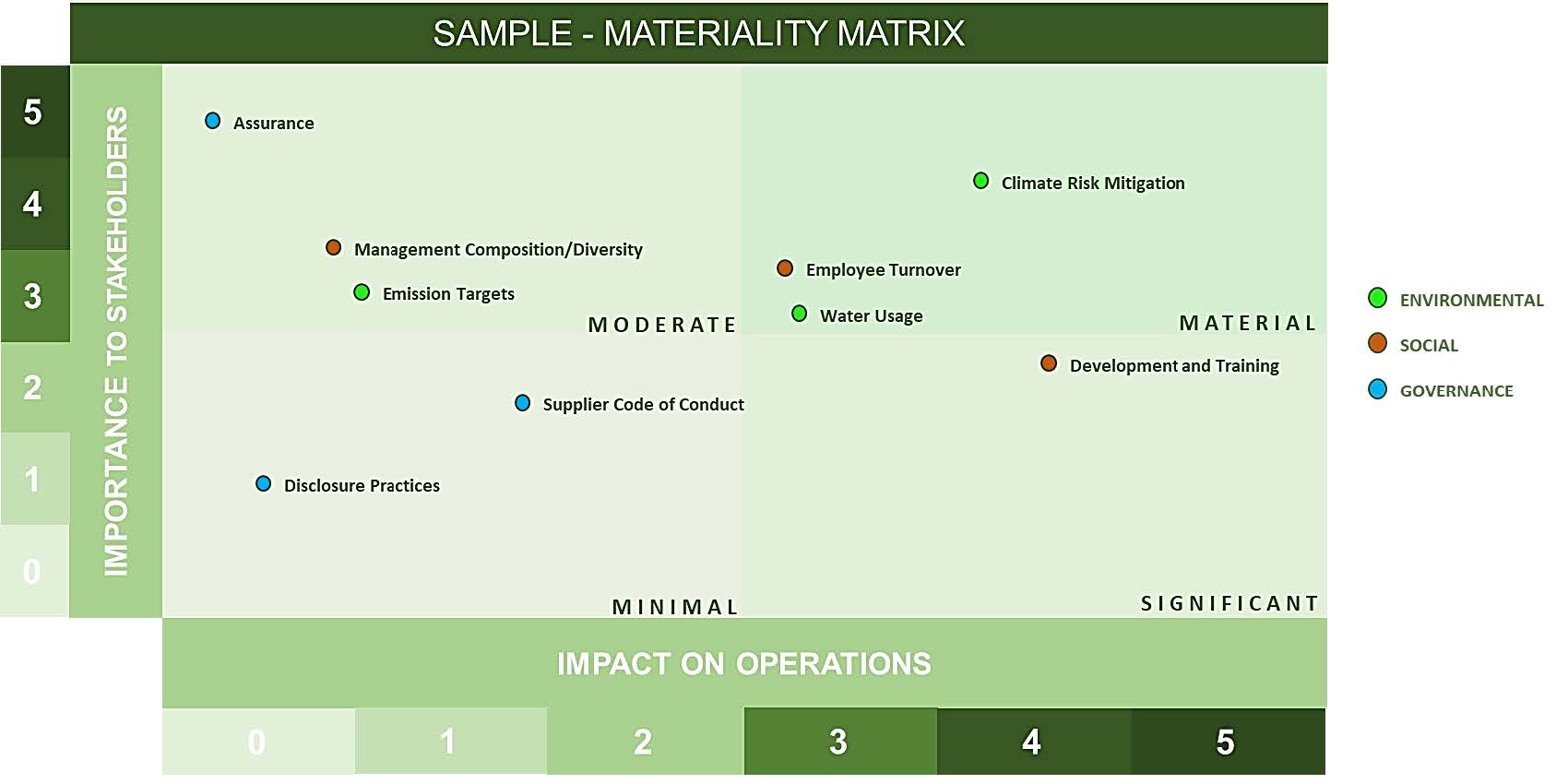

Materiality Matrix

The materiality matrix is a visual tool used to identify and prioritise ESG issues that are most relevant to a company and its stakeholders. The following is an example of how to create a materiality matrix for ESG disclosures:

i. Identify the relevant ESG issues: Start by identifying the ESG issues that are pertinent to the company's operations, industry, and stakeholders. This can be done through a materiality assessment, which involves gathering input from internal and external stakeholders as explained above.ii. Determine the impact and importance of each issue: Evaluate each issue based on its potential impact on the company's financial performance, reputation, and stakeholders.iii. Plot the issues on a matrix: Once you have identified and evaluated the ESG issues, plot them on a matrix with two axes: impact and importance. The impact axis measures the potential impact of the issue on the company's financial performance and reputation, while the importance axis measures the issue's importance to stakeholders.iv. Categorise the issues: Plot the issues into four quadrants:

1. Material: High impact and high importance issues that should be disclosed in the company's ESG report and given priority in the company's sustainability strategy.2. Significant: High impact but lower importance issues that should be monitored and managed but may not require immediate disclosure.3. Moderate: Lower impact but high importance issues that should be monitored and managed to maintain stakeholder trust and meet stakeholder expectations.4. Minimal: Lower impact and lower importance issues that may not require significant attention but should still be monitored for potential risks or opportunities.

Several resources are available to provide guidance on the creation of a Materiality Matrix, such as Climate Disclosures Standards Board2 and the Sustainability Accounting Standards Board’s Materiality Map3.

(e) Fifth: Set Targets and Goals

ESG targets and goals should be specific, measurable, and associated with the overarching strategy of the company; they should also be quantitative or directional. Targets should also be regularly reviewed and updated to ensure they remain relevant and achievable.

(f) Sixth: Reporting ESGs

The ESG report may begin by including a statement on the company’s ESG purpose, how ESGs are governed and the reporting boundary, to allow readers to understand the scope of the report. Further, the company can explain its materiality determination process and stakeholders the company has engaged with. The company should conclude by stating its targets and goals and how it aims to progress its ESG journey, as well as how this aligns with its corporate strategy.

Added: January 20242 https://www.cdsb.net/what-we-do/reporting-guidance/materiality

3 https://sasb.org/standards/materiality-map/Appendix 1 – ESG KPIs and Guidance

The list provides the KPIs as well as guidance on how to report and disclose data for each ESG aspect. It is intended to be used as a reference tool, with references to major international frameworks to provide additional guidance.

KPI Reference(s) Main Reporting Component(s) Environmental E.1: Environmental Oversight

The company should describe its management and board oversight on climate-related risks and opportunities.

Unit: Statement /Description

1. A statement on how the company addresses its environmental impact (e.g., explain whether senior management and/or the board address sustainability issues in meetings or have dedicated committees to do so.)2. A statement of purpose and approach of the board/management towards sustainability matters.3. A description of the following (where applicable):

3.1 Policies3.2 Commitments3.3 Goals and targets (e.g., a description of how management/the board oversee progress against climate/sustainability related targets)3.4 Responsibilities (e.g., if responsibilities are delegated to management-level positions; dedicated sustainability officer(s); Board committees etc.)3.5 Specific actions, such as processes, projects, programs, initiatives and frequency at which the board is informed about climate/sustainability targets and processes.E.2: Energy Consumption

The company should provide information on both direct and indirect energy usage. Direct energy usage refers to energy that is generated and used on property owned or operated by the company. Indirect energy usage refers to energy that is generated elsewhere, such as through utilities, but is used by the company.

Unit: megawatt hours (MWh) or gigajoules (GJ) or multiples

1. Report total energy consumed and breakdown by type;

1.1 Indirect energy consumed in the form of electricity, heating, cooling (i.e., total of energy purchases)1.2 Direct energy consumed, classified by renewable and non-renewable sources.2. State the standards, techniques, assumptions, and/or calculation tools utilised.E.3: Energy Intensity

The company should report total annual energy usage per output scaling factor (such as sales or revenue).

Unit: gigawatt-hours (GWh) per million BHD/USD or multiples

1. Report total energy consumed during the year divided by the selected scaling factor (e.g., sales, revenue etc.).2. State the standards, techniques, assumptions, and/or calculation tools utilised.E.4: Energy Mix

The company should provide a breakdown of its energy consumption by source.

Unit: Percentage (%)

1. Report the percentage of energy used by source, as part of total energy consumption.2. Report the percentage of renewable and non-renewable energy used, as part of total energy consumption.E.5: Green House Gas (GHG) Emissions

The company should report its total Green House Gas Emissions

Unit: metric tons of CO2 or equivalent

1. Report total absolute emissions by scope;

1. Total amount, in CO2 equivalents, for Scope 12. Total amount, in CO2 equivalents, for Scope 23. Total amount, in CO2 equivalents, for Scope 3 (if applicable).2. State the standards, techniques, assumptions, and/or calculation tools utilised.Note: GHG emissions should be calculated in line with the GHG Protocol4 methodology to allow for aggregation and comparability across companies and jurisdictions.

Term definitions:

▪ Scope 1 – Direct emissions from operations that are owned or controlled by the company;▪ Scope 2 – Indirect emissions resulting from the generation of purchased or acquired electricity, heating, cooling, and steam consumed within the company; and▪ Scope 3 – All other indirect emissions that occur outside the company, including both upstream and downstream emissions (if applicable).E.6: Emission Intensity

The company should report annual GHG emission scaled by a relevant scaling factor (such as size (e.g. m2 floor space), employment (e.g. headcount) and monetary units (e.g. revenue or sales)).

Unit: metric tons of CO2 or multiples per unit of scaling factor

1. Report total annual GHG emission during the year divided by the selected scaling factor.2. State the standards, techniques, assumptions, and/or calculation tools utilised.E.7: Climate Risk Mitigation

The company should describe its climate risk identification process, assessment, management processes, and report annual investment in infrastructure, resilience, and product development.

Unit: Statement / Description and monetary value in BHD/USD

1. Describe how your company identifies, assesses, and manages climate-related risks (including physical risks and transition risks).2. Report the amount invested annually in climate-related issues (in BHD or USD) (e.g., research and product innovation).E.8: Water Usage

The company should report total annual amount of water withdrawn, consumed, recycled.

Unit: cubic meters (m3) or equivalent

1. Report the total annual amount of water consumed by the organisation.2. Report the total annual amount of water withdrawn by the organisation.3. Report the total annual amount of water recycled/reclaimed by the organisation.Note: Companies should refer to CDP term definitions of water withdrawal, consumption and recycling.

E.9: Waste Generation

The company should report total weight of waste generated and a description of its waste disposal method.

Unit: Statement /Description and weight in metric tons or equivalent.

1. Total weight of waste generated in metric tons, and a breakdown of this total by composition of the waste (hazardous and non-hazardous).2. Description of the company’s waste disposal method(s).

2.1 Description of the company’s sustainable waste management practices (such as recycling initiatives and waste reduction strategies).3. State the standards, techniques, assumptions, and/or calculation tools utilised.E.10: Emission Targets

The company should provide a description of emission targets set, and steps taken to achieve them, including energy conservation measures.

Unit: Statement/ Description

1. A statement on how the company addresses its total emission.2. A statement of the board/management approach towards its total emissions, including whether it is subject to any country, regional, or industry-level emissions regulations and policies.3. A description of the following (where applicable):

3.1 Policies3.2 Commitments3.3 Goals and targets (e.g., a description of how management/the board oversee progress against climate/sustainability related targets)3.4 Responsibilities (e.g., if responsibilities are delegated to management-level positions; dedicated sustainability officer; Board committees etc.)3.5 Specific actions, such as processes, projects, programs, initiatives, and frequency at which the board is informed about emission targets and process.Social S.1: Total Workforce by sex, age-group, and employment type

The company should report the composition of its total workforce by sex, employment type and age group.

Unit: Amount and Percentage (%)

1. Report total number of employees currently employed within the organisation and the composition of the total workforce as per the below:

1.1 By sex, as percentage of the total workforce1.2 By age-group (as per the GRI’s employee age group categories: (a) under 30 years old, (b) 30-50 years old, and (c) over 50 years old), as a percentage of the total workforce.1.3 By employment type (e.g., full-time, part-time, intern etc.), as a percentage of the total workforce.S.2: Child and Forced Labour

The company should provide a statement of policies it applies to prohibit child/and or forced labour within the company, and if it considers policies that prohibit that same for their suppliers and/or vendors.

Unit: Statement/Description

1. A statement on how the organisation addresses prohibition of child and or/forced labour.2. A statement of the board/management approach's direction, including whether it is subject to any country, regional, or industry-level regulations and policies.3. A description of the following (where applicable):

3.1 Policies3.2 Commitments3.3 Goals and targets3.4 Responsibilities3.5 Specific actions, such as processes, projects, programs, initiatives and frequency at which the board is informed about any issues concerning child and or/forced labour relating to the company.S.3: Employee Turnover

The company should report the total annual turnover (whether voluntary or involuntary) categorised by sex and age group.

Unit: Amount and Percentage (%)

1. Report total annual employee turnover rate (whether voluntary or involuntary) for full-time employees during the reporting period, as per the below categories:

1.1 By sex1.2 By age-group (as per the GRI’s employee age group categories: (a) under 30 years old, (b) 30-50 years old, and (c) over 50 years old).S.4: Gender Pay Ratio

The company should report the median total compensation for men compared to the median total compensation for women (as a ratio).

Unit: Ratio

1. Report the median total compensation for women compared to the median total compensation for men (as a ratio).S.5: Health and Safety

The company should report the total number of injuries and fatalities occurred, lost days due to work injury and a description of occupational health and safety measures.

Unit: Amount and Description

1. Report on the total number of injuries and fatalities occurred in each of the past three years including the reporting year.2. Report lost days due to work injury in each of the past three years including the reporting year.3. A description of occupational health and safety measures adopted, and how they are implemented and monitored.S.6: Non-Discrimination

The company should provide a description of its harassment and/or non-discrimination policy.

Unit: Statement /Description

1. A statement on how the organisation addresses harassment and discrimination matters.2. A statement of the board/management approach, including whether it is subject to any country, regional, or industry-level regulations and policies.S.7: Nationalisation

The company should report on the number and percentage of national employees, as well as initiatives to increase nationalisation.

Unit: Amount and Statement/ Description

1. A statement of the board/management approach to increase nationalisation, including whether it is subject to any country regulations and policies.2. Report the number and percentage of national employees, as part of the total workforce.*Note: Applicable to Bahrain only.

S.8: Community Investment

The company should provide detailed information on the scope and impact of its community investment activities, as well as amount invested in community as a percentage of company revenue.

Unit: Description and Percentage (%)

1. Report the amount invested in the community as a percentage of company revenues.2. Provide a description of the scope and impact of its community investment initiatives.S.9: Human rights

The company should provide a description of its policy on human rights.

Unit: Statement /Description

1. A statement on how the organisation addresses human rights.2. A statement of the board/management approach's direction, including whether it is subject to any country, regional, or industry-level regulations and policies.3. A description of the following (where applicable):

3.1 Policies (and if it also covers suppliers and vendors).3.2 Commitments3.3 Goals and targets3.4 ResponsibilitiesS.10: Management Composition/Diversity

The company should report the percentage of male to female metrics broken down by various organisational levels.

Unit: Percentage (%)

1. Report percentage of male to female metrics, as per the below categories:

1.1 Entry-level1.2 Mid-level1.3 Senior/Executive level positionsS.11: Development and Training

The company should report average hours of training that its employees have undertaken during the reporting period.

Unit: Percentage (%)

1. Report average hours of training, as per the below categories:

1.1 By Sex1.2 By Employee category (Full-time, part-time, internship etc.)Governance G.1: Board Composition

The company should report the composition of the Board categorised by directors, such as the chairman, executive directors, non-executive directors, and independent non-executive directors.

Unit: Statement/ Description

1. Report board size2. Report female board directors by number and percentage of the Board size.3. Report composition of the board and its committees by:

3.1 Executive or non-executive.3.2 Independence.3.3 Tenure.3.4 Representation (appointed or elected)3.5 Details of non-compliance with regulations, as well as a description of the corrective actions taken.G.2: Collective Bargaining

The company should report on the total enterprise headcount covered by collective bargaining agreements (Unions) and the process in which employees’ contracts with their employers to determine their terms of employment.

Unit: Description and amount

1. Report total enterprise headcount covered by collective bargaining agreements (Unions) (if applicable).2. Provide a description of the process by which employees negotiate their contracts with the organisation to determine their terms of employment (e.g., compensation, benefits, hours, leave, occupational health and safety standards, initiatives to balance work and family etc.)Note: Companies should refer to International Labour Organisation (ILO) Convention 1545 term definition of ‘Collective Bargaining’.

G.3: Whistleblowing

The company should provide a description of the mechanisms used to discuss and report on behaviour.

Unit: Statement / Description

1. Provide a description of internal and external mechanisms for seeking advice and reporting concerns on organisational integrity.2. Provide a description on awareness initiatives conducted by the organisation.G.4: Data privacy

The company should Report if it follows a Data Privacy policy and if the company has taken steps to comply with Personal Data Protection Law (PDPL) rules.

Unit: Statement / Description

1. Provide a description of the company’s Data Privacy policy.2. Provide a statement of the steps taken to comply with Personal Data Protection Law (PDPL) rules.G.5: Disclosure Practices

The company should provide a description of its sustainability disclosure practices.

Unit: Statement / Description

1. Report if the company provides its sustainability data to sustainability supporting organisations such as the Global Reporting Initiative (GRI) Secretariat, United Nations (UN), CDP etc.2. Report if the company focuses on specific UN Sustainable Development Goals (SDGs), including setting targets and reporting progress.3. State whether the company publishes a sustainability report and/or how it integrates sustainability data in its disclosures.G.6: Conflict of interest

The company shall describe the processes for the highest governance body to ensure that conflicts of interest are prevented and mitigated.

Unit: Statement / Description

1. Report whether conflicts of interest are disclosed to stakeholders, including, at a minimum, conflicts of interest relating to:

1.1 Cross-board membership1.2 Cross-shareholding with suppliers and other stakeholders;1.3 Existence of controlling shareholders;1.4 Related parties, their relationships, nature, transactions, and outstanding balances.G.7: Supplier Code of Conduct

The company should report if it has established a Supplier Code of Conduct.

Unit: Statement / Description and Percentage (%)

1. Provide a description of the company’s Supplier Code of Conduct.2. Report the percentage of suppliers that comply with the company’s code of conduct and the compliance assessment mechanism.Note: A Supplier Code of Conduct refers to a set of principles and standards that outline the company’s expectations for responsible business practices by its supplier.

G.8: Incentivised Pay

The company should describe the processes for incentivising executives to perform sustainably.

Unit: Statement / Description

1. Report if executives are formally incentivised to perform on sustainability.2. Report the percentage of executive compensation tied to ESG performance metrics.3. Provide a description of other links between executive performance and sustainability performance (if any).G.9: Ethics & Anti-corruption

The company should describe its policy on ethical conduct and anti-corruption.

Unit: Statement / Description and Percentage (%)

1. Report if your company follows an Ethics and/or Anti-Corruption policy.

1.1 If yes, report the percentage of the workforce that has formally certified its compliance with the policy (provide description of certification and process).2. Provide a statement of the company’s commitment towards its ethics and/or anti-Corruption policy/position.G.10: Assurance

The company shall describe the processes by which its sustainability disclosures are assured or validated.

Unit: Statement / Description

1. Provide a description of the process by which sustainability disclosures are assured or validated.

1.1 Report if the company’s sustainability disclosures are assured or validated by an independent third party.Added: January 20245 https://www.ilo.org/ C154 - Collective Bargaining Convention, 1981 (No. 154)

Appendix 2 – ESG Reporting Frameworks and Global Initiatives

A range of the most widely used and accepted frameworks are provided below:

The Global Reporting Initiative (GRI): The Global Reporting Initiative (GRI) is a non-profit multinational organisation that offers a complete framework for sustainability reporting. The organisation was created in 1997 with the intention of supporting long-term development via transparency and accountability. The GRI Standards are classified into three series: Universal Standards, Topic-specific Standards, and Sector-specific Standards. They provide a comprehensive set of disclosures across a range of sustainability topics, including governance, labour practices, human rights, environmental impacts, product responsibility, and community engagement. The GRI Standards are designed to be flexible and adaptable to different types of companies, industries, and geographic regions. The framework encourages companies to report not only on their positive sustainability performance but also on their challenges and areas for improvement. This helps to promote transparency and accountability and enables stakeholders to make informed decisions based on reliable and comparable information.

Link: https://www.globalreporting.org/

Task Force on Climate-related Financial Disclosures (TCFD): The TCFD is a global voluntary framework that provides guidelines for companies to disclose climate-related financial risks and opportunities. Established by the Financial Stability Board, TCFD recommendations cover four core areas: governance, strategy, risk management, and metrics and targets. The TCFD recommendations are designed to be flexible and scalable to different types of companies and industries. They are also intended to help companies identify and seize opportunities related to the transition to a low-carbon economy.

Link: http://www.fsb-tcfd.org/

CDP (formerly the Carbon Disclosure Project): CDP is a global environmental impact non-profit that runs a disclosure system for companies to report on their environmental performance. CDP focuses on climate change, water security, and deforestation, and provides a standardised framework for companies to measure and manage their environmental impacts. It provides a standardised questionnaire that companies can use to report on their environmental impacts and risks, as well as their strategies for mitigating these impacts.

Link: http://www.cdp.net/en

Integrated Reporting Framework (IR): A comprehensive view of an organisation's strategy, governance, performance, and prospects—including ESG factors—is offered by the IR Framework. It encourages businesses to communicate how they are managing their stakeholder relationships as well as how they are creating value over the short, medium, and long term. The IR Framework can be used in conjunction with other reporting frameworks, such as the GRI Standards and the SASB Standards, and is intended to be adaptable to different types of companies and industries.

Link: http://www.integratedreporting.org/

Sustainability Accounting Standards Board (SASB): The SASB Standards are intended to assist businesses in providing investors with financial material ESG information. The framework focuses on 77 sustainability issues that are particular to each industry and are most likely to influence a company's financial performance. Environment, social capital, human capital, business model and innovation, and leadership and governance are the five categories into which these subjects are divided. The SASB Standards offer guidance on how to incorporate ESG information into financial reporting and are made to be compatible with frameworks like the Generally Accepted Accounting Principles (GAAP).

Link: http://www.sasb.org/

Climate Disclosure Standards Board (CDSB): The CDSB develops and publishes a set of globally recognised reporting standards called the Climate Change Reporting Framework. This framework provides guidance on how companies can report on their climate-related risks and opportunities in a clear, comprehensive, and consistent manner. The CDSB also provides guidance on how companies can report on other ESG issues, such as their impact on natural resources, social and human capital, and governance.

Link: https://www.cdsb.net/

International Sustainability Standards Board (ISSB): An independent body established by the IFRS Foundation to develop global sustainability reporting standards. The IFRS Sustainability Disclosure Standards (IFRS SDS) provide a structured framework for companies to disclose material sustainability information in a consistent and comparable manner, covering a wide range of environmental, social, and governance (ESG) topics. IFRS S1 establishes disclosure requirements that allow companies to communicate sustainability-related risks and opportunities to investors over the short, medium, and long term. Complementing this, IFRS S2 provides detailed guidelines for disclosing climate-related information and is meant to be used in conjunction with IFRS S1. Together, these standards enhance companies' ability to provide comprehensive and relevant sustainability reporting, enabling investors to make well-informed decisions.

Link: https://www.ifrs.org/

Added: January 2024