ESG-1.2 ESG Reporting Process

ESG-1.2.1

Listed companies and licensees must have in place an adequate governance framework and reporting process for ESG reporting.

Added: January 2024ESG-1.2.2

A standardised set of ESG metrics with clear definitions and guidance is advantageous for companies that are commencing their sustainability reporting journey (see diagram below).

Added: January 2024

Added: January 2024ESG-1.2.3

The ESG reporting process should include the following steps:

(a) First: Understand the purpose and importance of ESGs

A clear ‘ESG purpose’ should be determined to help align reporting efforts consistent with overall business strategy. ESG reporting leads to several benefits, for example:

Risk Management: ESG factors can affect a company's performance and future viability. Companies can identify potential risks and opportunities by assessing ESG factors.

Investor Attraction: More investors are considering ESG factors in their decision-making process. A company clearly conveying comparable and consistent ESG performance can gain a competitive edge and attract more investment.

Reputation Enhancement: Companies that report on ESG can improve their public image, fostering trust and loyalty among stakeholders.

(b) Second: Construct a working group

Establishing a cross-functional ESG team is one of the most crucial stages in taking the company’s ESG plan to the next level. This team includes members from various departments (such as finance, legal, risk management, investor relations etc.), to ensure a varied perspective and a comprehensive approach towards achieving the company’s sustainability and ESG reporting goals. Clear ownership should be established with key authorities to ensure that sustainability initiatives are prioritised and integrated into the company’s overall strategy and operations. The Board of Directors is responsible and accountable for ensuring ESG reporting.

The organisation should ideally construct a management-level committee to oversee sustainability objectives and goals. Where needed, expert advice should be sought.

(c) Third: Understand the Reporting Frameworks

The company should identify the relevant ESG issues and data sources, set targets, and establish a reporting process to ensure accurate disclosure of ESG information. The frameworks should be studied closely to determine which approach to use for each KPI. It is encouraged that the working group begin by reviewing the ESG issues raised in international reporting standards and guidelines to establish boundaries.

Detailed guidance on what topics to report on, how to measure and report on them, and what best practices to follow are presented in international frameworks/guidelines (see Appendix 2).

(d) Fourth: Conduct a Materiality Assessment

A key tool to prepare the company's ESG report is conducting an ESG materiality assessment to identify and prioritise ESG issues relevant to the organisation. Companies use the concept of materiality to guide their sustainability strategic planning processes. A material sustainability issue is an economic, environmental, social or governance issue on which a company has an impact or may be impacted by (both positive and negative). It may also be one that significantly influences the assessments and decisions of stakeholders. Materiality analysis includes determining where your company's value chain may generate externalities, its effects, and which issues, practices, and policies are most essential to ESG goals.

After the company’s most important ESG risks and opportunities have been identified, the insights can be utilised to improve strategic planning and reporting. Companies that focus on material ESG topics from a strategic perspective may benefit in the long run, while those that focus on immaterial elements may incur an implicit opportunity cost.

In the initial stages of materiality assessment, a company should identify its key stakeholders. Building support from significant internal and external stakeholders, while ensuring participation across all divisions and functions, maintains the objectivity and independence of the evaluation process.

Furthermore, it is imperative to establish robust data collection and management systems. The working group should develop a data collection plan that outlines the metrics and indicators to be tracked, taking into account both quantitative and qualitative data sources, encompassing internal and external data. The data collection process should prioritize accuracy, reliability, and the absence of errors or inconsistencies in the collected information. This entails implementing measures to verify the integrity of the data, ensure its accuracy, and promptly address any discrepancies or issues that may surface. It is also important to openly disclose any challenges or gaps encountered during the data collection process and provide a clear plan for addressing them.

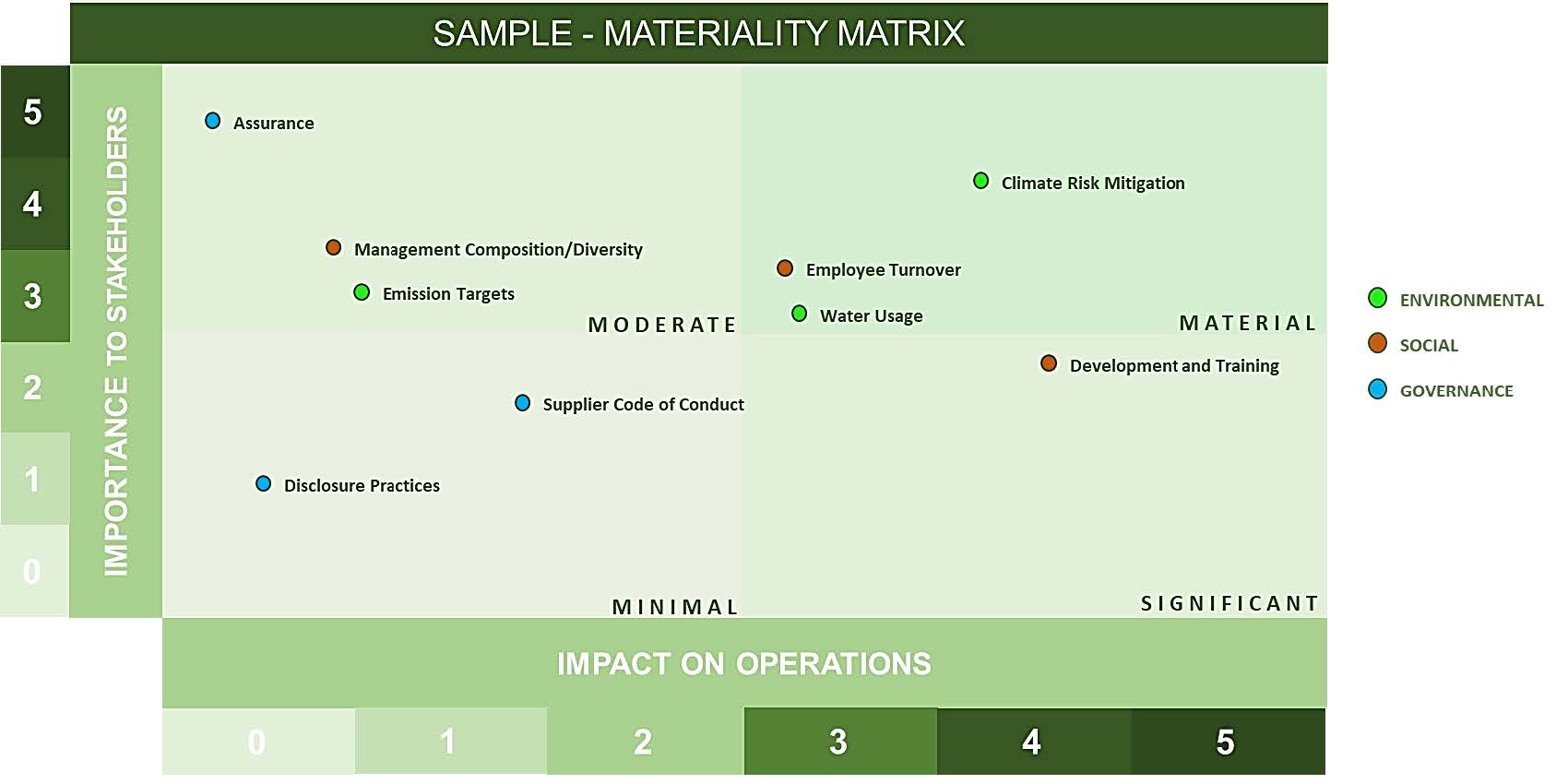

Materiality Matrix

The materiality matrix is a visual tool used to identify and prioritise ESG issues that are most relevant to a company and its stakeholders. The following is an example of how to create a materiality matrix for ESG disclosures:

i. Identify the relevant ESG issues: Start by identifying the ESG issues that are pertinent to the company's operations, industry, and stakeholders. This can be done through a materiality assessment, which involves gathering input from internal and external stakeholders as explained above.ii. Determine the impact and importance of each issue: Evaluate each issue based on its potential impact on the company's financial performance, reputation, and stakeholders.iii. Plot the issues on a matrix: Once you have identified and evaluated the ESG issues, plot them on a matrix with two axes: impact and importance. The impact axis measures the potential impact of the issue on the company's financial performance and reputation, while the importance axis measures the issue's importance to stakeholders.iv. Categorise the issues: Plot the issues into four quadrants:

1. Material: High impact and high importance issues that should be disclosed in the company's ESG report and given priority in the company's sustainability strategy.2. Significant: High impact but lower importance issues that should be monitored and managed but may not require immediate disclosure.3. Moderate: Lower impact but high importance issues that should be monitored and managed to maintain stakeholder trust and meet stakeholder expectations.4. Minimal: Lower impact and lower importance issues that may not require significant attention but should still be monitored for potential risks or opportunities.

Several resources are available to provide guidance on the creation of a Materiality Matrix, such as Climate Disclosures Standards Board2 and the Sustainability Accounting Standards Board’s Materiality Map3.

(e) Fifth: Set Targets and Goals

ESG targets and goals should be specific, measurable, and associated with the overarching strategy of the company; they should also be quantitative or directional. Targets should also be regularly reviewed and updated to ensure they remain relevant and achievable.

(f) Sixth: Reporting ESGs

The ESG report may begin by including a statement on the company’s ESG purpose, how ESGs are governed and the reporting boundary, to allow readers to understand the scope of the report. Further, the company can explain its materiality determination process and stakeholders the company has engaged with. The company should conclude by stating its targets and goals and how it aims to progress its ESG journey, as well as how this aligns with its corporate strategy.

Added: January 20242 https://www.cdsb.net/what-we-do/reporting-guidance/materiality

3 https://sasb.org/standards/materiality-map/