Derivative Exposures

CA-15.3.24

Exposures to derivatives are included in the leverage ratio exposure by means of two components:

(a) Replacement cost (RC); and(b) Potential Future Exposure (PFE).Added: October 2018

CA-15.3.25

Bahraini conventional bank licensees must calculate their exposures associated with all derivative transactions including where aBahraini conventional bank licensee sells protection using a credit derivative, as the replacement cost (RC)28 for the current exposure plus an add-on for PFE, as described in Paragraph CA-15.3.26. If the derivative exposure is covered by an eligible bilateral netting contract as specified in this Section 15.4, the treatment in Chapter CA-4 may be applied29. Written credit derivatives are subject to an additional treatment, as set out in Paragraphs CA-15.3.37 to CA-15.3.39.Added: October 2018

28 If there is no accounting measure of exposure for certain derivative instruments because they are held (completely) off-balance sheet, the bank must use the sum of positive fair values of these derivatives as the replacement cost.

29 Cross-product netting is not permitted in determining the leverage ratio exposure.

CA-15.3.26

For derivative transactions not covered by an eligible bilateral netting contract as specified in Paragraphs CA-15.4.1 to CA-15.4.3, the amount to be included in the exposure measure is determined as follows:

Exposure measure = alpha * (RC+PFE)

where

alpha = 1.4RC = the replacement cost of the contract (obtained by marking to market), where the contract has a positive value. RC is determined in accordance with CA-15.3.27PFE = an amount for PFE calculated in accordance with CA-15.3.28.Added: October 2018

CA-15.3.27

The replacement cost of a transaction or netting set is measured as follows:

RC = max {V - CVMr, + CVMp, 0}where (i) V is the market value of the individual derivative transaction or of the derivative transactions in a netting set; (ii) CVMr is the cash variation margin received that meets the conditions set out in Paragraph CA-15.3.33 and for which the amount has not already reduced the market value of the derivative transaction V under the bank's operative accounting standard; and (iii) CVMp is the cash variation margin provided by the bank and that meets the same conditions.

Added: October 2018

CA-15.3.28

The potential future exposure (PFE) for derivative exposures must be calculated mathematically as follows:

PFE = multiplier*AddOn aggregateFor the purposes of the leverage ratio framework, the multiplier is fixed at one. Moreover, when calculating the add-on component, for all margined transactions the maturity factor set out in CA-15.3.29 below may be used. Further, as written options create an exposure to the underlying, they must be included in the leverage ratio exposure measure by applying the treatment described herein, even if certain written options are permitted the zero exposure at default (EAD) treatment allowed in the risk-based framework.

Added: October 2018

CA-15.3.29

The minimum time risk horizons include:

a) The lesser of one year and remaining maturity of the derivative contract for unmargined transactions, floored at ten business days. Therefore, the adjusted notional at the trade level of an unmargined transaction must be multiplied by:

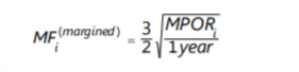

where Mi is the transaction i remaining maturity floored by 10 business daysb) For margined transactions, the minimum margin period of risk is determined as follows:— At least ten business days for non-centrally-cleared derivative transactions subject to daily margin agreements.— Five business days for centrally cleared derivative transactions subject to daily margin agreements that clearing members have with their clients.— 20 business days for netting sets consisting of 5,000 transactions that are not with a central counterparty.— Doubling the margin period of risk for netting sets with outstanding disputes. Therefore, the adjusted notional at the trade level of a margined transaction should be multiplied by:

where i MPOR is the margin period of risk appropriate for the margin agreement containing the transaction i.Added: October 2018